Quarterly Journal of Economics: Denial Of A Wanted Abortion Has “Immediate And Lasting Effects” Including A Higher Risk Of Short Term Death, And, Even Fifteen Years Later, “More Health Issues, Lower Educational Attainment, Higher Rates Of Single Motherhood, Poverty, And Reliance On Government Assistance.” According to Londoño-Vélez and Saravia, “This article examines the impact of denying a wanted abortion on women and children in Colombia using high-quality administrative microdata and credibly exogenous variation in abortion access. Women can seek legal abortions through a tutela, with cases randomly assigned to judges. Female judges are 20 percentage points (32%) less likely to deny abortion cases than are male judges, and we use the judge’s sex as an instrument for abortion denial. Denial of a wanted abortion has both immediate and lasting effects. It increases a woman’s risk of death by 2.5 percentage points within nine months, mainly due to unsafe abortion procedures, and raises the likelihood of carrying the pregnancy to term by 31 percentage points. Tracking outcomes up to 15 years later, we find that women denied an abortion experience more health issues, lower educational attainment, reduced labor force participation, and higher rates of single motherhood, poverty, and reliance on government assistance. Existing children, born before their mother sought an abortion, are less likely to attend school and are more likely to work.” [Londoño-Vélez and Saravia, 2025-05]

Deterioration

Q1 2025: Large American Companies Filed For Bankruptcy At The Fastest Rate In 15 Years. According to Bloomberg, “Large US companies filed bankruptcy at the fastest rate in 15 years through the first three months of 2025, S&P Global Market Intelligence said Thursday. A total of 188 bankruptcies were filed by large companies through March, the most since 254 such filings were made over the first three months of 2010, S&P said in a report. Last year, 139 large corporate bankruptcies were filed over the same three-month time period. Companies that sought court protection in March include the owner of Forever 21’s US retail operator, Canada’s Mitel Networks and film producer Village Roadshow Entertainment Group. Genetics testing firm 23andMe and dining chain Hooters of America also went bankrupt last month. ‘Companies, particularly those with weaker balance sheets, continue to face challenges as debt matures and needs to be refinanced at higher interest rates than at the time of issuance,’ S&P said. The high rate of filings follows an increase in corporate bankruptcies in the past few years. The number of companies filing repeat bankruptcies in 2023 and 2024 was the most over a two year span since 2020, Bloomberg News previously reported.” [Bloomberg, 2025-04-10]

Amid A Notable Increase In The Jobless Rate For Americans Aged 20 To 24, Leading Indicators Of Grad School Interest Have Increased. According to Bloomberg, “It’s a classic recession move: When the job market looks bleak, head to grad school. That’s what happened after the global financial crisis, and early signs suggest it could be happening again. Admissions consultants who guide students through applications, essays and test prep say interest is climbing fast. Official numbers won’t be in for months, but firms like Kaplan, Ivy Coach, IvyWise, Top Tier Admissions and Cambridge Coaching all expect a big year. “The number one influencer of students thinking about grad school is either an economic downturn or economic uncertainty,” said Jayson Weingarten, senior admissions consultant at Ivy Coach. “Students think that will be a good relaunch when the job market picks up.” op-line figures for US employment remain solid, but a “low hiring, low firing” job market has made it harder for younger workers to find employment. The jobless rate for those ages 20 to 24 was at 7.5% last month, up 2 percentage points from a low in April 2023, and anxieties are running high. Many fear artificial intelligence is making scores of white-collar jobs obsolete, while others anticipate a trend towards degree inflation in job postings could be on the horizon if the economy were to fall into a recession from the president’s trade war.” [Bloomberg, 2025-04-12]

Tariffs

Goldman Sachs Economics: Trump’s Tariffs Could Increase U.S. Manufacturing Employment By Almost 100 Thousdand, But At The Cost Of More Than 500 Thousand Other Jobs. According to Bloomberg, “Goldman Sachs economists led by Jan Hatzius have taken a look through history and academic studies to examine whether Trump’s tariffs will succeed in reviving domestic manufacturing employment. While the range of estimates is wide, studies find a 10 percentage point increase in tariff rates raises employment in protected industries by 0.2-0.4%, but that each 1 percentage point increase in tariff-driven costs lowers employment by 0.3-0.6%. ‘Scaling these estimates to the US economy imply a boost of just under 100k to manufacturing employment from tariff protection but a roughly 500k drag on downstream employment from input cost pressures,’ the Goldman economists” [Bloomberg, 2025-04-14]

Cros Employees Were Urged By CEO Andrew Rees To Manage Expenses Closely As The Board Agreed To “Establish More RElaistic Targets For Our Internal Incentives Plan.” According to Bloomberg, “Crocs Inc. employees were urged to closely manage their expenses as the company grapples with supply chain ‘volatility’ caused by President Donald Trump’s trade war, according to the contents of a memo seen by Bloomberg. The note, which was said to have been sent Thursday by Chief Executive Officer Andrew Rees, said staff should ‘remain prudent for the remainder of the year’ and be thoughtful about travel and which initiatives to prioritize. The memo also said that the board’s compensation committee ‘has agreed to establish more realistic targets for our internal incentives plan’ as a result of the economic environment. Crocs, known for its clogs, is one of several retailers that have started to sound alarms over the impact of Trump’s policies, including on-again, off-again tariffs against countries that are key production hubs for the industry. Some companies are withdrawing financial guidance, while others have added tariff-related surcharges or frozen hiring. Broomfield, Colorado-based Crocs produces about half of its name-brand shoes in Vietnam, which got a 90-day reprieve this week from 46% tariffs. The company also has third-party manufacturers in China, where US levies have been hiked to 145%. ‘Given the state of the escalating and uncertain tariff environment, we are focused on managing our business prudently to maximize shareholder value over the medium to long-term,’ a Crocs spokesperson said in an emailed statement.” [Bloomberg, 2025-04-11]

Retaliation

April 2025: China Raised Tariffs On American Imports To 125 Percent. Combining Trump’s Levies, Trade Between The Two World’s Two Largest Economies Became Almost Prohibitively Expensive. According to Bloomberg, “China retaliated against Donald Trump’s latest tariffs by hiking duties on all US goods, while calling the administration’s actions a ‘joke’ and saying it no longer considers them worth matching. Beijing will raise tariffs on all US goods from 84% to 125% starting April 12, the Ministry of Finance said on Friday, after the White House clarified that levies on Chinese goods rose to 145% this year. ‘Given that American goods are no longer marketable in China under the current tariff rates, if the US further raises tariffs on Chinese exports, China will disregard such measures,’ according to the statement. With tariffs at levels now set to halt most all trade between the world’s biggest economies, the concern now is that the economic fight could spill into other areas of the relationship. Trump and Xi are locked in a standoff over who will move to deescalate first: Trump has said he’s ‘waiting’ for a call from Beijing, while Chinese officials have repeatedly said they”re open to negotiations but won’t be bullied into talking.” [Bloomberg, 2025-04-11]

Unintended Consequences

Trump’s CPB Guidelines Suggest That Imported Goods Will Have Tariffs Assessed On Them By The Country Of Final Manufacture, Making Arbitrage Opportunities Possible. According to the Financial Times, “The US Customs and Border Protection, the US federal agency that enforces trade regulations, has published some initial guidance on how the new tariffs will be implemented. It says exporters will need to break down the contents of the articles they are exporting, differentiating between US inputs — which enter tariff-free — and non-US inputs, which must pay the new tariffs at a rate that depends on where the goods were manufactured. Beyond US and non-US inputs, though, tariff rates are not broken down by the proportion of a product that comes from different countries, but determined by the final country of manufacture. However Anna Jerzewska, founder of Trade and Borders consultancy, said that unlike in a bilateral trade deal — when the rules are explicitly set out as part of the agreement — for the so-called non-preferential rules of origin used outside such deals, the details were much less clear. ‘With these non-preferential rules of origin it is much less certain and US Customs determine[s] it based on its own interpretation,’ she said.” [Financial Times, 2025-04-08]

The Complexity Of Proving The Origin Of Components May Encourage Companies To Cut American Inputs Out Of Production, Preferring To Simply Pay The Tariffs. According to the Financial Times, “Trade experts say this is hard to predict, but warn that many companies may simply prefer to pay the tariffs rather than endure the cost and complexity of working out how much of their content is US and non-US. This is despite the heavy potential burden of the tariffs, which have sent global markets plunging. Proving the origin of entirely non-US goods is not simple either. Lawrence Friedman, customs lawyer and a partner at Chicago law firm Barnes, Richardson & Colburn LLP, said determining that a product had been sufficiently ‘transformed’ to qualify for a particular country’s tariff was subject to uncertainty. ‘It’s not a difficult process in itself, but it is subject to some subjectivity and vagaries. Someone can make an informed declaration of origin that customs just disagrees with,’ he said.’A decision can turn on which component makes the”essence” of a finished good, but “essence” is a slippery term.’” [Financial Times, 2025-04-08]

Fiscal Contraction

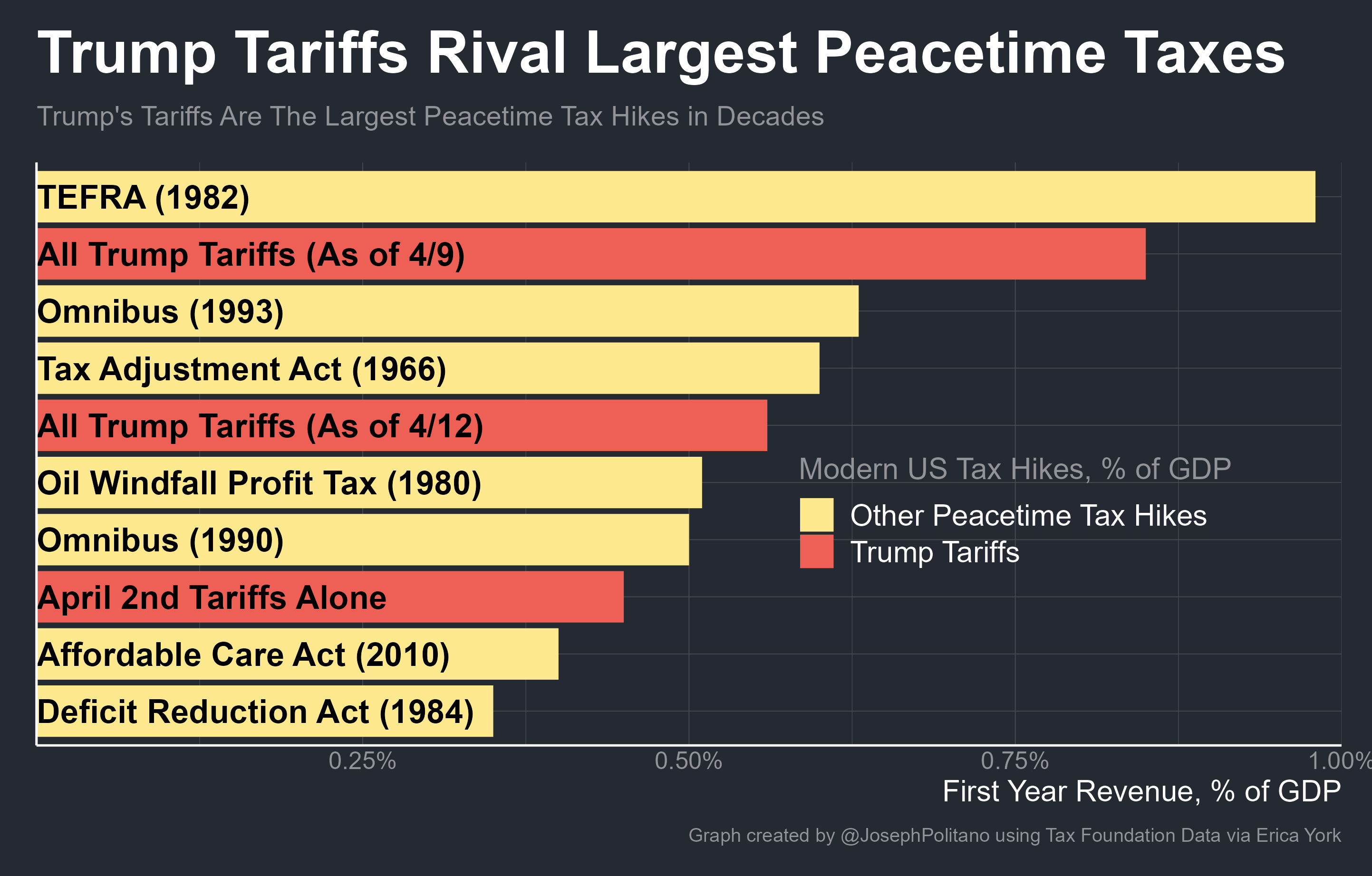

Apricitas Economics: As A Percentage Of Output, Trump’s Tariffs Increased Taxes By More Than Any Legislation Since The 1982 Rollback Of Some Of The Kemp-Roth Tax Cuts. According to Apricitas Economics, “Yet it’s also just worth mentioning the sheer size of Trump’s tariff hikes in fiscal terms—they are among the largest peacetime tax hikes in American history. Analysis from the Tax Foundation estimates that total tariffs will increase federal revenues by about 0.56% of US GDP if sustained, and the April 2nd announcement alone would have increased revenues by 0.45%. For context, the passage of the Affordable Care Act in 2010 caused a smaller net increase in tax revenues than Trump did last week. If a more sensible tax like a VAT or income tax was implemented with similar scale, suddenness, and volatility, it would still be a major shock to the macroeconomy—but Trump has manifested this entirely through an unprecedented increase in some of the most economically distortive taxes in existence. Plus, these revenue estimates understate the impact of the tariff hikes—taxes on Chinese imports are now so large that the US will collect vanishingly little revenue from them given the likely total collapse in trade volumes.” [Apricitas Economics, 2025-04-12]

Despite The Attempt To Target The Chinese Economy, Chinese Comporate Bond Yields Have Actually Declined. According to Bloomberg, “The global market volatility that followed Donald Trump’s April 2 tariff announcement is comparable only to the worst days of October 2008 and March 2020. Yet, credit markets in China, the main target of the trade war waged by the US administration, haven’t flinched. While US and European credit gauges saw some wild swings in recent days, with Treasuries also in the spotlight, China’s local bond markets so far have dodged any panic selling and gained instead. Average yield of the country’s benchmark three-year and top-rated yuan corporate bonds went down by about 12 basis points this month, a China bond index shows, as domestic traders are betting on more monetary easing measures from the government to support the ailing economy. ‘US tariffs” direct impact on Chinese credit markets have so far been quite contained,’ according to analyst Chang Wei Liang, a forex and credit strategist at DBS Group Research. China’s credit is ‘underpinned by state support’ and most companies are not exposed to trade, he wrote in a note. Spreads on Chinese bonds widened by about 30 basis points since the end of March — a level in line with peers in Asia.” [Bloomberg, 2025-04-12]

Antagonizing America’s Allies Has Left China An Opening

Frustrated European Leaders Have Grown More Open To China, With An EU-China Summit Now Being Planned For July 2025. According to the Wall Street Journal, “Instead of hewing closer to Washington’s line, voices are growing in Europe for a reversal of the EU’s China policy, which has increasingly aligned itself with American moves to deny China modern technologies and investment opportunities. Ursula von der Leyen, president of the European Commission, spoke with Chinese Premier Li Qiang shortly after Trump’s tariffs were imposed, and an EU-China summit is being planned for July. Meanwhile, the EU and China last week agreed to restart talks to settle a dispute over Chinese electric-vehicle imports, which the bloc hit with tariffs a few months ago. Spanish Prime Minister Pedro Sánchez, ahead of his visit to Beijing on Friday, called for Europe to review its relationship with China as it adapts to the new reality. His statement provoked a rebuke from Bessent, who warned that cooperating with Beijing would be ‘cutting your own throat.’ Chinese leader Xi Jinping had a different reaction as he welcomed Sánchez. Europe and China, he said, must ‘jointly safeguard economic globalization and the international trade environment, and jointly resist unilateral and bullying actions.’” [Wall Street Journal, 2025-04-14]

Despite China’s Support For Russia, Recent American Moves Have Forced Europe To Approach Them. According to the Wall Street Journal, “European relations with China were poisoned over the past three years by Beijing’s support for Russia, which wouldn’t have been able to prosecute its war on Ukraine without Chinese diplomatic and economic backing. While that assistance continues, on the diplomatic front something unthinkable happened in recent months: Russia and the U.S. voted against a United Nations resolution on Ukraine, while China abstained and criticized Washington for excluding Europe from peace negotiations. As the post-World War II rules-based order morphs into empires with spheres of influence, Europe must balance against both Russia and America—and only China could provide that counterweight, said Bernard Guetta, a French member of the European Parliament. Even a full-blown political alliance between Europe and Beijing could emerge over time if the U.S. doesn’t change its course, he said. ‘A Chinese question exists now because the new U.S. administration not only hasn’t made a single friendly gesture toward the EU, but has only made unpleasant and unsettling ones,’ said Guetta, a critic of the Chinese Communist Party. ‘This doesn’t mean that we suddenly have to praise the Chinese regime. But there are historical precedents—Roosevelt and Churchill once relied on Stalin, and that doesn’t mean that they converted to Communism.’” [Wall Street Journal, 2025-04-14]

Uncertainty

Apricitas Economics: The Wild Fluctuations In Tariff Rates, “An Insane Way To Run An Economy” According to Apricitas Economics, “It should go without saying that this is an insane way to run the world’s largest economy. Imagine being a US solar panel importer, panicking because most of your goods come from Southeast Asian nations like Vietnam and Thailand threatened with insane tariffs. After April 2nd, you rush out to import as much as you can before a 36% effective tariff increase takes effect April 9th, only to have the tariffs reduced by 26% the next day. Or imagine being an electronics retailer, already facing tariffs of 16% on imported game consoles that mostly come from China. You brace for an expected 32% tariff increase based on the April 2nd tariff rates, instead receive a 61% tariff hike because China tariffs were increased further, and then receive another 27% tariff hike the next day even when most other imports saw tariff relief. Or imagine being that same electronics retailer, panicking about the effects of tariffs on your cell phone imports, watching tariffs accelerate up to 65% amid the China trade war, only for the White House to quietly publish an addendum yesterday exempting smartphones, computers, and parts from all of the tariffs imposed since April 2nd.” [Apricitas Economics, 2025-04-12]

Uncertainty Over Apple Exemptions

April 11, 2025: CPB Posted An Exemption For “Computers, Tablets, Apple Watches, Computer Monitors, Semiconductor Equipment, And Other Electronics.” According to the Wall Street Journal, “Tech investors briefly rejoiced when a notice from U.S. Customs and Border Protection posted late Friday said computers, tablets, Apple watches, computer monitors, semiconductor equipment and other electronics were exempt from many tariffs on Chinese products and a 10% tariff on all U.S. imports.” [Wall Street Journal, 2025-04-13]

April 13, 2025: Trump Posted That “There Was No Tariff ‘Exemption.’” According to the Wall Street Journal, “Administration officials on Sunday, including Commerce Secretary Howard Lutnick, said the tech products exempted from many tariffs will face separate levies in a month or two as part of a trade investigation into semiconductors. White House trade adviser Peter Navarro said Sunday the official policy is ‘no exemptions, no exclusions.’ ‘There was no tariff “exception” announced on Friday,’ Trump said on his Truth Social platform Sunday, adding that the products will be in the separate tariff bucket with semiconductors.” [Wall Street Journal, 2025-04-13]

WSJ Editorial Board: Trump’s Tariffs “Favor The Powerful And Politically Connected” And “Make American Companies Less Globally Competitive”

WSJ Editorial Board: “Tariffs Are Advertised In The Name Of Helping American Workers, But What Do You Know? They Turn Out To Favor The Powerful And Politically Connected.” According to the Wall Street Journal Editorial Board, “Tariffs are advertised in the name of helping American workers, but what do you know? They turn out to favor the powerful and politically connected. That’s the main message of President Trump’s decision to exempt smartphones and assorted electronic goods from his most onerous tariffs. Customs and Border Protection (CBP) late Friday issued a notice listing products that will be exempt from Mr. Trump’s so-called reciprocal tariffs that can run as high as 145% on goods from China. The exclusions apply to smartphones, laptop computers, hard drives, computer processors, servers, memory chips, semiconductor manufacturing equipment, and other electronics.” [Wall Street Journal Editorial Board, 2025-04-13]

WSJ Editorial Board: “It Is No Credit To The Trump Administration To Have A Commerce Secretary Who Knows So Little About Modern Commerce.” According to the Wall Street Journal Editorial Board, “The Trump exemptions carry several lessons that vindicate tariff critics. One is a rebuttal of the fantasy pitched by Commerce Secretary Howard Lutnick to CBS News that an ‘army of millions and millions of human beings screwing in little, little screws to make iPhones, that kind of thing is going to come to America’ and be automated. Guess not. As CEOs and these columns have argued, there aren’t nearly enough American workers who could do that work. And even if there were, most of the economic value-added doesn’t come from final-stage assembly. It comes from design and higher-end component supply. It is no credit to the Trump Administration to have a Commerce secretary who knows so little about modern commerce. Oh, and on Sunday Mr. Lutnick said the tariffs on electronics could go up again in the coming months. The exemptions also expose the fiction that foreign exporters pay the bulk of tariff costs. If that were true, China would absorb the cost and U.S. consumers wouldn’t pay more. No exemptions would be needed. Mr. Trump wants the exemptions to avoid the political blame for rising prices on high-profile products.” [Wall Street Journal Editorial Board, 2025-04-13]

WSJ Editorial Board: The Trump Administration’s Behavior Was “A Tacit Admission That Tariffs Will Make American Companies Less Globally Competitive, Especially In The Artificial Intelligence Race.” According to the Wall Street Journal Editorial Board, “The exemptions also expose the fiction that foreign exporters pay the bulk of tariff costs. If that were true, China would absorb the cost and U.S. consumers wouldn’t pay more. No exemptions would be needed. Mr. Trump wants the exemptions to avoid the political blame for rising prices on high-profile products. This is also a tacit admission that tariffs will make American companies less globally competitive, especially in the artificial intelligence race. That explains the exemptions for ASML’s chip-making equipment and Nvidia’s graphic processing units. Mr. Trump first makes U.S. companies less competitive, then he and his Administration, in their unerring wisdom, pick exceptions worthy of help to remain competitive. Politicians, not success in the marketplace, pick business winners and losers.” [Wall Street Journal Editorial Board, 2025-04-13]

Capital Flight

Bloomberg: Trading Patterns In The U.S. Are Similar To Those In Emerging Markets. According to Bloomberg, “That masks a fundamental shift that has taken hold among investors, traders and analysts. Serious questions now exist around the wisdom of owning American assets that until recently were the envy of a risk-obsessed world. Amid the manic moves, key trading patterns even bear soft echoes with emerging markets. All told, fear is spreading that Trump’s bid to rewrite the terms of global trade risks imperiling America’s privileged status in the financial system.” [Bloomberg, 2025-04-11]

Code

include("../scripts/oxocarbon-plot.jl")usingYFinance, DataFrames, Dates, StatsPlotstheme(:oxocarbon)t10y =get_prices("^TNX"; interval="1d", startdt=Date("2005-04-12"), enddt=Date("2025-04-12")) |> DataFrameusd =get_prices("^NYICDX"; interval="1d", startdt=Date("2005-04-12"), enddt=Date("2025-04-12")) |> DataFramet10y.chg = (t10y.close .- t10y.open)./t10y.openusd.chg = (usd.close .- usd.open)./usd.opentreasury =DataFrame(date=Date.(t10y.timestamp), t10y=t10y.chg)usd =DataFrame(date=Date.(usd.timestamp), usd=usd.chg)df =leftjoin(usd, treasury, on=:date)# Build a clean dataframe of all of these values #=df = DataFrame(date=t10y.timestamp, t10y=(t10y.close .- t10y.open)./t10y.open,usd=(usd.close .- usd.open)./usd.open)=## Create a dataframe of the data after April 2, 2025liberation =filter(row -> row.date >Date("2025-04-02"), df)cap_flight(x,y) = x >0&& y <0# Calculate the share of capital flight days for each periodpre_cap_flight =100.0*sum(cap_flight.(df.t10y, df.usd)) /size(df, 1)post_cap_flight =100.0*sum(cap_flight.(liberation.t10y, liberation.usd)) /size(liberation, 1)# Plot the changes against each otherscatter(df.t10y, df.usd, xlabel ="Treasury Yield Change", ylabel ="USD Change", label ="Pre-Tariffs", alpha =0.1, title="April 12, 2005 - April 12, 2025")scatter!(liberation.t10y, liberation.usd, xlabel ="Treasury Yield Change", ylabel ="USD Change", label ="Post-Tariffs")hline!([0], label ="", linestyle =:dash, color =:black)vline!([0], label ="", linestyle =:dash, color =:black)

Over the last two decades, 19.86 percent of days have seen higher bond yields and a weaker dollar. Since “Liberation Day,” that has been true on 42.86 percent of days.

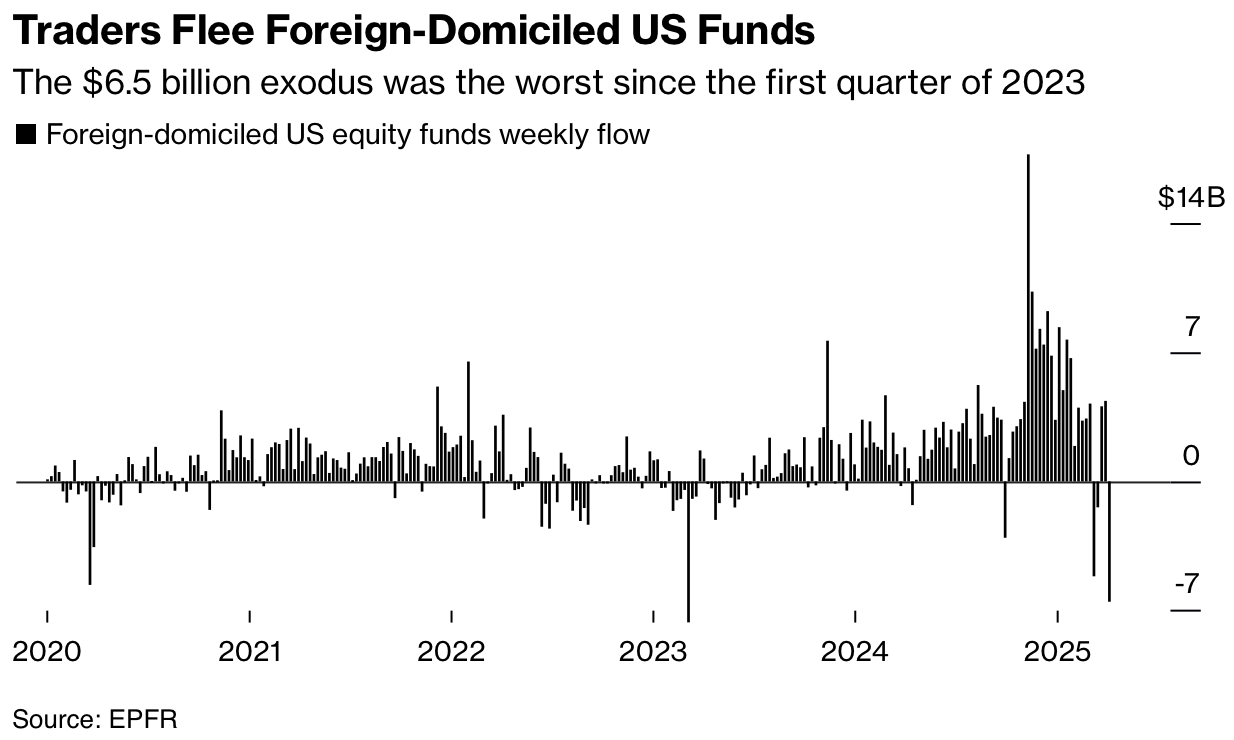

The $6.5 Billion Withdrawn From Foreign-Domiciled U.S. Equity Funds Was The Worst In Two Years. [Bloomberg, 2025-04-11]

WSJ: The Simple Explination For The Treasury Market: “Investors Don’t Want To Buy It.” According to the Wall Street Journal, “The Treasury market freaked everyone out this week when yields on longer-term debt shot higher even as stocks were being bludgeoned and the dollar fell. Naturally, traders are wondering why. The immediate suspects include somewhat plausible ideas revolving around complex trading strategies employed by hedge funds to conspiracy theories focused on nefarious dealings by foreign governments. But the answer might be far simpler: U.S. government debt is doing badly because, well, investors don’t want to buy it.” [Wall Street Journal, 2025-04-11]

The Change In Treasury Futures Would Not Be Sufficent To Lead To A Basis Trade Blowup. According to the Wall Street Journal, “It isn’t surprising that befuddled investors would reach for more complicated answers. It is a natural instinct when things take an unexpected turn. The biggest boogeyman is the “Treasury basis trade.” Torsten Slok, chief economist at Apollo Global Management, has estimated this at around $800 billion. It involves hedge funds buying bonds while selling futures contracts linked to them to asset managers. The managers often want to be more exposed to higher-yielding corporate debt yet use the derivatives to give them exposure to risk-free Treasury returns. This strategy went pear-shaped during the market rout of March 2020, when the prices of the futures sold by hedge funds held up better than those of the Treasurys they had bought. The resulting unwind caused a selloff in government bonds. This time, a similarly huge impact looks unlikely. Data from JPMorgan shows that futures did get a bit more expensive between April 2 and April 8 relative to both actual Treasury debt and market interest rates. But the increase was small.” [Wall Street Journal, 2025-04-11]

Indicators Of Continued Equity Weakness

Following The 15 Largest S&P 500 Gains (Of Which Last Wednesday Was One), It Was Higher Six Months Ahead Less Than Half The Time. A Far Cry From The 67 Percent Chance On Any Day Going Back To 1928. According to Bloomberg, “A knee-jerk reaction to President Donald Trump’s 90-day pause on broad tariffs propelled US stocks to one of their best days on record last week. Ironically, that could be a harbinger of tough times for equity investors. The S&P 500 Index’s best days in history have usually preceded weaker-than-average returns in the near term. Following its 15 largest daily gains, the US stock benchmark was higher six months later just 43% of the time, Bloomberg Intelligence data going back to 1928 show. That’s lower than the 67% probability on any given day that the S&P 500 will advance over the subsequent half year.” [Bloomberg, 2025-04-14]

Lawlessness

Following Trump’s Executive Order Allowing Foreign Corrupt Practices, The DOJ Has Backed Away From Enforcing White Collar Crime. According to the Wall Street Journal, “The Trump administration is retreating from some types of white-collar law enforcement, including cases involving foreign bribery, public corruption, money laundering and crypto markets. In some cases, the administration is effectively redefining what business conduct constitutes a crime. Trump’s executive order in February said bribery prosecutions hurt the ability of American companies to compete overseas, punishing them for practices that are routine in some parts of the world. That pronouncement could upend dozens of cases and investigations. At the Justice Department, Attorney General Pam Bondi has ordered prosecutors to focus their anti-money-laundering and sanctions-evasion attention on drug cartels and international crime organizations. A few themes are emerging: Prosecuting executives for wrongdoing that doesn’t have obvious victims is out. The Justice Department is open to arguments that a defendant has been targeted for political reasons, or that some prosecutions undermine economic competitiveness and national-security interests. And political connections within Trump’s world seem to matter.” [Wall Street Journal, 2025-04-13]

The SEC Has Also Stopped Enforcing Some Laws, Especially Against Cryptocurrency Firms. According to the Wall Street Journal, “The Securities and Exchange Commission also enforces the foreign-bribery law. The chief of its Foreign Corrupt Practices Act unit, and his deputy director, were part of a wave of officials who took a buyout offer intended to slim down the 4,500-employee agency. Acting SEC Chairman Mark Uyeda said the agency is reviewing how to proceed in FCPA cases and wants ‘to make sure that we”re uniformly applying and enforcing the laws.’ The SEC also has dropped lawsuits against crypto companies Coinbase and Kraken and trading firm Cumberland DRW. The lawsuits had alleged those companies failed to register with the agency and were operating illegally. The cases were the cornerstone of a Biden administration effort to regulate most cryptocurrencies as securities. The SEC said in a court filing it was pausing a lawsuit against Justin Sun, a Chinese crypto magnate it had accused in March 2023 of market manipulation and fraud. Sun had asked a court to dismiss the claims, saying his firm’s trading was legitimate and his activity took place overseas, leaving the SEC without authority over him. A few weeks after Trump was elected, Sun invested $30 million in crypto company World Liberty Financial, owned by the Trump family.” [Wall Street Journal, 2025-04-13]

Context

The laws these bad actors have violated are still on the books. While the administration has signaled it will not enforce them, there is nothing to stop it from changing its mind, or for a future administration from enforcing them. As a result, it is creating an incentive structure for these firms to support the administration and ensure the continued power of those who will not enforce the law.

Outlook

While research on the pass through of tariff-driven price increases under the first Trump administration generally shows that consumers were spared a good portion of the costs, there is good reason to believe that the same will not be true this time around. One consequence of the pandemic was a corporate embrace of pricing power. Research in the Federal Reserve’s Finance and Economics Discussion Series by Montag and Villar finds that during the post-pandemic inflation, companies raised prices more than many existing models of corporate responses to inflation would predict.

This aligns with a trend best identified by Samuel Rines, who called it “Price over Volume,” where companies saw smaller declines in sales volumes relative to price increases. Part of the reason for the success of this strategy was that earnings and employment were strong, and so consumers were willing to put up with (although they were not happy about them) price increases in goods they wanted.

There are two reasons to think that this will not be the case this time around. First of all, if the economy weakens, as most consumers seem to think it will, they will not have the spending power to support higher prices. Secondly, the increases in input prices producers are facing from Trump’s Tariffs is larger than than the increase driven by the post-pandemic inflation. The annual increase in producer prices for supermarkets and grocery stores was 18.8 percent in October 2022. That is a far cry from the 145 percent tariff on imports from China, some of which cannot be substituted quickly.

This means that the post-2018 trend of companies sparing consumers the costs of Trump’s tariffs is unlikely to be repeated.

[Apricitas Economics,

[Apricitas Economics,  [Bloomberg,

[Bloomberg,