April 16, 2025

Macrofinancial Outlook for the Day

Releases

Retail Sales

Industrial Production and Capacity Utilization

March 2025: Industrial Production Decreased 0.3 Percent, Led By A Decline In Utilities Due To Good Weather. Year Over Year, It Increased 1.3 Percent. According to the Federal Reserve, “Industrial production (IP) decreased 0.3 percent in March but increased at an annual rate of 5.5 percent in the first quarter. The March decline was led by a 5.8 percent drop in the index for utilities, as temperatures were warmer than is typical for the month. In contrast, the indexes for manufacturing and mining grew 0.3 percent and 0.6 percent, respectively. At 103.9 percent of its 2017 average, total IP in March was 1.3 percent above its year-earlier level. Capacity utilization stepped down to 77.8 percent, a rate that is 1.8 percentage points below its long-run (1972–2024) average.” [Federal Reserve, 2025-04-16]

March 2025: Capacity Utilization Dropped To 77.8 Percent, 1.8 Percent Below Its Long-Run Average. According to the Federal Reserve, “Industrial production (IP) decreased 0.3 percent in March but increased at an annual rate of 5.5 percent in the first quarter. The March decline was led by a 5.8 percent drop in the index for utilities, as temperatures were warmer than is typical for the month. In contrast, the indexes for manufacturing and mining grew 0.3 percent and 0.6 percent, respectively. At 103.9 percent of its 2017 average, total IP in March was 1.3 percent above its year-earlier level. Capacity utilization stepped down to 77.8 percent, a rate that is 1.8 percentage points below its long-run (1972–2024) average.” [Federal Reserve, 2025-04-16]

Home Builder Confidence Index

April 2025: Homebuilder Confidence Recovered Slightly, But Remained Pesimistic. According to the National Association of Home Builders, “Each month, the HMI depicts overall builder sentiment toward housing market conditions on a scale ranging between 0 and 100. A higher reading (>50) is an indication that the majority of builders feel confident about the current and near-term outlook for housing. Lower readings signify less optimism among builders. Builder confidence in the market for newly built single-family homes was 40 in April, edging up one point from March. Here are the readings for the three HMI indices in April: Current sales conditions rose two points to 45. Sales expectations in the next six months fell four points to 43. Traffic of prospective buyers increased one point to 25. The latest HMI survey also revealed that 29% of builders cut home prices in April, unchanged from March. Meanwhile, the average price reduction was 5% in April, the same rate as the previous month. The use of sales incentives was 61% in April, up from 59% in March.” [National Association of Home Builders, 2025-04-16]

April 2025: While Current Sales Conditions Improved, Future Expectations Fell. According to the National Association of Homebuilders, “Each month, the HMI depicts overall builder sentiment toward housing market conditions on a scale ranging between 0 and 100. A higher reading (>50) is an indication that the majority of builders feel confident about the current and near-term outlook for housing. Lower readings signify less optimism among builders. Builder confidence in the market for newly built single-family homes was 40 in April, edging up one point from March. Here are the readings for the three HMI indices in April: Current sales conditions rose two points to 45. Sales expectations in the next six months fell four points to 43. Traffic of prospective buyers increased one point to 25. The latest HMI survey also revealed that 29% of builders cut home prices in April, unchanged from March. Meanwhile, the average price reduction was 5% in April, the same rate as the previous month. The use of sales incentives was 61% in April, up from 59% in March.” [National Association of Homebuilders, 2025-04-16]

April 2025: Homebuilders Offering Sales Jumped. According to the National Association of Homebuilders, “Each month, the HMI depicts overall builder sentiment toward housing market conditions on a scale ranging between 0 and 100. A higher reading (>50) is an indication that the majority of builders feel confident about the current and near-term outlook for housing. Lower readings signify less optimism among builders. Builder confidence in the market for newly built single-family homes was 40 in April, edging up one point from March. Here are the readings for the three HMI indices in April: Current sales conditions rose two points to 45. Sales expectations in the next six months fell four points to 43. Traffic of prospective buyers increased one point to 25. The latest HMI survey also revealed that 29% of builders cut home prices in April, unchanged from March. Meanwhile, the average price reduction was 5% in April, the same rate as the previous month. The use of sales incentives was 61% in April, up from 59% in March.” [National Association of Homebuilders, 2025-04-16]

GDP Now

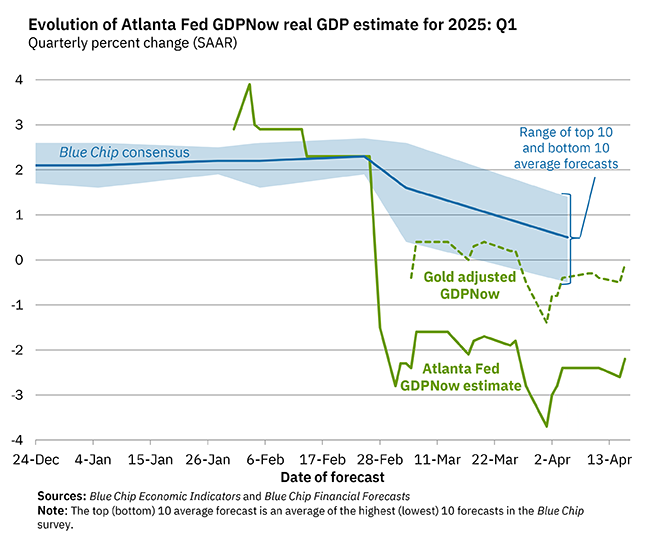

GDP Now: The Updates To Industrial Production, Retail Sales, And Capacity Utilization Increased Forecast Q1 2025 Real GDP Growth To -0.1 Percent (-2.2 Percent Not Adjusting For Gold) According to the Atlanta Federal Reserve,  [Atlanta Federal Reserve, 2025-04-16]

[Atlanta Federal Reserve, 2025-04-16]

Context: The Recession Did Not Begin In Q1, But A Narrative Could be Taking Hold

The accounting identity for GDP (\(Y\)) is: consumption (\(C\)), investment (\(I\)), government spending (\(G\)), and net exports (\(X_n\)): \[ Y = C + I + G + X_n \] but, like almost all accounting identities, it does not tell you much of anything when thinking about why things happen.

In reality, almost all economic fluctuations happen with consumption and investment. But neither is a single category.

The easiest way to break up goods consumption is between durable and non-durable goods. Non-durable goods are things like groceries, which need to be purchased regularly, and cannot be avoided, no matter how dire the economic situation. That is why when you look at the plot of retail sales, the monthly change in grocery consumption is much less volatile than the overall retail sales number.

When households are feeling a pinch, they may go to a cheaper store, but they will not go without food.

Durable goods, on the other hand, last and as a result households have much more discretion over when to purchase them. The canonical durable good is a car. When households are cautious about the future, they are more likely to use the car they have for longer. As a result, durable goods consumption is much more volatile, and is a useful leading indicator about how households are feeling.

Therefore, the result reported today that in March, that automotive sales surged should appear a positive sign. Unfortunately, however, there is strong evidence that much of this consumption was by households looking to bring forward a purchase before tariffs on automotive inputs were in effect.

This is backed up by the story told in industrial production and capacity utilization. Industrial production is a good indicator of output. In fact, when economists model the economy with monthly variables, industrial production is often used as a proxy for GDP. It is, however, a leading indicator. It generally takes some time for goods that are produced to be consumed. That it fell in March indicates productive businesses are not expecting the current increase in demand to last.

This is borne out by the fall in capacity utilization. What economists call productive capital, of the capacity that businesses have to produce depreciates in two economically relevant ways: over time, and through use. This is a source of investment demand by businesses, that need to replace depreciated capital. Declining utilization, therefore, reduces the use-based demand for capital investment.

These signs indicate an economic slowdown.

Leading Indicators

WSJ Headline: Canadians Are Cashing Out Their American Vacation Homes [Wall Street Journal, 2025-04-13]

Scottsdale Arizona: The Number Of Canadians Selling Homes Increased By A Factor Of Around Seven, While The Number Of Candian Buyers Has Declined By 40 Percent.. According to the Wall Street Journal, “In the greater Phoenix area, there has been a dramatic increase in Canadians selling their property, says Miles Zimbaluk, a real-state agent with HomeSmart in Scottsdale, Ariz. Such listings climbed to around 700 in January through March, up from around 100 at the same time last year, according to Zimbaluk’s review of tax records. He says he has also seen a 40% decline in the number of Canadians buying property in Arizona during that period.” [Wall Street Journal, 2025-04-13]

Canadians Have Long Been The Largest Share Of Foreign Homeowners In The United States. According to the Wall Street Journal, “It’s a big shift after Canadians have long made up the largest share of foreign residential real-estate buyers in the U.S. They accounted for an average of 23% of foreign purchases from 2010 to 2013, and were still the largest segment at 13% last year, according to the National Association of Realtors.” [Wall Street Journal, 2025-04-13]

Context

When foreign owners of real estate sell their holdings, there is a significant chance they will take their money out of the country, especially when the dollar is weakening as it is now. Unless they sold to another foreign buyer, this results in a net capital outflow, which weakens the dollar.

Under normal circumstances, this would make American exports more competitive on the global marketplace, attracting foreign investment, but we are currently doing whatever we can to make the United States a less attractive place to put capital right now.

Tariff Stuff

April 2025: Trump Announced A Section 232 Investigation Into “Critical Minearals.” According to Bloomberg, “President Donald Trump has launched a probe into the need for tariffs on critical minerals, the latest action in an expanding trade war that has targeted key sectors of the global economy. The order, which Trump signed on Tuesday, calls for the commerce secretary to initiate a Section 232 investigation under the Trade Expansion Act of 1962 to ‘evaluate the impact of imports of these materials on America’s security and resilience,’ according to a White House fact sheet. If the secretary finds that the imports threaten to ‘impair national security and the President decides to impose tariffs,’ those levies would take the place of current so-called reciprocal duties Trump announced earlier this month on US trading partners. The order covers a range of minerals, including rare earth elements, that the US government considers ‘building blocks of our defense industrial base’ and crucial to building jet engines, missile guidance systems, advanced computers, as well as radar, optics and communications equipment. The order also covers uranium, as well as processed forms of the minerals and derivative products.” [Bloomberg, 2025-04-15]

- One Day Before The Order, The Chinese Government Suspended Exports Of Those Minearls. According to the New York Times, “China has suspended exports of a wide range of critical minerals and magnets, threatening to choke off supplies of components central to automakers, aerospace manufacturers, semiconductor companies and military contractors around the world. Shipments of the magnets, essential for assembling everything from cars and drones to robots and missiles, have been halted at many Chinese ports while the Chinese government drafts a new regulatory system. Once in place, the new system could permanently prevent supplies from reaching certain companies, including American military contractors.” [New York Times, 2025-04-13]

Uncertainty

The Trump Administration Barred Nvida From Selling Its H20 Chips To Chinese Buyers. According to Bloomberg, “resident Donald Trump’s administration has barred Nvidia Corp. from selling its H20 chip in China, an escalation of Washington’s tech battle with Beijing that will cost the company billions of dollars and hamstring a product line it explicitly designed to comply with previous US curbs. The US government informed Nvidia on Monday that the H20 would require a license to export to China ‘for the indefinite future.’ The new rules address Washington’s concerns that ‘the covered products may be used in, or diverted to, a supercomputer in China,’ the company said in a filing. Nvidia warned it will report about $5.5 billion in writedowns during the current quarter, tied to inventory and commitments for the chip.” [Bloomberg, 2025-04-15]

- One Week Before, The Trump Administration Had Backed Off A Threat To Do Just That After Nvidia CEO Jensen Huang Attened A $1 Million-A-Head Dinner At Mar-A-Lago. According to NPR, “When Nvidia CEO Jensen Huang attended a $1 million-a-head dinner at Mar-a-Lago last week, a chip known as the H20 may have been on his mind. That’s because chip industry insiders widely expected the Trump administration to impose curbs on the H20, the most cutting-edge AI chip U.S. companies can legally sell to China, a crucial market to one of the world’s most valuable companies. Following the Mar-a-Lago dinner, the White House reversed course on H20 chips, putting the plan for additional restrictions on hold, according to two sources with knowledge of the plan who were not authorized to speak publicly. The planned American export controls on the H20 had been in the works for months, according to the two sources, and were ready to be implemented as soon as this week.” [NPR, 2025-04-09]

Automotive Companies Have Been Hurt By The Fact That No One In The Trump Administration Defined “U.S. Content” When Creating A Tariff Exemption. According to the Wall Street Journal, “The White House sought to give car companies a break on a hefty auto tariff enacted this month by offering a deduction for American-made parts. The problem is industry executives are puzzled over how to collect it. And that is in large part because it hinges on a simple yet loosely defined phrase they are struggling to interpret: ‘U.S. content.’ When President Trump enacted the 25% tariff on all vehicle imports, he gave automakers some relief: They would be allowed to pay a lower tariff based on the percentage of U.S.-produced parts and materials used in a foreign-built vehicle. The White House, however, has yet to provide many details on what exactly constitutes ‘U.S. content’ or how it might be determined, for now leaving it up to the companies to figure it out on their own. Meanwhile, they have been left to pay the full tariff. ‘We”re all waiting to better understand how this is supposed to be done,’ said Jennifer Safavian, president and chief executive of Autos Drive America, an industry group representing foreign-based automakers. ‘It’s not really been clear to us.’” [Wall Street Journal, 2025-04-15]

- While Each Vehicle Contained Between 20 And 30 Thousand Individual Parts, The Trump Administration Warned Automakers That Incorrect Calcuations Would Result In Retroactive Tariffs. According to the Wall Street Journal, “The lack of clarity on the U.S.-content provision has triggered frustration and confusion across the auto industry, which imports about 7.5 million vehicles into the U.S. each year. Automakers will need to trace the origin of a lot of components: Safavian noted that each vehicle typically has 20,000-30,000 parts. On the line are billions of dollars in potential savings for General Motors, Toyota Motor and other auto manufacturers that are now paying the tariff on foreign-built vehicles, including those made in Mexico and Canada. The 90-day pause on reciprocal tariffs announced last week doesn’t apply to automotive goods. Company executives say the U.S. content requirements are critical for shaping longer-term decisions, such as whether to raise prices or reroute production. A study published Thursday by the Center for Automotive Research, an Ann Arbor, Mich.-based nonprofit, said the auto-import tariffs could increase costs for automakers by more than $100 billion. Misinterpreting the rules carries some risk: The Trump administration has warned that any company found to have provided inaccurate information on their U.S. content levels could be subject to retroactive tariffs.” [Wall Street Journal, 2025-04-15]

Q1 2025: Frothy Markets Driven By Uncertainty Juiced Big Bank Trading Profits. According to the Wall Street Journal, “Wall Street is raking in even more money from trading than it did during the market’s Covid-19 era swings. Goldman Sachs increase; JPMorgan Chase and Morgan Stanley all said a surge in trading revenue helped lift their profits in the first quarter and beat expectations. Bank trading desks have been collecting more fees from investors scrambling to reduce or dial up the risk in their portfolios on any new clue about how President Trump’s tariffs might ultimately play out. Combined, the three banks earned more than $12 billion in fees in their equities businesses, the desks that run stock-market related activities for clients. That tops the trading boom that followed some of the pandemic’s worst days.” [Wall Street Journal, 2025-04-15]

April 2025: The Treasury Term Premium, A Measure Of Economic Uncertainty, Hit Its Highest Level In More Than A Decade. According to Bloomberg, “The 10-year yield was up two basis points to 4.39% on Tuesday after falling the most since January on Monday. The term premium — the extra return investors require to hold longer notes over shorter ones — rose to 71 basis points, a level last seen in September 2014, according to data from the Federal Reserve Bank of New York referring to last week. Term premiums have been on the rise as US economic policy becomes harder to predict. An index of such uncertainty neared a record this month after President Donald Trump announced sweeping tariffs and then backtracked on some. Proposals for tax cuts and a potential need to increase the US government debt limit also contributed to the move.” [Bloomberg, 2025-04-14]

Term Premium - The Decline In Foreign Demand For Treasuries Likely Worsened The Term Premium. According to Bloomberg, “The US has long benefited from abundant demand from foreigners for its debt, who currently hold about 30% in total. That’s helped compress term premiums and reduce borrowing costs, but the trend is flipping into reverse. ‘The decline in foreign demand for US Treasuries is a paradigm shift in the demand dynamic and recent events could accelerate this trend,’ Societe Generale SA strategists including Subadra Rajappa wrote in a note. That should lead to higher term premium and worsen US deficit projections as net interest outlays climb, they added.” [Bloomberg, 2025-04-14]

Apology To The Basis Trade

Tracy Alloway: “Why Keep Buying Debt Securities Issued By A Government Which Seems Hellbent On Divorcing Itself From The Global Economy ANd Potentially The Entire Global Financial System?” A Decline In Real Demand, Rather Than The Basis Trade Likley Led To The Increase In Rates Following The Tariffs. According to Bloomberg, “Now that the dust is settling on last week’s historic selloff in bond markets and we’re starting to get some additional info from the CFTC, TRACE etc., I think it’s worth revisiting what actually just happened in bond markets. This is important because if we want to know where we’re heading, we need to understand where we’re coming from (Especially true in Trump’s America, where the rapidity of the news cycle means that we’re at real risk of forgetting what happened just a week ago. SignalGate anyone?) So here’s my autopsy, as it stands, of last week’s bond market crash. Whenever weird things happen in what’s supposed to be the world’s most boring market — bonds — basis trades put on by hedge funds and other active managers, make for pretty good villains. Overlevered, overpaid, and overhere, the trades thrive in opacity. Like the proverbial pod shop that is always blowing up somewhere, they’re convenient scapegoats to blame when stuff starts getting hairy. They are also, as discussed in last week’s newsletter, hard to gauge in terms of size. This is the case even after regulators have complained about basis trade risks for the past five years — ever since the 2020 blow-up ended with massive intervention by the Federal Reserve. And so, it makes sense that when the bond market was going nuts last week, everyone initially reached for the 2020 pandemic parallel to explain what was going on. There were anecdotes of repo capacity being constrained, liquidity in the Treasury market deteriorating — all of these things were believed to be a tell-tale sign of another basis trade blow-up. Now, with the benefit of hindsight and data from the CFTC and TRACE, the role of basis trade blow-ups in the bond market selloff seems to have been vastly overestimated. Yes, repo funding was clearly constrained last week but not, crucially, because of basis trades alone. Instead, as previously mentioned in this space, there were a couple other things going on. […] At the same time, real money investors seemed to be heading to the door en masse. After all, why keep buying debt securities issued by a government which seems hellbent on divorcing itself from both the global economy and potentially even the entire financial system? […] The result was constrained repo funding and Treasury market illiquidity as investors headed for the doors all at once and broker-dealer balance sheets got clogged. Basis trades weren’t the proximate cause of all the madness, they were merely the first step on the totem pole of one almighty retreat.” [Bloomberg, 2025-04-14]

┌ Warning: Metadata 'notes' not returned from server.

└ @ FredData ~/.julia/packages/FredData/5M7x4/src/get_data.jl:77Citigroup: The Increase In SOFR Volumes Following The Tariff Announcement Indicated Real Money Leaving Treasuries. According to Bloomberg, “There was a perfect storm of swap spread long deleveraging, due to a combination of carry and deregulation positioning, combined with outright selling by multiple types of investors. There is clear evidence when looking at the very large TRACE Treasury volumes but most important is that SOFR volumes are up about $200 billion from the last week of March. This indicates that real money accounts, not just levered accounts, have been stopped out of positions.” [Bloomberg, 2025-04-14]

Context: What the SOFR Market Tells Us

The volume measurement in the plot above shows the daily dollar amount of transactions in the overnight Treasury repo market. As can be seen, there are typical seasonal patterns in the data, with volumes surging toward the middle and end of each month, as these are common dates for short term borrowing needs, either to finance payrolls, contractual obligations, or derivative related activities.

What Citi noted about the Post-Tariff spike is that when long-term holders of treasuries sell in high volume, they usually sell to treasury dealers, who are often have the balance sheets most capable of absorbing those holdings. But those dealers don’t keep the cash directly on hand. Rather, they meet their short term financing needs by borrowing, often in the overnight repo market. The spike in SOFR volumes likely indicates that these dealers were securing more short-term funding to purchase those offloaded treasuries.

Attraction Of Europe Relative To The United States

European Financial Markets Have Been Much More Resiliant To Trump’s Tariffs, A Reversal From The Previous Few Years. According to Bloomberg, “Europe’s long-sluggish financial markets are being shocked into life as Donald Trump’s drive to reshape global trade and security undermines America’s decades-long dominance. Across assets of all stripes, the Old Continent is collectively trouncing America in a way that’s rarely been seen before. The euro is the strongest in three years. German bonds last week beat Treasuries by the most ever. And while European shares have been knocked by the trade war, they’re turning out to be far more resilient than American ones. The shift from just six months ago is remarkable. European markets in late 2024 seemed destined to be forever in the shadow of the US and its Trump-fueled exceptionalism. All anyone wanted to talk about was the US’s hot AI stocks, the ascendant dollar and an imminent wave of tax cuts and deregulation that would make America great again.” [Bloomberg, 2025-04-16]

- As Trump Has Diminished The Appeal Of The American Financial System, The Relative Appeal Of Europe Has Increased. According to Bloomberg, “It all suggests that time is up for the era when America, at the heart of global financial markets and trade, sucked in trillions of dollars from the rest of the world. Now investors are looking for alternative places to take their cash in a direct repudiation of Trump’s policies and unpredictable style of governing. Some of the biggest names in finance are positioning for more gains in Europe. Vanguard International favors short-dated bonds in the euro area with the central bank free to cut interest rates. Goldman Sachs Group Inc. sees the euro rising to $1.20 as the dollar’s appeal wanes. Citigroup Inc.’s Beata Manthey, who in October called the stock rally in Europe, this week downgraded US equities to neutral while maintaining her positive outlook on Europe.” [Bloomberg, 2025-04-16]

Housing Theory Of Everything

Sam D’Amico, Founder Of Impulse Labs: NIMBYism Makes It Hard To Change Course While Manufacturing, A Radically Important Part Of Building Successful Manufactured Goods. According to Bloomberg, “There are also some interesting political dynamics. People like to imagine that one impediment to domestic US manufacturing (in relation to China) is that labor costs are much higher here. But in Sam’s view, that doesn’t quite capture the tension. As he sees it, the bigger issue is that a modern advanced manufacturing company is likely to employ a lot of well-paid engineers. And then the issue is that in places where you”ll likely find well-paid engineers, the voters typically aren’t excited about living next to factories. And so you have this situation, in which the places that have talent density also have a NIMBY tendency, where it’s politically difficult to set up an actual plant. Something I hadn’t previously realized is that back in 2018, when Tesla famously started building cars in a gigantic tent in its parking lot, the issue was that it would”ve taken a long time to get all the permits to build a proper new facility. But it was able to get moving faster just by assembling cars underneath a temporary structure — basically it was about finding a legal loophole to avoid months and months of permitting hearings. But Sam’s main point is that when you”re doing modern, advanced manufacturing, the supply chain itself is literally the product. Or to put it another way, what you”re selling is literally your ability to stand up a supply chain. I don’t think this should be much of a surprise to listeners and readers of Odd Lots. Whether we”re talking about Boeing airplanes or ASML advanced lithography machines, what distinguishes these companies is their ability to coordinate (almost like an orchestra) various parts from hundreds of suppliers, some of whom might be making a component just for one customer. If a single piece doesn’t work on time, or comes in late, the whole thing doesn’t work. Sam likened it all to Lego assembly. You sell your ability to connect existing Legos in some distinct way.” [Bloomberg, 2025-04-14]

Outlook: Private Equity Wobble

After surging following election day, private equity stocks have not done well. All of the four largest companies are more than ten percent below their level at the beginning of November, after all four had advanced more than ten percent above that level. The reasons behind it are hardly surprising, but beyond the current economic uncertainty, there is reason to believe that Private Equity, as it has existed for the last few decades is in trouble, and it is worth understanding what sort of impact it could have on the real economy.

The fundamental business model of private equity is fairly simple. Financially speaking, a company is simply the future cash flows it will generate. Therefore, the owners of that company’s its equity holders’ main asset is those future cash flows.

If the company borrows to purchase a large portion of its equity, then the value of the remaining equity holders’ cash flows can increase, providing the increase in cash flow per share driven by the decrease in the number of shares is greater than the reduction in those cash flows due to higher interest payments (for more information about the basic calculus, see this 2023 paper).

Private equity firms take this trade and leverage their exposure to it through their funding structure. Typically, a firm will raise a fund from outside investors where they charge a management fee on top of all of the assets raised and a performance fee that is a percentage of the profits generated. These funds are typically expected to operate over a finite period of years.

The way this worked in the past, funds would buy companies on the open market, take them private, attempt to maximize their future cash flows per share, and sell them back onto the open market. That model has become less viable in recent years.

One reason for that is the trend of a general decline in interest rates has halted due to the response to the pandemic. Private equity took off in the 1980s, and for almost 40 years, interest rates were falling. As a result, a leveraged company, so long as it was not completely insolvent, would almost always be able to refinance its debt at a lower rate. This allowed private equity fund managers to increase their target leverage ratios, and when firms were sold back into the market, their buyers anticipated that with lower rates they could drive up leverage even more, further increasing cash flows.

In fact, the expectation of falling rates was so prevalent, many firms opted to have the firms they owned borrow at floating rates, with more than $3 trillion in obligations by 2023. Because the increase in leverage was maximized, there was almost no margin for error, and, to save money, few firms had opted to purchase insurance against rate increases.

On top of that, the success of private equity firms made it harder for them to execute their primary trade. Going back to the Ben-David and Chinco paper, levering up to increase cash flows per share only works if the ratio of the equity price to future cash flows is sufficiently low. The early success of private equity as a business model attracted trillions of dollars to the space, increasing competition for each company, raising share prices, and reducing the potential profits of the transaction.

Further complicating matters, the post-pandemic IPO market has been muted. This has made it difficult for private equity firms to sell their companies out of their funds. One method has been so called continuation funds, in which a new private equity fund is raised that uses its money to buy companies from private equity, rather than the open market.

More than 100 of these funds were raised in 2022 and 2023 alone, but with half the lifespan of typical funds, they are at or nearing maturity. With private equity funds on both sides of the transaction (often the same sponsor), incentives are not always good for the investors in each fund, which is why they are not popular. As a result, appetite among the large sophisticated investors who have been the main source of funding for private equity has declined. 2024 was the third consecutive year of declining fundraising, with the 2023-2024 decline alone being 24 percent.

It is no wonder, then, that the industry has been looking to other sources. The first Trump administration allowed target date funds, a typical 401(k) investment vehicle to put as much as ten percent of their assets into private markets, and the industry has been launching vehicles anticipating the second one would raise that threshold.

But the sophisticated fiancees at running these companies have not been standing pat. Of particular popularity have been what are called dividend recapitalizations, where a private equity owned company will borrow even more to pay a dividend to its equity owners, the private equity fund. It is not uncommon for these dividends to exceed the amount of money that the fund invested in the company, essentially guaranteeing an investment will be booked as profitable, even if the company goes under.

A different approach has been taken by some. KKR, the notorious private equity firm behind the RJR Nabisco deal immortalized in the book Barbarians at the Gate, has used some of its own money to directly buy companies to hold, rather than through funds.

The uncertainty caused by Trump’s tariffs has not helped. Dealmaking has ground to a halt.

The result is an environment where more than $8 trillion in assets are the subject of trillions more in debt, all of which is tied to companies that are marginally solvent by design. An exogenous shock, such as the imposition of the most sever tariffs in living memory, could be just the trigger to push them over the edge.

Technically insolvent companies will not go bankrupt as a rule, but if they do, the contagion effect would be something to behold.