April 17, 2025

Macrofinancial Outlook for the Day

Releases

Housing Starts/ Building Permits

March 2025: The Government’s 90 Percent Confidence Interval For The Annualized Monthly Rate Of Residential Construction Was Between -24.9 Percent And 2.1 Percent. According to Bloomberg, “For now, the slowing new-home industry is still seen adding to overall US economic growth in the first quarter, if only marginally so. The Federal Reserve Bank of Atlanta’s GDPNow forecast shows residential investment contributing a small 0.15 percentage points to first-quarter growth. The new residential construction data are volatile, and the government report showed 90% confidence that the monthly change ranged from a 24.9% decline to a 2.1% gain.” [Bloomberg, 2025-04-17]

March 2025: Housing Starts Fell By The Most In A Year, Decreasing At An Annualized Rate Of 11.4 Percent. According to Bloomberg, “Housing starts in the US fell in March by the most in a year, as weak demand from high prices and mortgage rates gives builders little confidence to break ground. New residential construction decreased 11.4% to an annualized rate of 1.32 million last month, restrained largely by single-family homes, according to government figures released Thursday. The figure was weaker than the 1.42 million median estimate in a Bloomberg survey of economists.” [Bloomberg, 2025-04-17]

Single Family Homes Construction Fell At A 14.2 Percent Annualized Rate. According to Bloomberg, “Construction of new single-family homes dropped 14.2% to an annualized 9.40 million rate, the steepest decline since the onset of the pandemic. Multifamily construction fell as well, but to a lesser extent.” [Bloomberg, 2025-04-17]

March 2025: The Number Of Single Family Homes Under Construction Fell To Its Lowest Level In Four Years, While The Rate Of Building Permits Being Issued Also Declined. According to Bloomberg, “Prices have come off their peak somewhat as builders deploy incentives to try to clear excess inventory, which still stands at the highest since 2007. That’s also prompting builders to slow down on projects, with the number of single-family homes under construction falling to the lowest level in four years, continuing a steady decline back to mid-2022. In a sign residential construction will remain constrained, building permits for single-family homes fell to the slowest pace in four months.” [Bloomberg, 2025-04-17]

Context: Housing Shortage

The shortage of Housing in desirable areas as a major cause of the discontent that helped elect Trump. Comparing a measure of inflation that does not include housing, the way Europeans do, shows a much different story than the one told by the CPI, yet the elevated CPI helped to explain the discontent voters felt.

Without housing, inflation was much closer to the Fed’s target in 2024 than the CPI would imply, which would have given the Fed the ability to cut interest rates starting in the middle of 2023.

And yet the Trump administration has pursued policies that have not made it easier to build housing. A decent portion of the construction labor force are exposed to his lawless immigration enforcement. A lot of wood comes from Canada, while a lot of the raw materials for drywall come from Mexico. DOGE has caused chaos at HUD and the FHA, not to mention the GSEs, while his trade war has caused mortgage rates to spike.

Philadelphia Manufacturing Survey

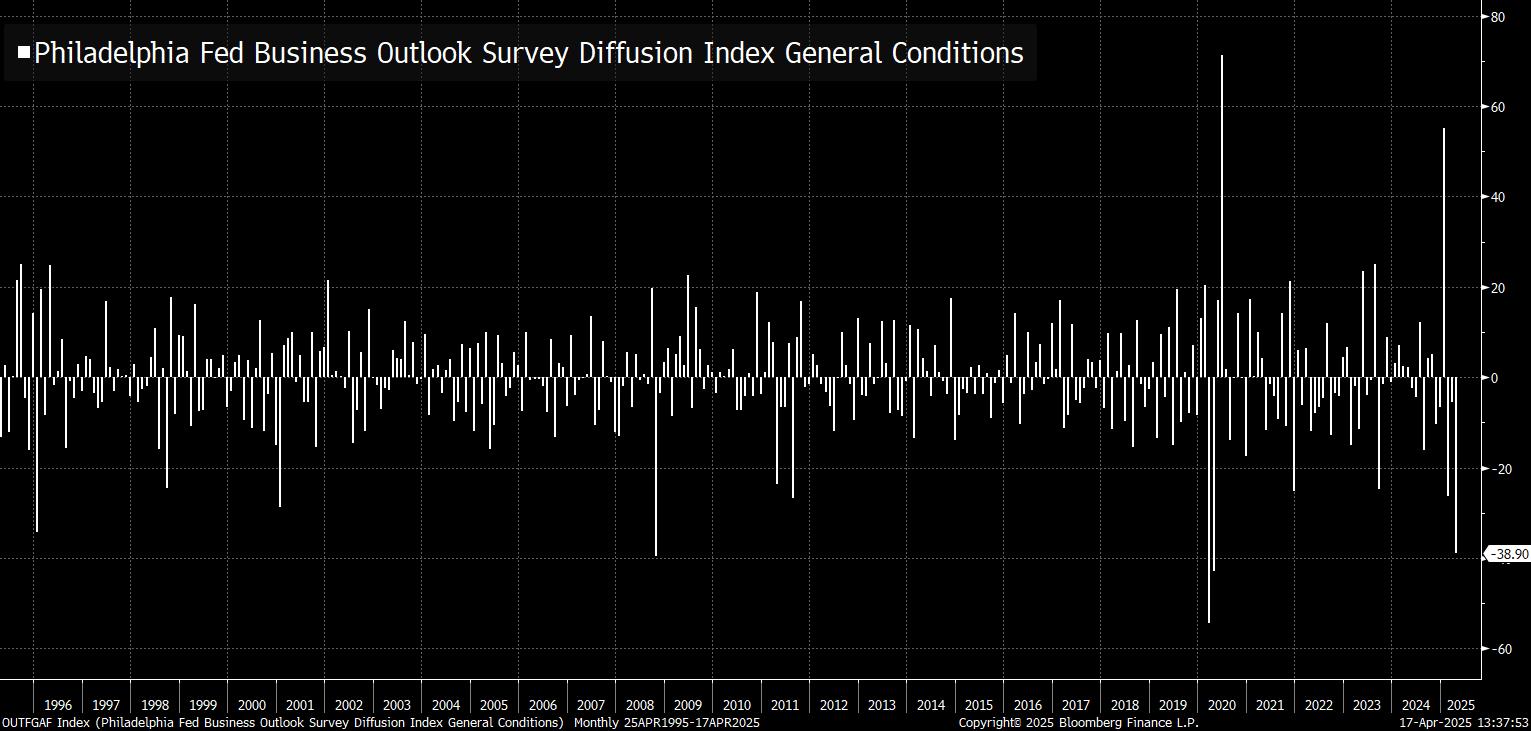

April 2025: Manufacturing Activity In The Region Supervised By The Philadelphia Federal Reserve Declined, With Indicators For General Activity, New Orders, And Shippments Turning Negative, Price Increases Forecast, And Subdued Growth Expectations. According to the Philadelphia Federal Reserve, “Manufacturing activity in the region declined this month, according to the firms responding to the April Manufacturing Business Outlook Survey. The survey’s indicators for general activity, new orders, and shipments all fell and turned negative. The employment index registered a near-zero reading, suggesting steady employment conditions. Both price indexes continue to suggest overall price increases. The future activity indicators continue to suggest subdued expectations for growth over the next six months.” [the Philadelphia Federal Reserve, 2025-04-17]

April 2025: The Philadelphia Manufacturing Survey Fell By The Third Most On Record, With The Only Larger Falls Coming In 2020 And 2008. According to twitter user @TheStalwart,  [twitter user @TheStalwart, 2025-04-17]

[twitter user @TheStalwart, 2025-04-17]

Flexport CEO Sounds The Alarm

8:57 AM: Two American Flexport Customers Sold Themselves To Their Chinese Factories. According to Ryan Petersen, “Two of our American customers devastated by the tariffs gave up and sold themselves to their Chinese factories in the last week.” [Ryan Petersen, 2025-04-17]

11:25 AM: Thousands Of American Small Business, Generating Trillions Of Dollars In Economic Activity Will Go Down If Tariffs Aren’t Changed. According to Ryan Petersen, “Thousands, and then millions, of American small businesses, including many iconic brands, will go bankrupt this year if the tariff policies on China don’t change. These small businesses are largely unable to move their manufacturing out of China. They are last in line when they try to go to a new country as those other countries can’t even keep up with the demand from mega corporations. The manufacturers in Vietnam and elsewhere can’t be bothered with small batch production jobs typical of a small business’s supply chain. When the brands fail, they will be purchased out of bankruptcy by their Chinese factories who thus far have built everything except a customer facing brand, which is where most of the value capture happens already.Consumer goods companies typically mark up the goods 3x or more to support their fixed costs (including millions of American employees). Now the factories will get to vertically integrate and capture the one part of the chain they haven’t yet dominated. American businesses import $600B worth of goods from China every year. Assuming typical retail markups we see in Flexport data, those goods create almost $2T worth of sales each year. In the week since the tariffs hit, ocean freight bookings from China are down 50% across the industry. Flexport bookings from China down more like 35%, but sources at carriers and forwarders indicate 50% is the industry wide stat. That’s around $1T of economic activity wiped out. And these companies tend to run very lean, financing inventory and reinvesting excess cash in more marketing and growth initiatives. If the goods stop, many will die. And when they die, it may actually be the final victory for the Chinese manufacturer as they scoop up brands that took decades to build through the blood, sweat and tears of some of the most creative and entrepreneurial people in the world. American brand builders are second to none worldwide. The fact is, America will have to back off these tariffs, it’s just a question of when. Even if it’s not this administration, a future one will realize they’ve got to get us out of the recession. and free trade is one of the most proven strategies to do it.” [Ryan Petersen, 2025-04-17]

Context: In Line with The Empire Manufacturing Survey, Manufacturers Are Not Looking Optimistic

While neither region is the top for manufacturing output, Pennsylvania and New York are both states in the top ten for manufacturing employment, and so the negative outlook of their employers is significant to the overall domestic manufacturing industry, an industry the Trump administration claims to be focused on.

The Fed

Economic Club of Chicago Speech: Powell Expected Inflation And Unemployment Diverging From The Fed’s Goals

April 2025: In A Speech To The Economic Club Of Chicago, Powell Forecast Rising Inflation And Unemployment, “Probably For The Balance Of This Year.” According to Bloomberg, “‘For the time being, we are well positioned to wait for greater clarity before considering any adjustments to our policy stance,’ Powell said. In a question-and-answer session that followed his speech, Powell said he expects unemployment and inflation will each be headed away from the Fed’s goals ‘probably for the balance of this year.’ The Fed chair acknowledged that a weakening economy and elevated inflation could eventually bring the central bank’s two goals into conflict. ‘We may find ourselves in the challenging scenario in which our dual-mandate goals are in tension,’ he said. ‘If that were to occur, we would consider how far the economy is from each goal, and the potentially different time horizons over which those respective gaps would be anticipated to close.’” [Bloomberg, 2025-04-16]

Powell Noted That Inflation From Trump’s Tariffs Could Be More Than A One-Time Impulse. According to Bloomberg, “Powell repeated Wednesday that the level of the tariff increases announced so far is significantly larger than anticipated. He added that the duties are highly likely to generate at least a temporary rise in inflation, but that the inflationary effects could also be more persistent. ‘Avoiding that outcome will depend on the size of the effects, on how long it takes for them to pass through fully to prices and, ultimately, on keeping longer-term inflation expectations well anchored,’ he said. Fed officials cut interest rates three consecutive times at the end of 2024, but started 2025 signaling they would take a more patient approach in the face of sticky inflation. Many officials have doubled down on that thinking, emphasizing the need to minimize the risk that tariffs lead to a persistent rise in inflation and Americans” long-term expectations for price growth.” [Bloomberg, 2025-04-16]

- Powell Said The Fed Was Conditionally Weighing The Stable Prices Part Of Its Mandate More Heavily In The Context Of Future Inflation, “Without Price Stability, We Cannot Achieve The Long Periods Of Strong Labor-Market Conditions That Benefit All Americans.” According to Bloomberg, “Federal Reserve Chair Jerome Powell again stressed the central bank must ensure tariffs don’t trigger a more persistent rise in inflation. ‘Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem,’ Powell said Wednesday at the Economic Club of Chicago. Powell said policymakers would balance their dual responsibilities of fostering maximum employment and stable prices, ‘keeping in mind that, without price stability, we cannot achieve the long periods of strong labor-market conditions that benefit all Americans.’ In a note to clients, JPMorgan Chase & Co. Chief US Economist Michael Feroli said the comment positioned price stability as a ‘prerequisite’ to sustainably achieving the Fed’s employment mandate.” [Bloomberg, 2025-04-16]

Commenting On The Market Turmoil That Followed Trump’s Tariffs, Powell Said, “Markets Are Doing What They’re Supposed To Do.” According to Bloomberg, “Powell also commented on recent financial market turmoil, stressing that markets were functioning ‘just about as you would expect them to function.’ ‘Markets are struggling with a lot of uncertainty, and that means volatility,’ Powell said, ‘but having said that, markets are functioning.’ He added, ‘markets are doing what they”re supposed to do. They”re orderly.’ Trump has continued to dramatically shift his plans for imposing new tariffs, leaving businesses, consumers and global financial markets on edge. He backtracked on so-called reciprocal tariffs announced on April 2, after the plans sent markets into turmoil. He pressed forward with a baseline 10% global tariff and duties in excess of 100% on China, then sent mixed signals on creating exemptions for smartphones and other technology products. He’s also imposed tariffs on auto, steel and aluminum imports, and signaled pharmaceuticals and semiconductors may be next.” [Bloomberg, 2025-04-16]

Trump Responded By Saying “Powell’s Termination Cannot Come Fast Enough!”

6:12 AM: Trump, In Response To Powell’s Speech Gave Him A Nickname “Too Late,” And, While Touting American Economic Strength Called For Rate Cuts. According to @realDonaldTrump on Truth Social, “The ECB is expected to cut interest rates for the 7th time, and yet, “Too Late” Jerome Powell of the Fed, who is always TOO LATE AND WRONG, yesterday issued a report which was another, and typical, complete “mess!” Oil prices are down, groceries (even eggs!) are down, and the USA is getting RICH ON TARIFFS. Too Late should have lowered Interest Rates, like the ECB, long ago, but he should certainly lower them now. Powell’s termination cannot come fast enough!” [@realDonaldTrump on Truth Social, 2025-04-17]

April 2025: The European Central Bank (ECB) Cut Interest Rates By 25 Basis Points. [Bloomberg, 2025-04-17]

Trump Claimed The Power To Fire Powell. According to Nick Timiraos, “Trump on Powell: ‘If I want him out he’ll be out of there, real fast, believe me.’ ‘He’ll leave if I ask him to. He’ll be out of there.’ ‘He’s too late. He’s always too late, too slow.’ ‘And I‘m not happy with him.’” [Nick Timiraos, 2025-04-17]

Context: What Happens to the Dollar

Yesterday, I noted that the Euro-Dollar exchange rate has surpassed a level it had not had since before Russia Invaded Ukraine. That figure is reproduced below.

The ECB Deposit facility rates are now 2.25 percent, while the Fed’s interest rate target is between 4.25 and 4.5 percent, effectively 4.33 percent. That opens up a carry trade, where an investor could short euros and buy dollars, exploiting the interest rate difference, while being at risk of a dollar decline. That risk could normally be hedged by currency swaps, but swap rates have spiked, thereby eliminating the opportunity.

Part of it is the general risks to the dollar that have been apparent in Trump’s second term. But the threat to Fed independence he has posed is, in my opinion, under priced. While Bessent called Fed independence a “jewel box that has got to be preserved,” Trump going against something an appointee of his had publicly said before would not be unprecedented.

Furthermore, the administration has already attacked its independences, claiming power over its regulatory functions, functions that give it information vital to making monetary policy decisions.

In other words, Trump represents a structural threat to the position of the dollar, which means that he cannot be arbitraged away.

Blackstone Dividend Cut

April 2025: Blackstone Declared A Dividend Of $0.93 Per Share. According to Blackstone, “Blackstone has declared a quarterly dividend of $0.93 per share to record holders of common stock at the close of business on April 28, 2025. This dividend will be paid on May 5, 2025.” [Blackstone, 2025-04-07]

January 2025: Blackstone Announced A Quarterly Dividend Of $1.44 Per Share. According to Blackstone, “Blackstone has declared a quarterly dividend of $1.44 per share to record holders of common stock at the close of business on February 10, 2025. This dividend will be paid on February 18, 2025.” [Blackstone, 2025-01-30]

Context: Public Companies Are Loathe To Cut Dividends

Public companies really do not like to cut their dividends. Survey after survey shows that financial financial executives view maintaining their dividends on par with maintaining earnings.

The rise of buybacks has made this easier, as they are seen as more flexible. So a cut in the dividend of the world’s largest alternative asset manager is something of note.

A Toothless Drug Price Executive Order

April 2025: Trump Signed An Executive Order With The Purpose Of Lowering Drug Prices. According to the Financial Times, “President Donald Trump has signed an executive order aimed at lowering drug prices for Americans in a move that would shake up the pharmaceutical industry in its biggest and most profitable market.” [the Financial Times, 2025-04-14]

The Order Would Not Require Drugmakers Offer Their Lowest Prices To American Buyers, Despite The Fact That Americans Paid On Average 3.2 Times More Than Citizens Of Other Developed Countries In 2022. According to the Financial Times, “The order stops short of implementing a “most favoured nation” status, which would force drugmakers to offer their lowest prices in the world to the US. Trump has previously railed against other countries for “freeloading” on US consumers, saying that American patients are subsidising medicines that are cheaper abroad. But a US official said on Tuesday that the government was “very focused on narrowing the delta between what the United States gets for prices versus what other developed nations do”. The US paid about 3.2 times more for branded drugs than other developed countries in 2022, according to research by RAND healthcare for the health and human services department — the most recent data available. The official said the executive action would “foster a more competitive prescription drug market”.” [the Financial Times, 2025-04-14]

**Financial Times: The Order Pushed For An End To The IRA Drug Price Negotiation Standards In “A Win For The Pharmaceutical Industry.** According to the Financial Times,”It also includes changes to the drug-pricing measures included in former president Joe Biden’s Inflation Reduction Act, which for the first time allowed Medicare, the public insurance programme for seniors, to negotiate the cost of drugs. Most notably, in a win for the pharmaceutical industry, the order pushes for an end to the different price negotiation regimes for pills and injectables. Under the IRA, Medicare could negotiate the price of popular pills after nine years, but would have to wait for 13 until it could negotiate the price of injectables, which was criticised by pharma companies.” [the Financial Times, 2025-04-14]

S&P 500 Death Cross

April 2025: Following Trump’s Tariff Announcements, The S&P 500 Matched A Pattern Traders Call A “Death Cross,” Where The 50 Day Moving Average Drops Below The 200 Day Moving Average. According to Bloomberg, “US stock prices have fallen sharply since President Trump launched sweeping tariffs on imports. Now, traders say, an unusual pattern in the stock market known as a “death cross” suggests further losses might be in store for the S&P 500 Index. Here’s what to know about the market phenomenon and what it means for stock prices. A death cross occurs when an index’s 50-day moving average crosses below its longer-term 200-day moving average, a reversal of the pattern that would be typical if the market were in an uptrend. Although the formation is unusual, it tends to emerge during volatile moments in the financial markets, especially as signs of economic distress appear. There was a death cross in November 1999 during the peak of the dot-com era, and again in October 2000 after the dot-com bubble burst, and in December 2007 ahead of the global financial crisis.” [Bloomberg, 2025-04-16]

- Despite The Name, Preformance Following The A “Death Cross” Has Not Been Abnormally Terrible. According to Bloomberg, “Since 1950, the S&P 500 has posted a median loss of 0.7% one month after a death cross was triggered, according to data compiled by LPL Financial. And three months later, the index was higher more often than not, with a median gain of roughly 2%. The index proceeded to rise 10% on average a year later, LPL Financial data show.” [Bloomberg, 2025-04-16]

Outlook: Denominator Effects And Financial Cascades

Institutional investors like rules. When you have herculean amounts of money at stake, it is more comforting to allocate it according to a set of rules than the whims of an investment committee. The committee is still there to make decisions, but allocation rules prevent any decision from being too bad.

There are different types of rules, but they generally follow the form of maximizing allowable exposure to any specific idea. A simplistic rule would be to mandate that a portfolio must be 60 percent stock and 40 percent bonds.

In normal circumstances, and assuming that the adherents to this rule do not impact the market with their trading, the response to a market decline of 10 percent in equities over five trading days would look as follows. To add color, let’s assume that bonds move in the opposite direction, but at one third the magnitude. That would mean, if stocks decline by one percent, bonds would increase by 0.33 percent.

The following table illustrates what would happen to the portfolio over five days assuming a reallocation after each day.

| Day | Stocks Change | Bonds Change | Stocks | Bonds | Total | Stocks % | Bonds % | Stock Trade | End Stocks | End Bonds |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | - 2 % | 0.66 % | 58.8 | 40.26 | 99.06 | 59.36 % | 40.64% | 0.64 | 59.44 | 39.62 |

| 2 | - 2 % | 0.66 % | 58.25 | 39.88 | 98.13 | 59.36 % | 40.64% | 0.63 | 58.88 | 39.25 |

| 3 | - 2 % | 0.66 % | 57.70 | 39.51 | 97.21 | 59.36 % | 40.64 % | 0.63 | 58.33 | 38.88 |

| 4 | - 2 % | 0.66 % | 57.16 | 39.14 | 96.30 | 59.36 % | 40.64 % | 0.62 | 57.78 | 38.52 |

| 5 | - 2 % | 0.66 % | 56.62 | 38.77 | 95.39 | 59.36 % | 40.64 % | 0.61 | 57.23 | 38.16 |

The overall portfolio declines by 4.6 percent, but if the investor had not reallocated, the portfolio would have declined by 4.3 percent. What that illustrates is how, in period where a consistent trend exists, the ratio rule exacerbates the portfolio’s decline relative to what doing nothing would do.

Of course, the real world is not that simple. During normal market fluctuations, rules like this have the effect of stabilizing markets. Because these portfolios are not price takers, their trading decisions actually move the market, and by enforcing the selling of winners and buying of losers, fluctuations are smoothed over.

Unfortunately, when the market is moving due to something more than normal fluctuations, something worse happens. For the portfolios, the same loss exacerbation as illustrated above occurs, but the selling of what areas had strengthened leads to downward pressure on those areas. What is doing well incurs the pressure of what isn’t.

That is the point of a recent article in the Journal of Applied Economics by Hasse, Lecourt, and Siagh. They show something similar in sovereign wealth funds, finding that in normal market conditions, periodic rebalancing is ideal, but during recessions, and crises, “the buy-and-hold approach is best.”

That is not currently the case for many institutional investors, and that could combine with another problem in modern markets: opaque private investments. Generally, private investments do not trade as frequently as their public counterparts, and there is less pricing information. While any deal provides pricing information, those certainly do not occur on the order of the fractions of a second between stock price changes.

This is in part a service. Private companies can hide the volatility of their values behind infrequently quoted prices, giving their investors a sense of stability. Unfortunately, just because a price is not quoted, does not mean it is not changing.

An unchanging price in a falling market is, however, a problem for these rule-bound investors. By definition, they become overweight private investments, and unlike public securities, trading them is tricky.

Since the tariff-driven market chaos started, big institutional investors have been looking to offload private investments. That is mostly because these investments have not been marked down.

Unfortunately, the relatively thin markets for these private investments means that attempts to sell them quickly could quickly tank their prices, and those prices, once marked, need to be accounted by others. While this could limit the denominator-driven, it imposes another mark-to-market loss on those investors.

That limits their ability to borrow, and begins to tie things up. Mark-to-market gains are a common form of collateral, and if that collateral falls, leveraged investors could face magin calls. In these, investors must either post more collateral, or sell the underlying assets. That can spread into what is called contagion, where weakness in one overleveraged portfolio has second order consequences that can blow things up.

And that can lead to what Nathan Tankus of Notes on the Crisis said could be the worst day of the Trump administration, the one where “someone tells [him] what central Bank Liquidity Swaps are.”