Fannie And Freddie

May 2025: Trump Said “The Time Would Seem Right” To Re-Privatize Fannie Mae And Freddie Mac. According to Bloomberg, “President Donald Trump said that he’s giving ‘very serious consideration to bringing Fannie Mae and Freddie Mac public’ after more than a decade of government control. ‘Fannie Mae and Freddie Mac are doing very well, throwing off a lot of CASH, and the time would seem to be right,’ Trump wrote late Wednesday on his Truth Social platform. ‘Stay tuned!’” [Bloomberg, 2025-05-21]

Matt Levine: Before The GFC, The Value Of Fannie Mae And Freddie Mac (As Enterprises) Was Their Implicit Government Guarantee. According to Matt Levine in Bloomberg, “Fannie and Freddie are giant companies with lots of money (Fannie Mae is the largest company in the US by assets), they are regulated by a dedicated US government agency (currently the Federal Housing Finance Agency), and they were chartered by Congress to achieve a regulatory purpose. Their guarantees were, for a long time, considered almost as good as a US government guarantee. This was in part because they were regulated and well-capitalized, and because Fannie and Freddie were after all in a pretty good business: They had reasonably high standards for loans, they charged billions of dollars of guarantee fees to banks, and they seemed to have plenty of money put aside to pay out those guarantees even if there was a big wave of mortgage defaults. But people also thought that the guarantee was good because they assumed that, if anything did go wrong at Fannie or Freddie, the government would step in to bail them out. They were created by the government, they were a policy tool of the government, they are normally referred to as ‘the GSEs’ (government-sponsored enterprises), they were far too big to fail, and it just seemed obvious that the government wouldn’t let them fail. This was so obvious to everyone that, on the cover of the prospectus for every Fannie and Freddie mortgage-backed security, there would be a warning like ‘The certificates, together with interest thereon, are not guaranteed by the United States and do not constitute a debt or obligation of the United States or any agency or instrumentality thereof other than Fannie Mae.’ Everyone assumed that Fannie and Freddie bonds were backed by the government, so Fannie and Freddie constantly went around saying that they weren”t. But no one believed them. And then in 2008 Fannie and Freddie went bust. Part of the problem was that there was a historic housing downturn, a lot of people defaulted on their (conforming) mortgages, and Fannie and Freddie had big losses on their guarantees. Another part of the problem is that, over the years leading up to 2008, Fannie and Freddie built up sort of an investment portfolio that was horrific in very 2008 ways. Fannie and Freddie bought only high-quality conforming mortgages in their basic business of guaranteeing mortgages, but they invested their money — the insurance reserve they”d need to pay out those guarantees — in a surprisingly large amount of subprime mortgages.6 And it turns out that everyone was right: The government did not let Fannie and Freddie fail. Instead, the government took them over: The FHFA, Fannie and Freddie’s regulator, was appointed ‘conservator’ of the enterprises, basically kicking out their public-company directors and taking over their management. And the US Treasury gave them a huge line of credit to make sure that they could pay back all of their guarantees.” [Matt Levine in Bloomberg, 2025-01-08]

After Fannie And Freddie Could Not Meet Their Obligations Under The Bailout They Received From The American People, It Was Amended To Require 100 Percent Of Their Income Would Go To The American People Forever. According to Matt Levine in Bloomberg, “That is almost what the government did in the Fannie and Freddie bailouts? I think? It is debatable. The actual terms of the bailout were: Treasury committed to financing facilities in which it loaned Fannie and Freddie tens of billions of dollars, and Fannie and Freddie promised to pay 10% interest on those loans. Technically these loans were preferred equity, not loans, and the interest is technically a preferred dividend,7 but for simplicity I am going to say ‘loans’ and ‘interest.’ As an additional sweetener, Treasury got warrants to purchase 79.9% of Fannie’s and Freddie’s common stock for free. The result, in 2008, was that considerably more than 100% of Fannie and Freddie’s income, for the foreseeable future, would go to Treasury in the form of 10% interest on its giant bailouts, and if for some reason any money was left over for shareholders, Treasury would get 79.9% of it. This looked, in 2008, quite close to ‘we will give you a Snickers bar.’ Fannie and Freddie’s common stocks were delisted from the New York Stock Exchange, because their prices fell below $1 per share, and who would buy them? They continued to trade over the counter, as a weird curiosity for optimists who thought that one day there would be money in them for shareholders. In fact, for several years, Fannie and Freddie did not earn nearly enough money to pay Treasury its 10% coupon, which meant that each year they became less solvent, and had to borrow more money from Treasury just to pay Treasury the interest on the money they had previously borrowed. This became quite embarrassing. So in 2012, Treasury and Fannie and Freddie (now controlled by FHFA, their conservator) amended the deal. ‘Instead of paying you 10% on the money we have drawn, which is more than we can afford,’ they said, ‘we will just pay you whatever we can afford. Whatever our net income is, we”ll give you 100% of it, even if that is less than 10% of the money we have already borrowed. Or if it’s more. Forever.’ This is called the ‘third amendment,’ and it is the central point of the story. Because right around then — a little before or a little after the third amendment, depending on which side you”re on — Fannie and Freddie’s circumstances changed. The housing market had recovered, they were charging economically appropriate guarantee fees, and they basically had a good business. They started making more than enough money to pay Treasury the 10% interest on its loans, and in fact to start paying down the principal of those loans. There was light at the end of the tunnel: Eventually Fannie and Freddie would be able to pay back Treasury and get back on their feet; Treasury would get 10% interest on its money plus 79.9% of the stock of the companies as payment for its help, but Fannie and Freddie would go back to their old lives and the public shareholders, who owned the other 20.1% of the stock, would be real shareholders again. Except the deal had changed and now there was no way for Fannie and Freddie to pay back the loans: Instead of ‘we will pay you 10% annual interest on the money you loaned us,’ the deal after the third amendment was ‘we will pay you 100% of our income forever.’ When their income was considerably less than the 10% interest, I suppose that looked generous. When it was considerably more than the 10% interest, it looked harsh. The loans could never be paid back, because every penny that came in to Fannie and Freddie had to go to Treasury, without ever reducing the amount they owed.” [Matt Levine in Bloomberg, 2025-01-08]

- 2021: This Arrangement Was Changed Such That While They Did Not Have To Pay That Money To The Treasury, They Still Owed It To The American People. According to Matt Levine in Bloomberg, “But there has been, for many years, talk about returning Fannie and Freddie to private hands, and thinking about how one would do it. As part of that thinking, in 2021, the terms of the bailout deal were changed again: Fannie and Freddie are now allowed to keep all of their income to build up capital, rather than paying it to the government. But only sort of: They don’t have to pay their income in cash to the government, but each increase in net worth adds to the amount that they owe the government, so they still can’t pay off the debt. But building up capital is the sort of thing that you”d want them to do if you wanted to eventually launch them on their own again as private companies.” [Matt Levine in Bloomberg, 2025-01-08]

Matt Levine: Bill Ackman’s Privatization Proposal Would Amount To A More Than $300 Billion Transfer From The Treasury To Fannie And Freddie’s Shareholders. According to Matt Levine in Bloomberg, “Right now, if you look at Fannie Mae’s balance sheet, you will see $4.3 trillion of assets (mostly mortgages), $4.2 trillion of liabilities (mostly mortgage-backed securities), and total shareholders” equity of $90.5 billion. (Freddie: $3.34 trillion, $3.29 trillion, $56 billion.) But the amounts that Fannie and Freddie owe the government — which are counted as part of shareholders” equity, not liabilities, because they are technically preferred stock — are $212 billion and $129 billion, respectively, or more than double their shareholders” equity.9 The actual book equity available to common shareholders is negative many tens of billions of dollars. Fannie and Freddie have nowhere close to enough money to pay back Treasury. But you could do different accounting. Fannie Mae borrowed $119.8 billion from Treasury, and has since paid back a total of $181.4 billion. Freddie Mac borrowed $71.6 billion and has paid back $119.7 billion.10 Big chunks of those repayments came in 2013, when Fannie and Freddie started paying all of their net income to the government. If you treated those repayments as paying down their borrowing — which, again, is not how they are treated under the amended terms of the bailout — then they have arguably paid back everything by now, with interest. Ackman wrote on X last week: ‘The scenario we envision is that … the GSEs are credited with the dividends and other distributions paid on the government senior preferred, which would have the effect of fully retiring the senior preferreds at their stated 10% coupon rate with an extra $25 billion profit (in excess of the preferreds” stated yield) to the government. This extra profit could be justified as payment to the government for its standby commitment to the GSEs during conservatorship.’ Ackman’s argument is that, if you went back to the original deal, Fannie and Freddie have already paid back the government, so they don’t have to pay any more. So their $146 billion of combined shareholders” equity actually belongs to the shareholders, that is, 79.9% to the government and 20.1% to the public shareholders, who Ackman says are ‘millions of small investors who owned the stock [before 2008] as it was perceived to be safe dividend payer,’ plus him.11 And so privatization is mostly a simple matter of declaring that actually Treasury has already been paid back and the $341 billion that Fannie and Freddie in aggregate owe the government is just (as Felix Salmon puts it) ‘a function of bad accounting.’ You wipe that debt from their (and Treasury”s) balance sheets and you get more or less viable-looking companies. Maybe not quite viable yet, but they have a few more years to accumulate capital from their profitable businesses before they are actually released, and when they are, you do an initial public offering to raise the rest. Ackman: ‘Assuming a Q4 2026 IPO, the two companies collectively would need only raise about $30 billion to meet the 2.5% capital standard, a highly achievable outcome.’ And then the stock is worth tens of billions of dollars; Ackman puts it at $34 per share by 2026. (They’re both a bit below $5 today.) Anyway that’s roughly the state of play. We’ll see what happens. Here are three things that I am thinking about. One: Why would the government agree to (1) write off $341 billion that technically, legally, Fannie and Freddie still owe to Treasury and (2) essentially transfer that value from taxpayers to Fannie and Freddie’s existing common shareholders?” [Matt Levine in Bloomberg, 2025-01-08]

Matt Levine: “Do Fannie And Freddie Need To Be Re-Privatized?” Mortgages Work Today, And Given The Difficulty Of Imagining Them Operating Without A Government Guarantee, Should Private Shareholders Be Entitled To Their Profits In Good Times? According to Matt Levine in Bloomberg, “Do Fannie and Freddie need to be re-privatized? It does not seem to be especially impossible to get a mortgage today, and Fannie and Freddie are profitable for the government. What problem would it solve to re-privatize them? “A successful emergence of Fannie and Freddie from conservatorship should generate more than $300 billion of additional profits to the Federal government,” argues Ackman, “while removing ~$8 trillion of liabilities from our government’s balance sheet,” but presumably he thinks the enterprises are a good investment for him. Why are they a bad investment for the government? Three: What does it mean to re-privatize them? I started this column by talking about the various ways you could imagine the government encouraging home ownership. One of those ways is a well-capitalized, fortress-balance-sheet, privately owned mortgage guarantee company that operates with the … blessing and regulation, let’s say, but not the financial backing of the government. Another way is a government guarantee. For historical reasons, but also for too-big-to-fail reasons, pre-2008 Fannie and Freddie were technically the former but actually the latter. Perhaps post-2026 Fannie and Freddie will be different. We have learned some lessons from 2008. They will be better capitalized, better regulated, less likely to run into trouble, and everyone will understand that, if somehow they do run into trouble, the government won’t bail them out again. But … why? Is the Trump administration regulator who releases them from conservatorship also going to be particularly strict about their capital requirements and prudential regulation? Under new private ownership, will they not be tempted to invest in risky trades again? If they continue to guarantee a huge chunk of US mortgages, will they no longer be too big to fail?” [Matt Levine in Bloomberg, 2025-01-08]

Florida

In December 2023, Sastry, Sen, and Tenekedjieva documented how Florida’s housing market had, even more than the national housing market, been subsidized by Fannie and Freddie. One of the requirements Fannie and Freddie put on Mortgage lenders is a requirement for Home Insurance, provided by a well rated insurer.

Florida’s exposure to extreme weather events led many insurers to exit the market, as they found they could not profitably price risk. That posed a problem, however, the state government, wary of this problem, encouraged loser state insurance regulations allowing for many companies to enter the market. While major ratings agencies would not have rated these insurance companies well as, “they service the riskiest areas, are less diversified, hold less capital,” and become insolvent at a faster rate, smaller ratings agencies gave them good ratings. This was sufficient for Fannie and Freddie, which is Florida mortgages are sold to Fannie and Freddie at a higher rate than for the rest of the country.

If, however, Fannie and Freddie are re-privatized, it is hard to imagine shareholders would be comfortable with that increased risk. Therefore, they would likely raise the ratings standards for insurance companies on Mortgages they purchase. While precise consequences are hard to predict, looking at the difference between conforming and jumbo mortgages, it seems reasonable to expect that this would either lead to an increase of mortgage rates in Florida of around 11 basis points, or much higher insurance costs for Florida homeowners.

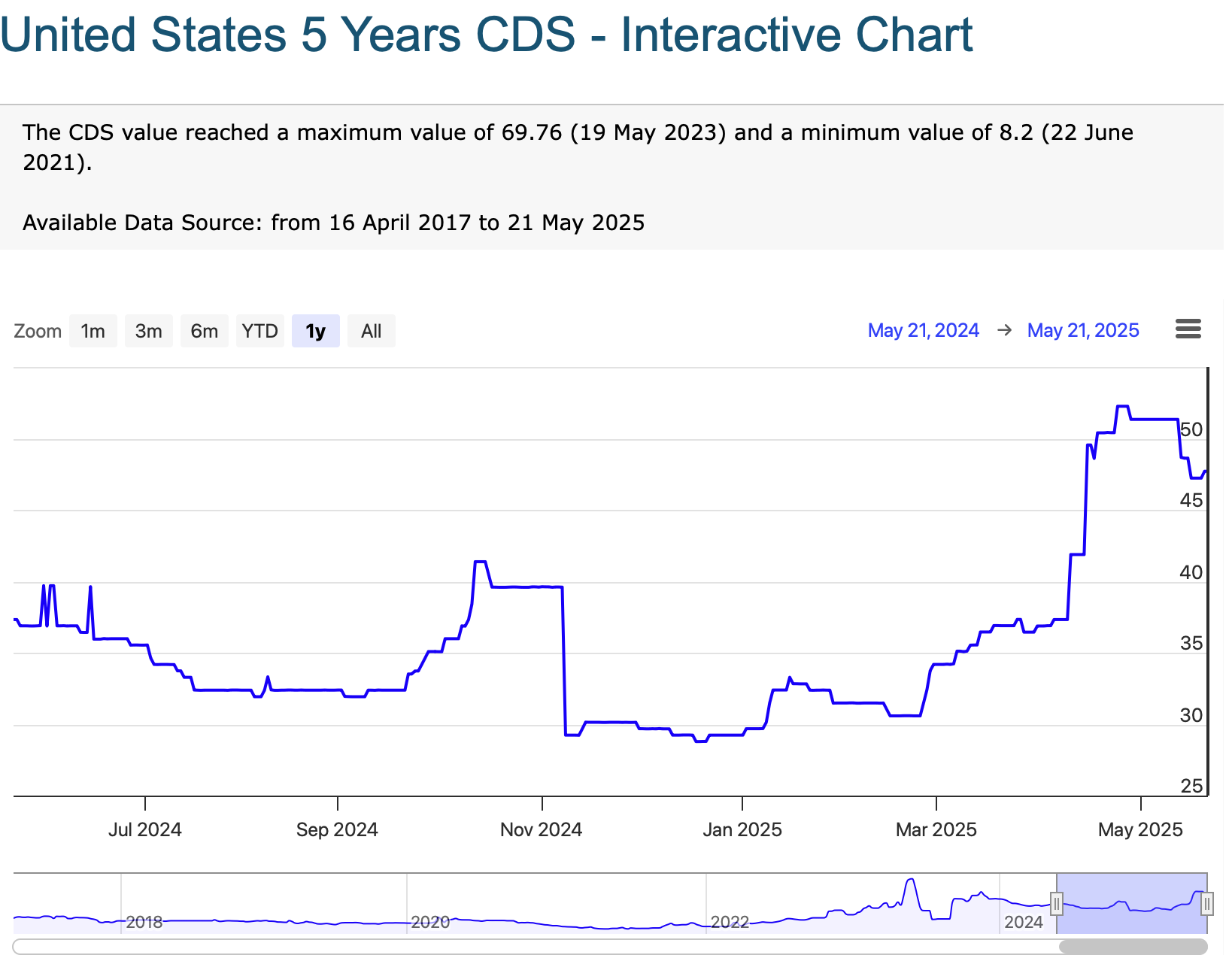

[World Government Bonds,

[World Government Bonds,  [Financial Times,

[Financial Times,  [Bloomberg,

[Bloomberg,  [Bloomberg,

[Bloomberg,