Stress in the macroeconomy has continued to build. The housing market shows notable weakness with slower homebuilding activity and declining home value growth, while manufacturing output in key states like Texas has retreated to near-zero growth despite “higher-than-usual price pressures.” Damage from Trump’s trade war, even with the recent “truce” seems to have been done, with shipping from China to the United States continuing to decline. At the same time, estimates of the impact of his proposed 50 percent tariffs on the EU show lower income and higher prices. Meanwhile, Fed Officials have cited uncertainty as a reason to delay interest rate cuts, while elevated debt spreads show that marginal businesses face increased financial stress since Trump took office, contradicting promises of business-friendly policies.

And, as is standard, one of Trump’s companies (TMTG) has offered $1 billion in convertible bonds that it promises to use to buy cryptocurrencies. For the buyers of those bonds, their profitability will directly depend on continued volatility in markets, volatility Trump seems to have some power over.

Macroeconomic Weakness

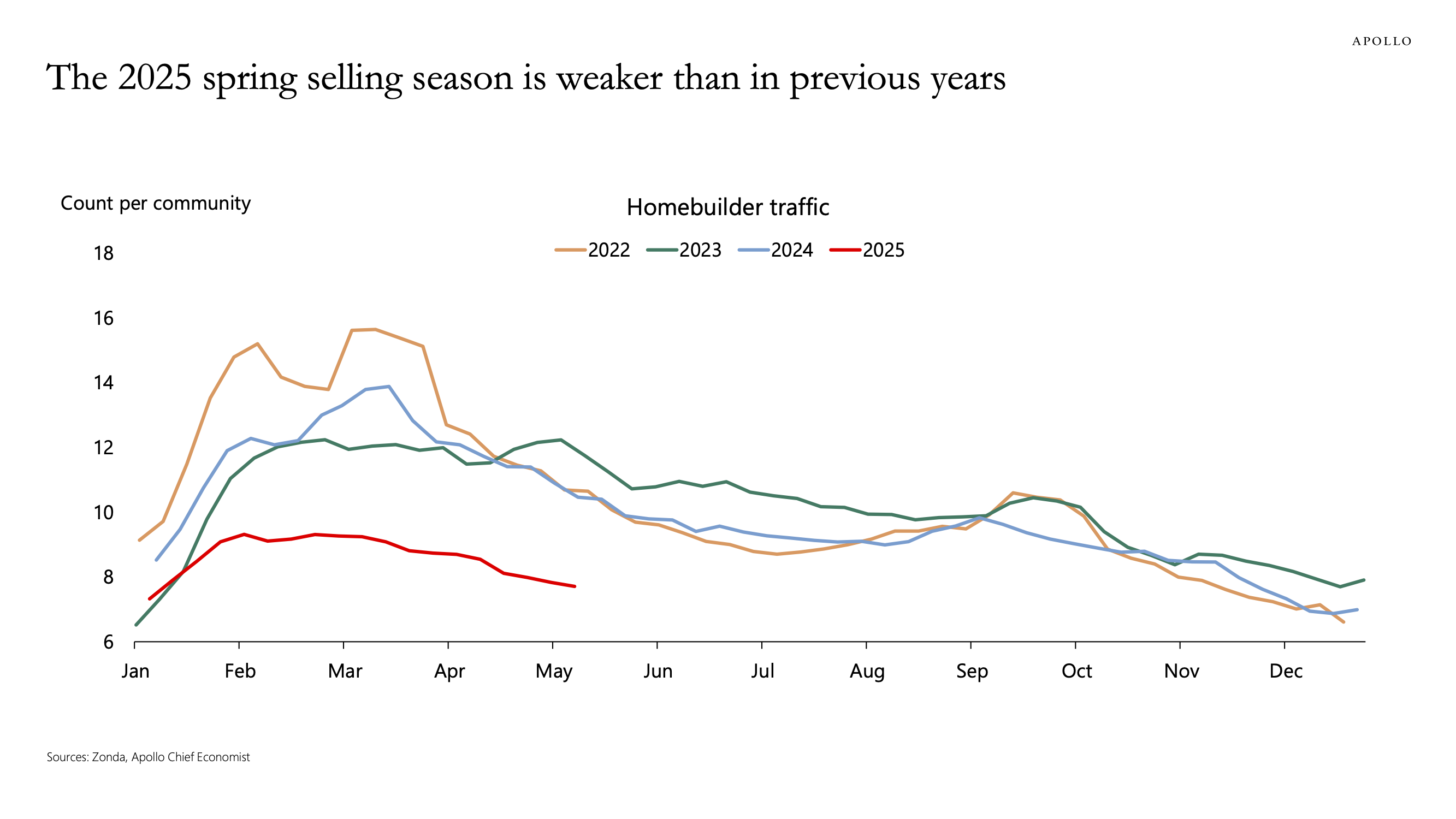

Housing

2025: Homebuilding Has Been Notably Slower Than In Previous Years. [Apollo, 2025-05-25]

Code

# Include custom plot themeinclude("../scripts/oxocarbon-plot.jl")theme(:oxocarbon)# Set up The Necessary PackagesusingFredData, DataFrames, Dates# Set up the Fred API key =ENV["FRED_API_KEY"]f=Fred(key)# Gather the necessary datanational_prices=get_data(f, "CSUSHPISA"; observation_start="2024-03-01", observation_end="2025-03-02", units="pc1").datalargest_cities=get_data(f, "SPCS20RSA"; observation_start="2024-03-01", observation_end="2025-03-02", units="pc1").data# Make the Plotplot(national_prices.date, national_prices.value; xlabel="Month", ylabel="Percent Change, YoY", label="National", linewidth=2, title="March 2025: Slowing Home Value Growth")plot!(largest_cities.date, largest_cities.value; label="20 Largest Cities", linewidth=2,)

Texas Manufacturing Sector

May 2025: After Modest Growth In Output In March And April, Manufacturing Production Growth In Texas Retreated To Near-Zero. According to the Dallas Federal Reserve, “Texas factory activity held steady in May, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, retreated four points to a near-zero reading, indicating flat output this month after modest growth in March and April.” [Dallas Federal Reserve, 2025-05-27]

May 2025: “Higher-Than-Usual Price Pressures Continued” For Texas Manufacturers. According to the Dallas Federal Reserve, “Higher-than-usual price pressures continued in May, while wage growth remained slightly subdued. The raw materials prices index fell 8 points to 40.7, and the finished goods prices index held steady at 15.1—both readings are well above average. Meanwhile, the wages and benefits index remained below average, largely unchanged at a reading of 15.0.” [Dallas Federal Reserve, 2025-05-27]

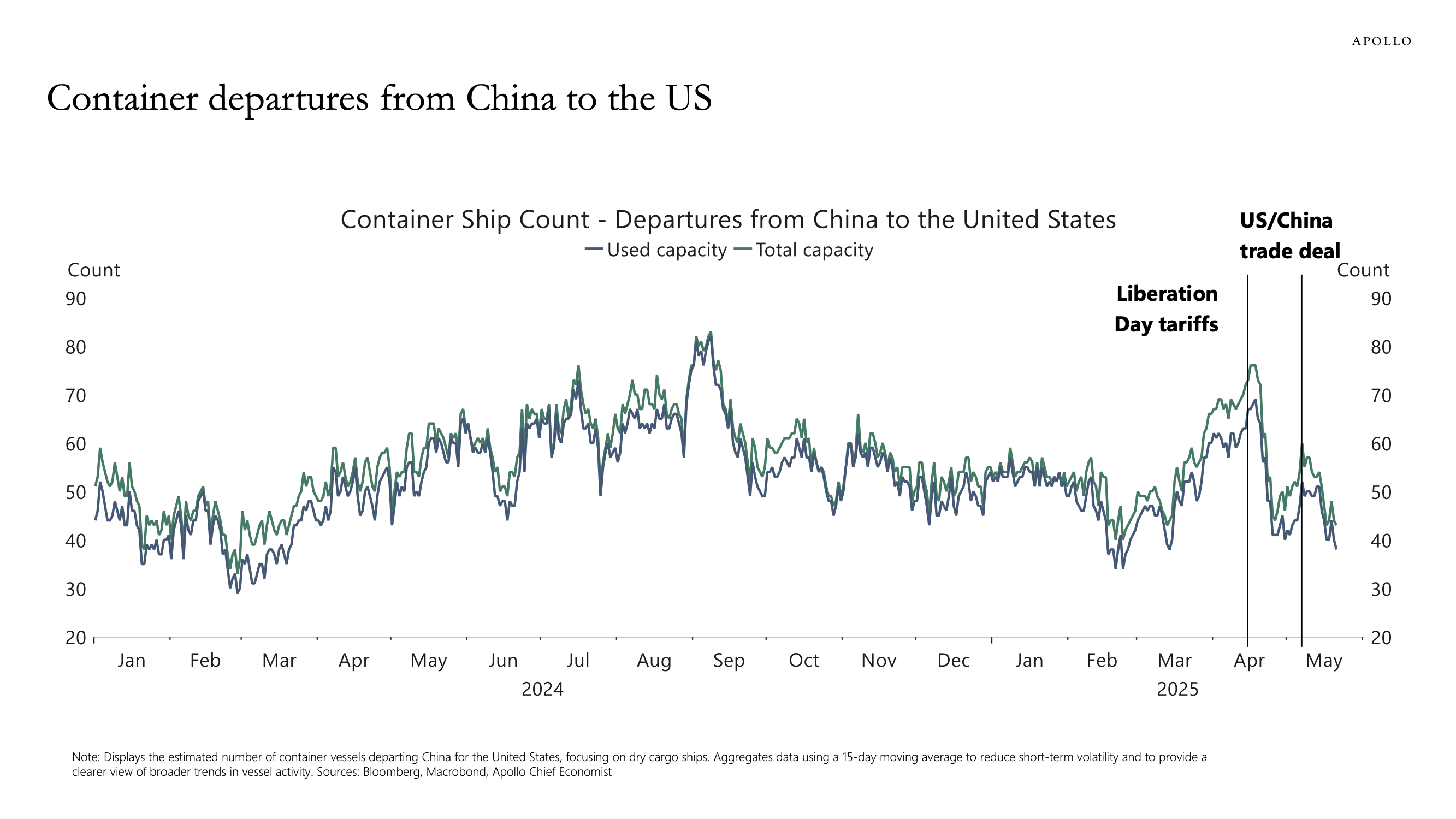

Trade War

Since Trump’s Trade Truce With China, Container Shipping From China To The United States Has Continued To Decline. [Apollo, 2025-05-25]

Bloomberg: If Trump’s Threat Of A 40 Percent Tariff On The European Union Was Enacted, income Would Fall By Roughly 60 Basis Points, While Prices Would Increase By 30 Basis Points. According to Bloomberg, “Trump’s 50% tariff threat would hit $321 billion worth of trade in goods, lowering US gross domestic product by close to 0.6% and boosting prices by more than 0.3%, according to Bloomberg Economics calculations.” [Bloomberg, 2025-05-26]

Threats To American Companies

May 2025: German Chancellor Mertz Threatened American Tech Companies As Targets For Possible Retailiation If Trump Continued To Escalate His Trade War. According to Bloomberg, “The European Union could retaliate against US technology companies if the trade conflict with Donald Trump’s administration escalates, German Chancellor Friedrich Merz said. While the leader of Europe’s largest economy aims to reduce tariffs and defuse tensions with the White House, he said that the bloc would need to protect its interests and pointed to the US surplus in services trade with the EU. ‘At the moment, we strongly protect US tech companies — also on taxes,’ Merz said Monday in Berlin at the WDR Europaforum conference. ‘That can be changed, but I don’t want to escalate this conflict. I want to solve it together.’” [Bloomberg, 2025-05-26]

Investment Held Back

GAO: The Trump Administration Illegally Impounded $5 Billion In Investments Targeted At Building Out An Electric Charger Network. According to the New York Times, “The Trump administration violated the law when it halted funding under a $5 billion federal infrastructure program, according to a nonpartisan government watchdog, which concluded on Thursday that officials should restore the aid for electric vehicle charging stations as authorized by Congress. The findings appeared to inch the government closer to a high-stakes constitutional showdown, as President Trump increasingly claims expansive powers to defy lawmakers and control the nation’s purse strings as part of his broad reorganization of American government. The allegations arise from Mr. Trump’s first days in office, when he and his administration raced to block vast swaths of the federal budget seen as incompatible with his political beliefs. One of the president’s targets was the National Electric Vehicle Infrastructure program, a roughly $5 billion tranche of money enacted as part of the bipartisan infrastructure law in 2021 to create a national network of charging stations. Mr. Trump and his allies had long denounced that money as wasteful, and the Transportation Department froze the program’s continued funding in February. Reviewing that action, the Government Accountability Office determined on Thursday that the funding halt had amounted to an improper impoundment, since the administration had denied money to states that lawmakers had previously approved. The government “must continue to carry out the statutory requirements of the program,” the watchdog said.” [New York Times, 2025-05-22]

Capital Flight

Higher Rates Around The World Could Diminish The Appeal Of American Bonds Relative To Japanese Ones For Japanese Investors. According to Bloomberg, “Fast forward to this week, and longer-term government bond yields in the world’s No. 1 and No. 4 economies are at levels that would have appeared normal before 2008, with 10-year US Treasury rates around 4.5% and Japan’s numbers around 1.5%. And there’s little reason for those rates to head back down in coming years. Both the US and Japan have heavy debt burdens and governments doing next to nothing to tackle them. Plus, the new reality for world trade means deflation fears are done. The consequences of higher-forever long term borrowing costs are tough to map out, just as the ultra-low rate era was full of surprises. One major consequence is likely to be a refocusing of Asian savings on opportunities within the region, rather than plowing quite so much into American markets. Another could be a forced refocus in Washington on the fiscal profile — House passage of a Republican tax bill (by exactly one vote) that may push national debt beyond $40 trillion notwithstanding.” [Bloomberg, 2025-05-24]

Since The 1990s Asian Financial Crisis, Asian Investors Have Parked Large Amounts Of Money In American Assets. With Domestic Rates Rising (And The Dollar Weakening), That May Not Continue. According to Bloomberg, “Asian investors in particular had a lot of excess money to put to work, in part a result of moves to accumulate reserves in the wake of 1990s crises — a phenomenon dubbed by former Fed chair Ben Bernanke as a savings glut. Eventually the pattern featured anomalies like Japan’s Norinchukin, a cooperative bank that invests the deposits of millions of Japanese farmers and fishermen, plowing tens of billions of dollars into things that went well beyond plain-vanilla investments. There were plenty of plain-vanilla investments, too. All in all, the 11 major Asian economies doubled their holdings of overseas assets to $40 trillion over the past decade, according to analysis by Gavekal Research. ‘The data is sketchy, but most of the accumulation of foreign assets has been in US dollars,’ Gavekal’s Udith Sikand wrote in a note earlier this month. With yields on the rise around the world, investors don’t need to rely on the US as much. Take Japan Post, which has one of the biggest Japanese bank-deposit pools. During the 2010s it effectively swapped domestic bonds for higher-yielding foreign ones. That was back when Japanese 10-year yields averaged less than 0.5%. Now that they”re a percentage point higher, and without the foreign-exchange risk, the appeal of staying at home is much greater. For many Asian investors, “the natural destination for capital will be their home markets as domestic yields normalize, as they are in Japan,” Sikand wrote. “The size of the potential flows is enormous,” he said. “South Korea, Japan, Singapore, Taiwan and Hong Kong between them have net international positions excluding official reserves of more than $5 trillion.” Rising worries about US investments are also creating a push-pull effect. Last week’s downgrade of the US sovereign rating by Moody’s Investors Service, along with increasing concerns about the fiscal effects of the Republican tax bill now headed to the Senate, may spur some investors to rethink how much they deploy in the US. Hong Kong pension fund managers were among those this week discussing the implications, as was the Philippine central bank.” [Bloomberg, 2025-05-24]

Tighter Business Conditions

Neel Kashkari: The Trump Administration’s Trade And Immigration Policies Have Created Uncertainty That Could Delay The Fed From Cutting Rates. According to Bloomberg, “Federal Reserve Bank of Minneapolis President Neel Kashkari said major shifts in US trade and immigration policy are creating uncertainty for Fed officials to move on interest rates before September, as the Trump administration continues tariff talks with numerous governments. ‘Anything is possible,’ Kashkari said Monday in an interview on Bloomberg Television in Tokyo. But will the picture ‘be clear enough by September? I am not sure right now. We will have to see what the data says, but also how the negotiations are going,’ he said. If trade deals are struck between the US and other nations over the next few months, ‘that should provide a lot of the clarity we are looking for,’ he added.” [Bloomberg, 2025-05-26]

Chicago Fed Chief Austan Goolsbee: Stagflationary Pressure From Trump’s Tariffs Could Delay Interest Rate Cuts. According to Bloomberg, “Widespread levies are seen pushing up US inflation while denting growth as firms pull back investment and households rein in spending. Kashkari and other central bank officials, including Chicago Fed chief Austan Goolsbee, have said the bar remains high for cutting interest rates in the near term. ‘This uncertainty is potentially weighing on economic activity and creating challenges for us because we are not sure where things are going to settle and, therefore, where we should go with monetary policy,’ Kashkari said.” [Bloomberg, 2025-05-26]

The Weakest Businesses Have Been Having Even More Trouble

Code

# Gather the necessary dataccc=get_data(f, "BAMLH0A3HYCEY"; observation_start="2024-05-23", observation_end="2025-05-24").datab=get_data(f, "BAMLH0A2HYBEY"; observation_start="2024-05-23", observation_end="2025-05-24").dataeffr=get_data(f, "EFFR"; observation_start="2024-05-23", observation_end="2025-05-24").data# Make the plotplot(ccc.date, ccc.value .- b.value; xlabel="Date", ylabel="Spread: CCC Rate - B Rate", label="Spread", title="Elevated Debt Spreads")vline!([Date(2025,1,20)], label="Inaguration", linestyle=:dash)vline!([Date(2025,4,2)], label="Tariff Announcement", linestyle=:dash)rhs=twinx()plot!(rhs,effr.date, effr.value; label="Risk-Free", color=colorant"#525252", ylabel="Effective Federal Funds Rate")

This figure takes a bit of explaining. The spread between the interest rate CCC rated companies need to offer to borrow money and the interest rate B rated companies need to offer to borrow is a good indicator of business stress. That is because marginal businesses can shift around between those two categories as economic conditions change, and so the higher rates for being categorized as worse greatly impact the operations of those businesses.

It should be expected that at higher risk-free interest rates, the spread between the two categories would increase, as the costs of not being paid back would be higher for lenders, making them demand a higher risk-premium. Therefore, as the Fed started to cut in 2024, it makes sense that the spread would decrease.

Since Trump has been president, however, that spread has been increasing, so that even though the current spread would not be unremarkable in the first half of 2024, it is elevated now. Illustrated another way:

Code

# Construct a clean dataframe with only the columns of valuedf1 =DataFrame(; date=ccc.date, ccc=ccc.value, b=b.value, )df2 =DataFrame(; date=effr.date, effr=effr.value, )# Join the two dataframes on date so that the extra values from effr are omitteddf =leftjoin(df1, df2, on=:date)plot(df.date, (df.ccc .- df.b) .- df.effr; xlabel="Date", ylabel="(CCC - B Spread) - Risk-Free Rate", label="", title="Rising Peril for Marginal Businesses", linewidth=2, legend=:topleft)vline!([Date(2025,1,20)], label="Inaguration", linestyle=:dash)vline!([Date(2025,4,2)], label="Tariff Announcement", linestyle=:dash)

Higher Deficits

Despite Record Tariff Revenue, House Republicans’ Tax Cuts For The Rich Would Still Lead To A Massive Deficit Increase. According to Bloomberg, “Daily revenue from US customs duties rose to a record $16.5 billion as American importers made monthly payments to the government for goods received in April. That revenue, disclosed in Treasury Department data released Friday, reflects the full impact of President Donald Trump’s new universal tariffs for the first time. About two-thirds of importers pay customs duties in one monthly sum — the month after goods arrive in US ports — and the deadline for April payments was Wednesday. If tariffs continue at the present rate, the data suggest that Trump will fall short of the $2 billion a day in tariff revenue he’s counting on to help pay for the record tax cuts included in a bill passed by the House of Representatives this week.” [Bloomberg, 2025-05-23]

NOTE: Because of the somewhat confusing wording, it is necessary to note that the $2 Billion a day figure would result in a single-day payment of closer to $50 Billion due to the high concentration of firms paying all of their tariffs at once (for the month).

Corruption

May 2025: Trump Media (The Company Behind Truth Social) Announced Plans To Raise $3 Billion To Purchase Cryptocurrencies. According to the Financial Times, “The Trump family media company plans to raise $3bn to buy cryptocurrencies such as bitcoin, in a bet on the kind of digital assets that have been championed by the US president’s administration. Trump Media & Technology Group, which is behind the Truth Social app and controlled by the president’s family, aims to raise $2bn in fresh equity and another $1bn via a convertible bond, according to six people briefed on the matter. TMTG’s capital raising could be announced ahead of a big meeting of crypto investors and advocates in Las Vegas this week, where vice-president JD Vance, Trump’s sons Donald Jr and Eric, and Trump’s crypto tsar David Sacks are expected to speak. The terms, timing and size of TMTG’s capital raising could still change. Two people familiar with the plans told the Financial Times that the offering had been increased in size in recent weeks due to strong demand.” [Financial Times, 2025-05-26]

Volatility Enhancement

As I noted in April, the appeal of convertible bonds is to arbitragers in a bet on volatility. One thing that has characterized markets under Trump has been notable volatility, especially volatility in response to something he controls: his pronouncements.

[Apollo,

[Apollo,  [Apollo,

[Apollo,