Continued unemployment claims look to have jumped since Trump announced his main tariffs, while mortgage rates surging and pending home sales dropping 6.3% - more than six times economists’ predictions. Consumer-facing businesses are struggling, with marginal retailers like At Home preparing for bankruptcy specifically citing tariff impacts. Prices for furniture and electronics have risen unusually sharply. The FOMC has expressed concerns about stagflationary preassure and while GDP growth was revised up to show a 0.2% annualized decline in Q1 2025, consumer spending growth–a source of strength for several years–was revised downward.

On the international front, Trump’s unilateral approach is undermining America’s global economic leadership and creating dangerous capital flight risks. ASEAN leaders have publicly criticized the tariff approach as creating “uncertainties” and announced plans to diversify trade beyond traditional U.S. markets, while foreign investment in dollar-denominated assets has dropped 19% in the first five months of 2025.

In some good news, a federal trade court unanimously ruled Trump’s emergency declaration justifying the tariffs was illegal, though an appeals court has temporarily paused implementation of that ruling.

While Fed officials warn that loss of America’s safe-haven status could have “long-lasting implications for the economy,” Trump’s CEA chair has continued to spout off about the negative impacts of the United States being an attractive place to invest.

Trade War

Lifecycle Model Simulation Of Trump’s Proposed Tariffs: The Effects Of A Reduction In The Capital Stock Driven By Tariff-Induced Higher Prices Led To More Than Twice The Welfare Costs As A Model Holding Capital Constant. According to Baqaee and Malberg, “This short note shows that accounting for capital adjustment is critical when analyzing the long-run effects of trade wars on real wages and consumption. The reason is that trade wars increase the relative price between investment goods and labor by taxing imported investment goods and their inputs. This price shift depresses capital demand, shrinks the long-run capital stock, and pushes down consumption and real wages compared to scenarios when capital is fixed. We illustrate this mechanism by studying recent US tariffs using a dynamic quantitative trade model. When the capital stock is allowed to adjust, long-run consumption and wage responses are both larger and more negative. With capital adjustment, U.S. consumption can fall by 2.6%, compared to 0.6% when capital is held fixed, as in a static model. That is, capital stock adjustment emerges as a dominant driver of long-run outcomes, more important than the standard mechanisms from static trade models — terms-of-trade effects and misallocation of production across countries.” [Baqaee and Malberg, 2025-04]

What this means

The model Baqaee and Malberg explore shows the pernicious effects of the following mechanism: investment in capital stock requires imported components, which, being more expensive raise the cost of capital. As a result, less is invested, which leads to a lower standard of living in the long run.

Weaker Global Standing

May 2025: ASEAN Leaders Issued A Statement Calling Out Trump’s Unilateral Approach To Trade Policy. According to Bloomberg, “Southeast Asian leaders called out President Donald Trump’s tariff plans as causing uncertainties in commerce with their region’s largest export customer and underscoring an ‘urgency of diversifying trade beyond traditional markets.’ ‘We express deep concern over the recent announcement by the United States to impose unilateral tariffs and their potential impact on our economies,’ the leaders said, according to a statement by the chairman of the Association of Southeast Asian Nations released Tuesday night. The leaders met this week in Kuala Lumpur, Malaysia, for a summit that included high-profile delegations from China and the Gulf States. ‘The uncertainties arising from these tariffs and potential retaliation could heighten volatility in both capital flows and exchange rates,’ the statement said, adding that Asean would ‘continue to engage in a frank and constructive dialogue with the US, and commit not to impose any retaliatory measures in response to US tariffs.’” [Bloomberg, 2025-05-27]

Consequences

May 2025: FOMC Meeting Minutes Revealed That Members Of The Committee Projected Stagflationary Preassure. According to the Wall Street Journal, “Federal Reserve officials signaled concern at their meeting earlier this month that large tariff hikes would push up prices and could risk stoking higher inflation. Policymakers largely agreed that heightened economic uncertainty and increased risks of both higher unemployment and inflation warranted no change in their wait-and-see policy stance, according to minutes of the May 6-7 meeting released Wednesday. ‘Participants agreed that uncertainty about the economic outlook had increased further, making it appropriate to take a cautious approach until the net economic effects of the array of changes to government policies become clearer,’ said the minutes.” [Wall Street Journal, 2025-05-28]

Weaker Growth

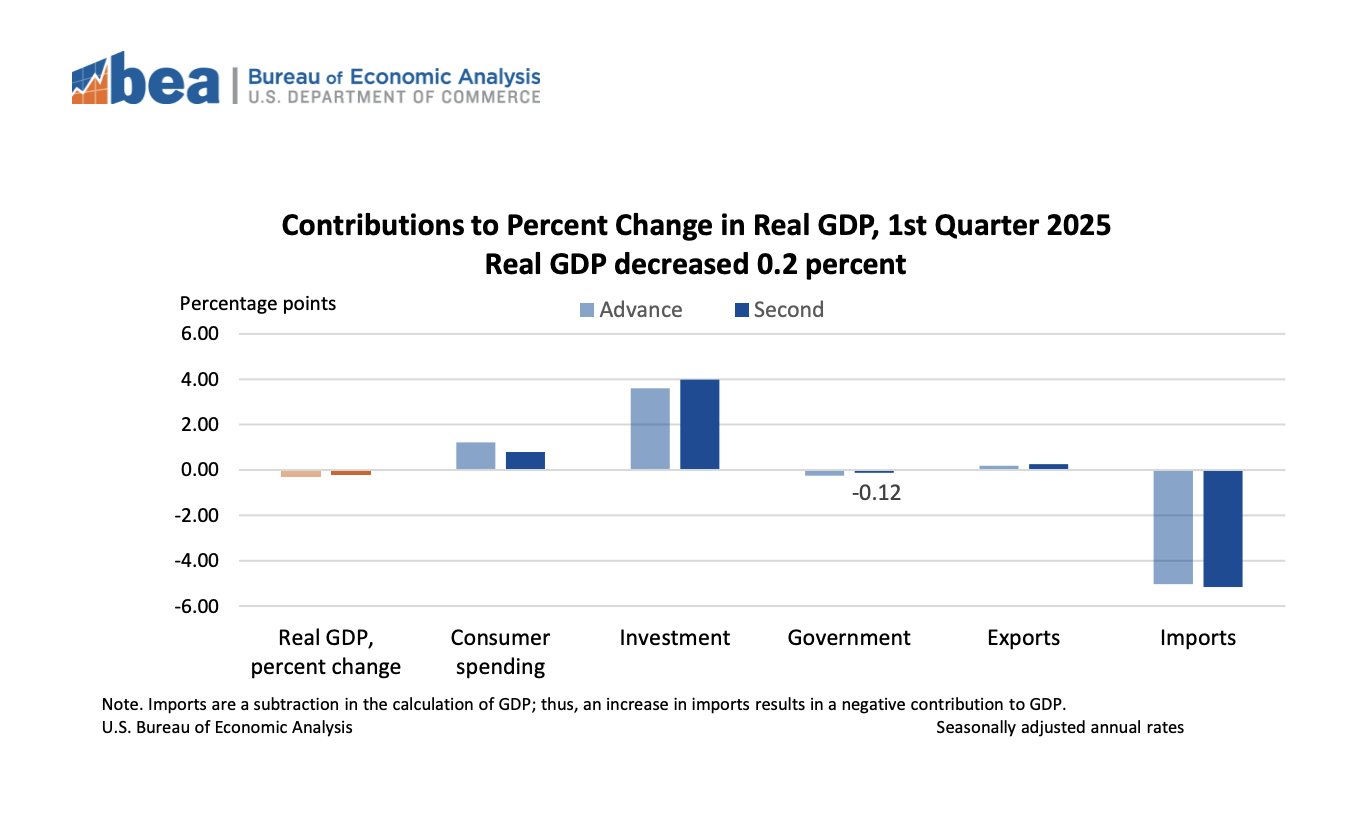

Q1 2025: While GDP Growth Was Revised Upwards To A Drop At A 0.2 Percent Annualized Rate, Consumer Spending Growth Was Revised Downward. [Bureau of Economic Analysis, 2025-05-29]

May 2025: At Home, The Home Decour Reatiler Prepaired To File For Bankruptcy As Trump’s Tariffs Hurt The Business. According to Bloomberg, “At Home Group Inc. is preparing to file for bankruptcy under a Chapter 11 reorganization in the coming weeks, among other options to shore up liquidity, according to people with knowledge of the matter. The Hellman & Friedman-owned home-decor retailer has been facing a cash crunch in recent months, which has been complicated further by the US’ tariffs and trade war. The company did not make its interest payment on May 15 and entered a forbearance pact with lenders on May 23, according to separate people with knowledge of the matter, who asked not to be identified discussing private information. The reprieve runs through June 30, the people said.” [Bloomberg, 2025-05-27]

Employment

Code

# Load custom plot themeinclude("../scripts/oxocarbon-plot.jl")theme(:oxocarbon)# Set up the Fred APIusingFredData, DataFrames, Dateskey =ENV["FRED_API_KEY"]f=Fred(key)# Load Dataweekly=get_data(f, "CCSA"; observation_start="2024-05-16", observation_end="2025-05-18").dataweekly_ma=get_data(f, "CC4WSA"; observation_start="2024-05-16", observation_end="2025-05-18").data# Make plotsplot(weekly.date, weekly.value ./1_000; title="Continued Unemployment Jumped After Trump's Tariffs", xlabel="Date", ylabel="Continued Unemployment Claims (Thousands)", label="Weekly", linewidth=1,)plot!(weekly_ma.date, weekly_ma.value ./1_000; label="4-Week Moving Average", linewidth=2, )vline!([Date(2025,4,2)]; label="Tariff Announcement", linestyle=:dash,)vline!([Date(2025,1,20)]; label="Inaguration", linestyle=:dash,)

NOTE: This could by a bit of cyclically, but it is something to take a note of.

Housing

April 2025: Pending Homes Sales Dropped By 6.3 Percent, More Than Six Times As Much As Economists Surveyed By Reuters Predicted. According to Reuters, “Contracts to buy U.S. previously owned homes fell more than expected in April as rising mortgage rates and economic uncertainty weighed on demand. The National Association of Realtors (NAR) said on Thursday its Pending Home Sales Index, based on signed contracts, dropped 6.3% to 71.3 last month. Economists polled by Reuters had forecast contracts, which become sales after a month or two, falling 1.0%. Pending home sales declined 2.5% from a year earlier.” [Reuters, 2025-05-29]

Code

# Get Datam30 =get_data(f, "MORTGAGE30US"; observation_start="2025-03-27", observation_end="2025-05-29").datam15 =get_data(f, "MORTGAGE15US"; observation_start="2025-03-27", observation_end="2025-05-29").data# Make Plotplot(m30.date, m30.value; title="Post-Tariffs, Mortgate Rates Have Surged", xlabel="Date", ylabel="30 Year Rate", label="30 Year", linewidth=2,)right_axis=twinx()plot!(right_axis,m15.date, m15.value; label="15 Year", linewidth=2, color=colorant"#525252", ylabel="15 Year Rate", )vline!([Date(2025,4,2)], label="Tariff Announcement", color=colorant"#673AB7", linestyle=:dash)

Higher Prices

May 2025: FOMC Officials Noted Trump’s Tariffs Were Likely To Raise Inflation. According to the Financial Times, “The early May FOMC meeting was the first after the turmoil that followed Donald Trump’s ‘liberation day’ tariff announcements on April 2. The falls in stocks and treasuries, combined with the dollar’s depreciation, broke with historical trends and sparked concern that Trump’s policies were leading global investors to ditch the dollar and US assets. Global investors have historically flocked to — not away from — US assets in times of market volatility. The FOMC minutes did not speculate on what the implications for the US economy could be if it lost its status as a perceived safe haven. Phillip Swagel, director of the non-partisan Congressional Budget Office, told the Financial Times this month that a shift in capital flows away from the US would dent growth, hit jobs and raise government borrowing costs. The minutes also showed that Fed officials thought Trump’s trade war had increased the chances that inflation would remain above the central bank’s 2 per cent goal. ‘Almost all participants commented on the risk that inflation could prove to be more persistent than expected,’ the minutes said.” [Financial Times, 2025-05-28]

WSJ Headline: Your Patio Furniture Set Is Going to Cost A Lot More This Summer [Wall Street Journal, 2025-05-26]

April 2025: While Apparel Prices Did Not Increase In Line With What Were Expected With Tariffs, Furniture And Electronics Prices Jumped By More Than Normal. According to Ernie Tedschi in Bloomberg, “First, the CPI was more of a mixed bag with regards to tariffs rather than a solid rebuttal. Apparel prices fell by 0.2% in April, which is telling given how much apparel the US imports, from China in particular. But electronics and furniture prices — goods also highly exposed to tariffs — rose 0.75% and 1.5%, which are unusually big increases for those categories.” [Ernie Tedschi in Bloomberg, 2025-05-28]

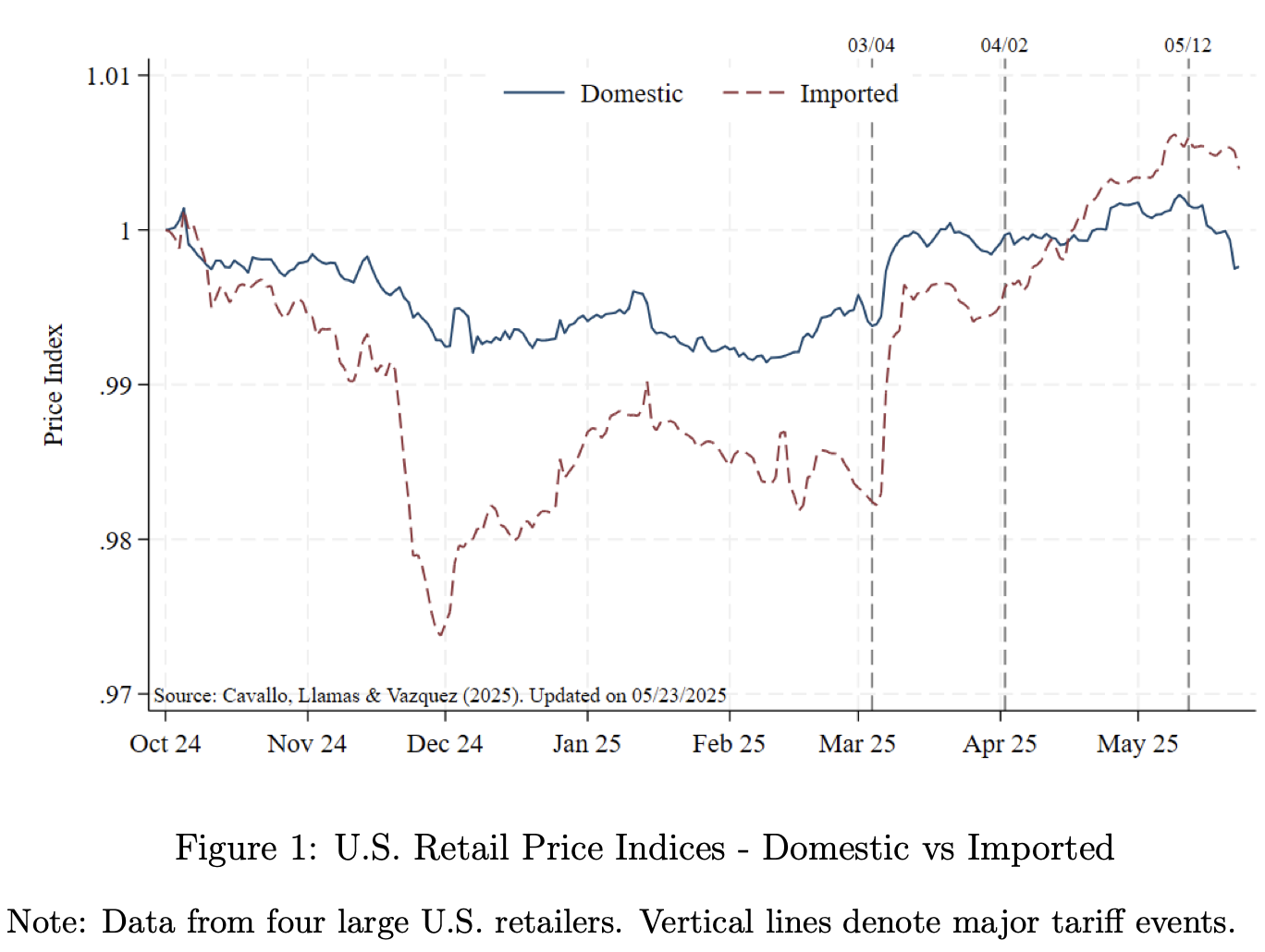

High-Frequency Analysis Of Retailer Prices Showed Tariff-Exposed Goods’ Prices Climbing Significantly Faster Than Other Goods. According to Ernie Tedschi in Bloomberg, “Tariffs are likely also showing up in more high frequency price data. Findings scraped from large US online retailers and compiled by economists Alberto Cavallo, Paola Llamas, and Franco Vazquez suggest that domestic-origin goods prices are up roughly half a percent since early March, while foreign-origin goods prices are up more than two percent. The timing of these price increases lines up almost exactly with White House tariff announcements in March and April.” [Ernie Tedschi in Bloomberg, 2025-05-28]

May 2025: Fed Governor Williams Expressed Concern That Post-Covid Inflation Had Changed Consumers’ Expectation That Long-Term Inflation Would Be Stable. According to Bloomberg, “Federal Reserve Bank of New York President John Williams said pandemic-era price shocks changed American consumers” inflation perceptions, and policymakers can’t take for granted that people’s estimates of future price increases will remain anchored. ‘The past five years have, I think, changed people’s perceptions of inflation,’ Williams said Wednesday in Tokyo during a conference at the Bank of Japan. Policymakers should aim to anchor not only longer-term estimates of future consumer price increases, but ‘the whole curve,’ he added. ‘The thing you want to avoid is allowing inflation to become highly persistent, because highly persistent can kind of become permanent,’ he said. Several household-based surveys have shown consumers” views of the economy worsening and their estimates for near-term consumer price increases rising in recent months, following a raft of tariff announcements from the Trump administration. Market-based measures of future inflation, however, and surveys conducted by the New York Fed still point to longer-term estimates that remain around the central bank’s 2% inflation target.” [Bloomberg, 2025-05-28]

Illegality Ruling

April 2025: The Trump Administration Moved To Transfer A Case Challenging The Power He Claimed To Impose The Tariffs To An Appeals Path Deemed More Deferential To Presidential Power: The U.S. Court Of International Trade. According to Bloomberg, “President Donald Trump wants legal challenges to his sweeping tariffs to be heard by a specialized trade court, an approach that worked in his favor during his first administration even though it didn’t give him an immediate victory. The Trump administration is seeking to transfer three cases filed in federal courts in Florida, Montana and California to the US Court of International Trade, or CIT, whose judges handle technical disputes over tariffs. That court ruled against the president in lawsuits targeting his 2018 steel tariffs, but Trump emerged victorious when an appeals court sided with him. Legal experts say that steering the current cases on the same path will likely benefit the administration because they, too, would go through the US Court of Appeals for the Federal Circuit, which has historically been deferential to the authority of presidents to levy tariffs.” [Bloomberg, 2025-04-23]

April 2025: The Trump Administration Told The U.S. Court Of International Trade That It Was Not The Body That Could Review His Emergency Declaration. According to Bloomberg, “The Trump administration asked the US trade court to reject a lawsuit by small businesses challenging the president’s global tariffs, arguing that judges don’t have the authority to review the national emergency he invoked to justify the sweeping levies. The businesses are improperly questioning the veracity of President Donald Trump’s assertion of a national emergency, ‘inviting judicial second-guessing of the president’s judgment,’ the Justice Department said in a filing late Tuesday in the US Court of International Trade. Trump is attempting to stave off claims that his trade war is based on a false emergency and therefore illegal. The 78-year-old Republican issued the tariffs after asserting in an executive order that US trade deficits had become a major threat to national security and military readiness. ‘Congress designated itself — not the judiciary — as the body to supervise emergency declarations and the adequacy of the president’s response,’ said the government.” [Bloomberg, 2025-04-30]

Despite Claims By The Justice Department That This Ruling Would Prevent Trump From Striking Deals, A Judge Said The Court Could Not Allow Him To Do “Something He’s Not Allowed To Do By Statute.” According to the Financial Times, “During the Oregon hearing, Department of Justice lawyer Brett Shumate said an injunction against the tariffs ‘would completely kneecap the president’ when he was on the world stage trying to strike trade deals. Judge Jane Restani replied that the court could not for political reasons allow the president to do ‘something he’s not allowed to do by statute’.” [Financial Times, 2025-05-28]

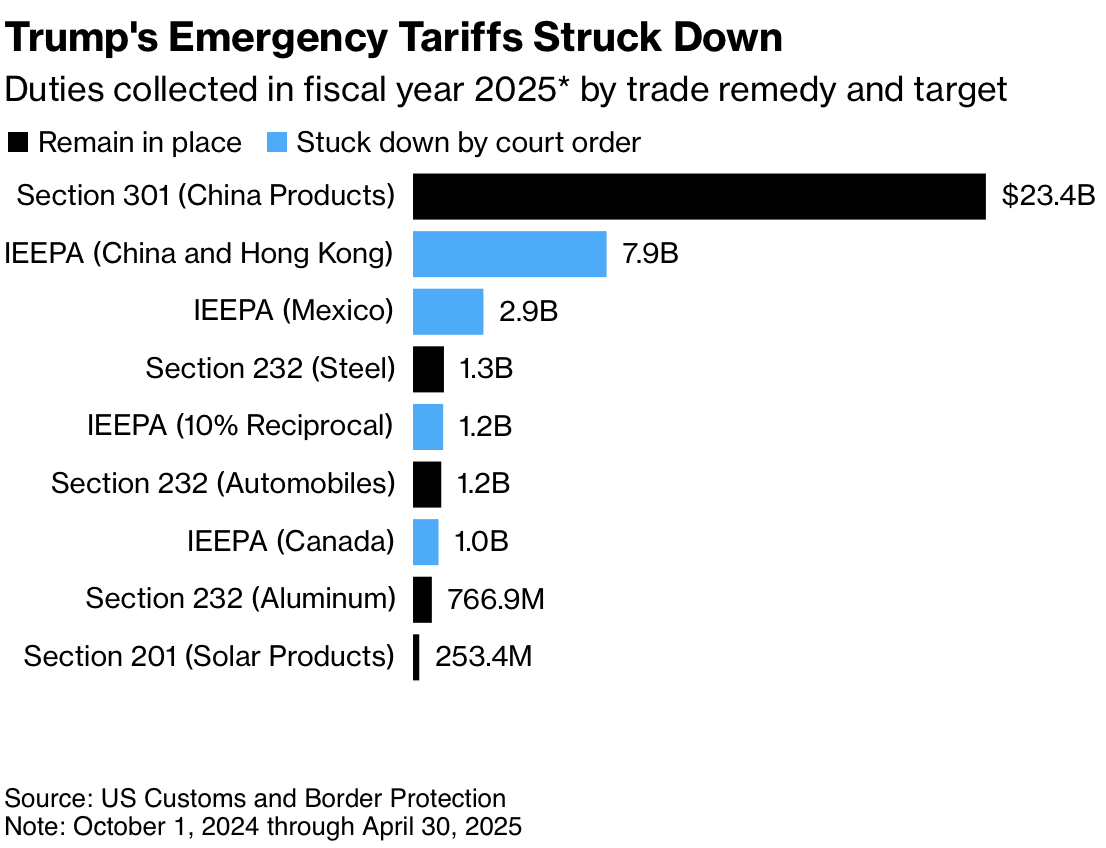

May 2025: The U.S. Court Of International Trade Ruled Unanimously–In A Summary Judgement–That Trump’s Declearation Of Emergency To Justify His “Reciprocal Tariffs” Was Illegal, But Did Not Give An Explict Remedy. According to Bloomberg, “The vast majority of President Donald Trump’s global tariffs were deemed illegal and blocked by the US trade court, dealing a major blow to a pillar of his economic agenda. A panel of three judges at the US Court of International Trade in Manhattan issued a unanimous ruling Wednesday which sided with Democratic-led states and small businesses that accused Trump of wrongfully invoking an emergency law to justify the bulk of his levies. The court gave the administration 10 days to ‘effectuate’ its order, but didn’t spell out any steps it must take to unwind the tariffs. […] The judges rejected the government’s argument that Trump had authority to unilaterally issue tariffs under a law intended to address financial transactions during national emergencies. The ruling was a so-called summary judgment, meaning a final victory for the plaintiffs in lower court without the need for a trial.” [Bloomberg, 2025-05-28]

While The Administration Signaled Plans To Appeal The Ruling, The Tariffs Would Not Be In Effect Until A Higher Court Said So. According to Bloomberg, “The Justice Department filed a notice of appeal with the US Court of Appeals for the Federal Circuit. The US Supreme Court may ultimately have the final say in the high-stakes case that could impact trillions of dollars in global trade. For now, the ruling permanently blocks the tariffs unless the appeals court allows Trump to reinstate them during litigation.” [Bloomberg, 2025-005-28]

In Contrast To The Trump Administration’s Request, The Court Ruled That The Tariffs Were Illegal For Everyone, Not Just The Plaintiffs. According to Bloomberg, “The Trump administration argued in court filings that the plaintiffs are improperly questioning his executive orders, ‘inviting judicial second-guessing of the president’s judgment.’ The government had asked the panel of judges to issue only a narrow ruling if they were to rule in favor of the plaintiffs, but the court concluded that wasn’t possible given the nature of the tariffs. ‘There is no question here of narrowly tailored relief; if the challenged tariff orders are unlawful as to plaintiffs they are unlawful as to all,’ the panel said.” [Bloomberg, 2025-05-28]

The Court Ruled That It Would Be Unconstitutional For Congress To Give All Of Its Tariff Powers To The President. According to the Wall Street Journal, “Wednesday’s ruling said it would be unconstitutional for Congress to delegate ‘unbounded tariff power’ to the president. ‘An unlimited delegation of tariff authority would constitute an improper abdication of legislative power to another branch of government,’ the court said. Congress placed limits in IEEPA, restricting when and how a president could place levies, the ruling said. The panel also said the U.S. trade deficit didn’t fit the law’s definition of an unusual and extraordinary threat.” [Wall Street Journal, 2025-05-28]

The Court Ruled That The Trade Deficit Did Not Constitute A National Emergency. According to the Wall Street Journal, “Wednesday’s ruling said it would be unconstitutional for Congress to delegate ‘unbounded tariff power’ to the president. ‘An unlimited delegation of tariff authority would constitute an improper abdication of legislative power to another branch of government,’ the court said. Congress placed limits in IEEPA, restricting when and how a president could place levies, the ruling said. The panel also said the U.S. trade deficit didn’t fit the law’s definition of an unusual and extraordinary threat.” [Wall Street Journal, 2025-05-28]

May 2025: An Appeals Court Temporarily Paused The Ruling Invalidating Trump’s Tariffs. According to Bloomberg, “A federal appeals court temporarily paused a ruling against President Donald Trump’s global tariffs while weighing a longer lasting hold. A brief order granting the stay was issued Thursday by the US Court of Appeals for the Federal Circuit.” [Bloomberg, 2025-05-29]

Weaker Growth

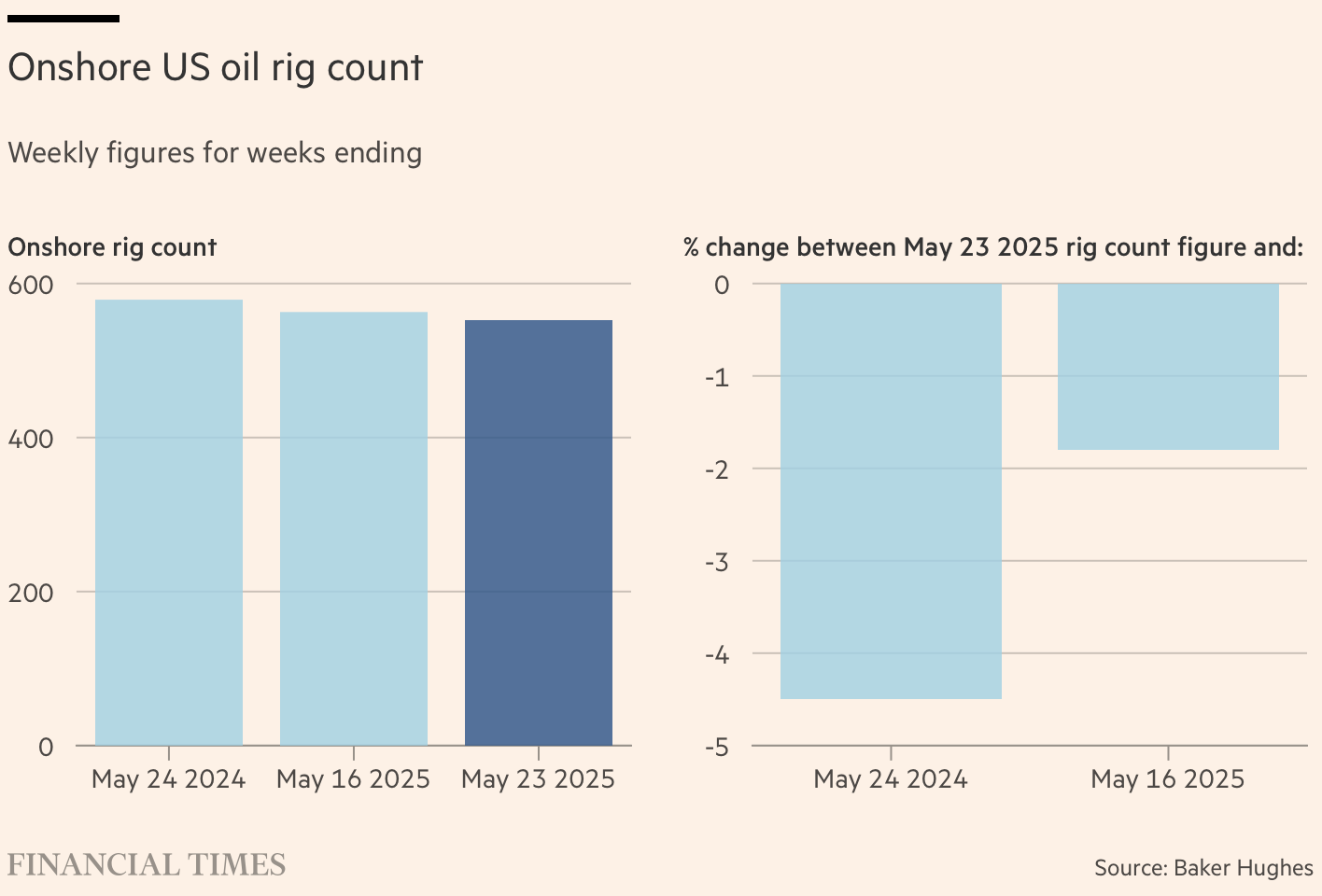

S&P Global: As Oil Prices Have Fallen Below Fracking Breakevens, Oil Production May Fall In 2026. According to the Financial Times, “US oil companies are cutting spending and idling drilling rigs, as Donald Trump’s tariffs push up costs and falling crude prices squeeze profits, prompting executives to warn that a decade-long shale boom is ending. Surprise decisions by the Opec+ cartel to pump more oil have compounded the gloom across the US oil patch, sparking fears of a new price war and prompting analysts to cut output forecasts. ‘We”re on high alert at this point,’ Clay Gaspar, chief executive officer at Devon Energy in Oklahoma City, told investors this month. ‘Everything is on the table as we move into a more distressed environment.’ Oil output will fall by 1.1 per cent next year to 13.3mn barrels a day, according to S&P Global Commodity Insights, as prolific shale drillers that made the US the world’s biggest producer idle rigs in the face of prices driven lower by fears of oversupply and Trump’s trade war. That would mark the first annual decline in a decade, excluding the 2020 pandemic when collapsing demand sent oil prices below zero and triggered widespread bankruptcies across states such as Texas and North Dakota. US oil prices settled lower again on Friday, ending the week at $61.53 a barrel, down about 23 per cent from its high point this year. Shale producers need an oil price of $65 a barrel to break even, according to the quarterly energy survey by the Federal Reserve Bank of Dallas.” [Financial Times, 2025-05-25]

May 2025: Amid Low Oil Prices Favored By Trump, The Number Of Oil Rigs Have Dropped. [Financial Times, 2025-05-25]

Big Beautiful Bill

House Republicans’ Tax Bill Would Raise Taxes On University Endowments To A Level Equal To Corporations, Without Allowing Many Of The Same Deductions Corporations Can Take. According to Matt Levine in Bloomberg, “The basic situation is that a corporation has revenue, and then it pays its expenses (salaries, etc.), and what’s left over is net income. And, in the US, the corporation pays 21% of its net income to the federal government as income tax; the rest belongs to its shareholders. Meanwhile the situation for a big US university is that it has an endowment, and the endowment generates investment income, and if the university is big and rich enough it pays 1.4% of that income to the federal government as an excise tax. And that might change to 21% under the new tax bill. […] Notice, though, the discrepancy in my first two paragraphs. Corporations pay a tax of 21% on the difference between their revenue and their expenses. Universities would pay a tax of 21% on their investment income, with, as far as I can tell, no ability to deduct regular operating expenses.4 A corporate executive’s salary is tax deductible, but a university professor’s salary isn”t. ‘The 21% rate matches the corporate tax rate, but the effective tax rate on some schools could in some cases be higher than what for-profit corporations pay, as nonprofits can’t claim certain deductions the way corporations can,’ the Journal notes.” [Matt Levine in Bloomberg, 2025-05-28]

With Higher Tax Rates On Endowments Than Corporations, It Would Make Sense For Universities To Essentially Convert Endowments To Corporations, Driving Their Tax Liabilities Near Zero. According to Matt Levine in Bloomberg, “That does suggest the germ of a trade, doesn’t it? At big universities, endowment income largely pays for salaries for professors, administrators, football coaches, etc. Those salaries presumably would not be deductible against an endowment excise tax. It is not that uncommon for professors at big research universities to work on topics — biopharmaceuticals, artificial intelligence, whatever — that have commercial potential. Sometimes there are arrangements: Work that a professor produces in her lab at the university, using the university’s resources and her graduate students’ work, can be commercialized, with some deal in which the professor and the university and a for-profit company all share in the value. And then if it becomes hugely valuable the university gets a big capital gain, in its endowment, somewhere down the line. In the current framework, a big capital gain is good, for the university. In a 21% excise tax framework, it is less good. (It’s 21% less good.) In the excise-tax framework, $100 of endowment income would pay for $79 of professors’ salaries. But if a for-profit corporation were to pay $100 of professors’ salaries, that payment would be tax-deductible (for the corporation). And so the trade is something like: The for-profit Chemistry Corporation hires all of Harvard’s chemistry professors, sets them up with labs, buys their equipment and pays their graduate students. Let’s say the operating budget of the chemistry department is $8 million, a number I just made up. The Chemistry Corporation takes over the responsibility for that budget. Harvard invests $100 million in the Chemistry Corporation and gets 95% of the stock; the professors get the rest. The Chemistry Corporation re-invests that cash with whoever currently manages Harvard’s endowment, targeting an 8% annual return. The Chemistry Corporation makes $8 million a year on its investments, and pays $8 million a year in operating expenses, for a net income of $0. It pays no taxes, because it has no net income. Harvard doesn’t pay any excise tax on the return on its $100 million Chemistry Corporation investment, because that return is zero. Harvard also rents office space to the Chemistry Corporation (not taxable, because not investment income?) and pays, you know, $1 a year for the Chemistry Corporation to provide teachers for undergraduate chemistry classes. I guess if they discover a valuable new chemical that’s gravy There is a precisely analogous approach for the Harvard Professional Football Team Inc., though it could also earn revenue from ticket sales. Or for the Classics Corporation, which probably couldn’t. This is extremely not tax advice, but you get the idea, right? On the current model, Harvard earns an endowment income, which it uses to pay its expenses. In a world of 21% excise tax, there would be a 21% slippage between the endowment income and the paying of expenses. But Harvard’s endowment income is generally less than its expenses. If you could pay the expenses before income becomes endowment income, you would avoid the slippage: $1 of expenses would reduce endowment income by $1. The big university endowments are already adventurous long-term investors, and “directly investing in private companies … could be attractive” for them. Perhaps for the tax deductions.” [Matt Levine in Bloomberg, 2025-05-28]

Capital Flight

Eurizon SLJ Capital CEO: Capital Flight May Drain $2.5 Trillion From The U.S. Economy. According to Bloomberg, “The switch from hoarding dollar assets to doubting US exceptionalism may send $2.5 trillion or more cascading through global markets, according to Eurizon SLJ Capital Chief Executive Officer Stephen Jen. In that scenario, emerging-market currencies will soar against the dollar, equities from Europe to Japan will benefit from inflows, while new capital swells debt markets in countries including Australia and Canada, asset managers and analysts said.” [Bloomberg, 2025-05-27]

May 2025: Taiwanese Insurers Faced The Prospect Of $18 Billion In Losses From Unhedged Dollar Investments. According to Bloomberg, “In early May, speculation built that Taiwan would be asked to strengthen its currency as part of US trade talks. A two-day surge in the Taiwan dollar shocked traders and companies alike. The speed of the advance — unseen since at least the 1980s — threatened to sink the value of the $294 billion of Treasuries held by Taiwan, some of it by the island’s life insurers, which hadn’t hedged for such a development. After all, the currency had weakened against the dollar in the prior three years. Its government said later that more than 90% of the companies’ overseas investments were dollar denominated. Even before that shock, Taiwanese life insurers — which were in effect recycling the trade surplus earned from the island’s semiconductor exports to the US — had posted a $620 million loss in April from the market volatility triggered by Trump’s tariffs. Goldman Sachs Group Inc.’s analysts estimated that a 10% appreciation in the Taiwan dollar could lead to $18 billion in unrealized currency loss for insurers, wiping out capital reserves.” [Bloomberg, 2025-05-27]

April 2025: One Of Australia’s Biggest Pension Funds Signaled That Its Exposure To American Assets Had Probably Peaked. According to Bloomberg, “UniSuper, one of Australia’s biggest pension funds with A$149 billion ($96 billion) of assets, said in early April that its investments in the US have probably peaked and plans to cut exposure as Trump “is turning out to be horrible for business.” This marked an about-turn from February when it was part of an industry road show looking for ways to invest more.” [Bloomberg, 2025-05-27]

May 2025: FOMC Officials Noted Concerns About The Impact Of Capital Flight From The United States. According to the Financial Times, “Federal Reserve officials have warned that the loss of the US’s safe-haven status triggered by President Donald Trump’s global trade war could have ‘long-lasting’ effects on the country’s economy. Minutes from the Federal Open Market Committee’s early May vote, published on Wednesday, indicated that some rate-setters focused on the fall in prices for US government debt, equities and the dollar in the weeks after the president announced sweeping tariffs on trading partners. ‘These participants noted that a durable shift in such correlations or a diminution of the perceived safe-haven status of US assets could have long-lasting implications for the economy,’ the minutes said. The early May FOMC meeting was the first after the turmoil that followed Donald Trump’s ‘liberation day’ tariff announcements on April 2. The falls in stocks and treasuries, combined with the dollar’s depreciation, broke with historical trends and sparked concern that Trump’s policies were leading global investors to ditch the dollar and US assets.” [Financial Times, 2025-05-28]

May 2025: Hong Kong’s Pension Regulator Directed Funds To Draw Up Plans To Sell Off Treasuries In The Event Of Another Downgrade. According to Bloomberg, “Hong Kong’s pensions regulator has pushed back against requests to change rules that would require funds to sell Treasuries in the event of another US ratings downgrade, and instead told funds to draw up ‘contingency plans.’ The Mandatory Provident Fund Schemes Authority, which regulates Hong Kong’s pension system, said in an emailed statement Wednesday it had ‘urged MPF trustees to evaluate the potential implications if the US loses its last AAA rating by an approved agency.’ Funds operating under the city’s HK$1.3 trillion ($166 billion) MPF system are only allowed to invest more than 10% of their assets in Treasuries if the US has a AAA or equivalent credit score from an approved agency. After Moody’s Ratings” downgrade earlier this month, the only remaining such score is from Japan’s Rating & Investment Information Inc. The city’s pension funds had asked the authority to reconsider this requirement. But in its statement it the MPFA said it has ‘no plan to amend the relevant regulations.’ Instead it said fund managers ‘must formulate suitable compliance contingency plans and make timely and orderly adjustments to their asset allocation in response to possible market developments.’” [Bloomberg, 2025-05-28]

January - May 2025: Dollar-Denominated Debt Issuance By Non-US Sovereigns Dropped 19 Percent. The First Such Drop In More Than Three Years, As Higher Interest Rates And A Weaker Currency Made It Less Attractive. According to Reuters, “Governments in Asia and Europe are raising far less debt in U.S. dollars than usual, preferring to issue at home as they avoid exposure to rising U.S. yields, currency volatility and broader concerns about U.S. government finances. According to Dealogic data, issuance of dollar bonds by non-U.S. sovereigns dropped 19% to $86.2 billion in the first five months of this year compared with the same period last year, marking the first decline in three years. The January-May dollar bond issuance by the governments of Canada and Saudi Arabia fell 31% and 29% to $10.9 billion and $11.9 billion, respectively, while issuance by Israel and Poland declined 37% and 31% to $4.9 billion and $5.4 billion. At the same time, Dealogic data showed global sovereigns’ local currency bond issuance had climbed to a five-year high of $326 billion so far this year. This drop in dollar bond issuance comes at a time when global investors are pulling back from U.S. assets, partly in response to tariffs and as they question U.S. financial dominance and safety.” [Reuters, 2025-05-29]

Stephen Miran Saw The $26 Trillion More Foreigners Have Invested In The United States Than Americans Have Invested Abroad As A Problem. According to Bloomberg, “Stephen Miran, chair of the Council of Economic Advisers, sees it differently. The large claims that foreigners have on American assets are a potential risk, he argued in an interview with Saleha Mohsin for the latest weekly Bloomberg Big Take DC podcast. Subtracting out American holdings overseas, the US net international investment position is a negative $26 trillion. “This minus-$26 trillion is a massive latent financial stability risk,” Miran said. While not a danger right now, “it could morph into one, one day,” he said. This is another reason for dealing with the trade deficit, he argues. If foreigners aren’t earning as many dollars selling stuff to Americans, they won’t have the greenbacks to keep adding to their holdings of US assets.” [Bloomberg, 2025-05-28]

Miran Saw Parallels To The Eurozone’s Debt Crisis. According to Bloomberg, “If the current net debtor figure were to swell to a negative $40 trillion or $50 trillion, ‘that’s when you sort of get to crisis level,’ Miran says. (It’s already more than doubled from 2019, when it weighed in at less than $12 trillion.) The scenario he invokes is Europe’s crisis of more than a decade ago, which saw foreign investors yank cash out of European Union members with high debt loads, such as Greece. ‘What we saw with the EU, 14 years ago, is you don’t want to let it get there, right — you want to deal with it now,’ he says of imbalances.” [Bloomberg, 2025-05-28]

Miran: Service Exports Don’t “Shore Up National Security.” According to Bloomberg, “Miran also says that, when it comes to assessing the balance of trade, services don’t count the way that goods do. While the US goods-trade deficit is massive, at $1.2 trillion for 2024, it runs a surplus in services — amounting to $293 billion last year. Miran says a services surplus is all well and good, and he”d like to even see that expand. But ‘it doesn’t help shore up national security.’ For that, you need to be making goods that go towards things like rockets, bullets, tanks and ships, he argues. ‘You”re never going to be able to open the Red Sea’ by selling more financial ‘exotics,’ or ‘advertisements on the internet,’ Miran explains.” [Bloomberg, 2025-05-28]

Miran Is Wrong

The fact that foreign investment in the United States dwarfs American investment abroad is not, as Miran suggested, analogous to the Greece in the aftermath of the global financial crisis (GFC). Mainly, unlike Greece, not only do we control our own monetary policy, but we borrow entirely in the currency we control.

Also, the idea that service exports do not provide national security is based on a common Trump administration fallacy about what services are. For one thing, services provide soft power, something that has value if it is not being wielded by someone like Trump. For another thing, many of the services we export are vital to the production of goods we import.

Some in the Trump administration know this, hence the (misguided in my opinion) decision to enhance restrictions on chip design software exports announced yesterday.

Anti-Capitalism

As Part Of The Deal Trump Has Negotiated For The Japanese Takeover Of U.S. Steel, The U.S. Government Would Recieve Control Of Some Of The Company Decisions. According to Bloomberg, “The US government is poised to receive a so-called golden share in United States Steel Corp. as a condition for approving Nippon Steel Corp.’s proposed acquisition of the American company. The plan, which would give the government de facto veto rights on certain company decisions and appointments, is part of ongoing talks between authorities and the companies, according to people familiar with the matter. On Friday, President Donald Trump announced a ‘partnership’ that included $14 billion in new investments, but provided few additional details. Still unclear are the scope of such veto powers and what the administration has decided regarding the existing $14.1 billion takeover proposal. The deal put forward to the Committee on Foreign Investment in the US and to the President included the original $55-per-share acquisition along with extra investment, two people familiar with the matter said. The golden share — reported earlier by Nikkei — is set to be included as part of the national security agreement that’s typically drawn up to reflect conditional Cfius approvals, some of the people said, asking not to be identified as talks continue. It’s not clear whether the powers would amount to an equity stake or simply mitigation powers.” [Bloomberg, 2025-05-27]

While This Sort Of Arangement Has Been A Rarity In The U.S., Brazil And The U.K. Have Used It When Partially Privatizing State-Owned-Enterprises. According to Bloomberg, “This mechanism, which allows the owner to outvote other shareholders in certain circumstances, is a rarity in the US, where the government does not typically hold stakes in listed companies. But golden shares have been used elsewhere, including in Italy, Brazil and the UK — often to preserve state control over key decisions at privatized or strategic companies.” [Bloomberg, 2025-05-27]

Corruption

Trump Signed Legislation Blocking IRS Rules That Would Require Crypto Platforms To Report Transactions. According to Bloomberg, “In April, Trump also signed legislation to block an Internal Revenue Service rule due to take effect in 2026 that would have forced some cryptocurrency brokers to provide tax information on transactions conducted on their platforms.” [Bloomberg, 2025-05-28]

Directing Retirement Funds to Trump’s Friends

May 2025: Trump’s Department Of Labor Rescinded Guidance Against Crypto Exposure In 401(k) Plans. According to the Financial Times, “The US has opened the door to Americans purchasing crypto tokens in their retirement accounts, underscoring how Donald Trump is taking a far more tolerant approach to digital assets than his predecessor Joe Biden. The Department of Labor said on Wednesday it had rescinded previous guidance issued in 2022 for retirement plan managers and sponsors to exercise ‘extreme care before they consider adding a cryptocurrency option to a 401(k) plan’s investment menu,’ referring to a widely used employer-sponsored vehicle for US pension savings.” [Financial Times, 2025-05-28]

May 2025: Vance Praised Crypto Billionaires For Helping Trump Win The White House. According to the Financial Times, “The vice-president praised bitcoin investors for supporting Trump in the 2024 presidential race. He singled out billionaire donors Cameron and Tyler Winklevoss, co-founders of crypto platform Gemini, for winning over the Silicon Valley elites to Trump. ‘Thanks in particular for what you did for me and the president, helping us get from candidacy to the White House,’ he said to the bitcoin conference’s chair David Bailey.” [Financial Times, 2025-05-28]

PE Bailout

Q1 2025: Private Equity Fundraising Dropped 35 Percent Globally. According to Bloomberg, “Private equity firms have seen a sharp drop in fundraising this year, the latest sign of how a slowdown in dealmaking and initial public offerings has hurt an industry that’s struggling to return capital to investors amid high borrowing costs. PE fundraising plunged 35% to $116 billion globally in the three months through March compared to the same period in 2024, according to a study by data provider Pitchbook. The researcher said it ‘positions the annualized fundraising total to fall below 2024 levels’ of $531 billion, which was already weaker than years past.” [Bloomberg, 2025-05-27]

Trump’s SEC Has Started The Process Of Making It Easier To Put 401(k) Assets Into Private Equity. According to Brooke Masters in the Financial Times, “Now Donald Trump’s administration could throw open the doors. The Securities and Exchange Commission is rethinking rules that limit funds with more than 15 per cent in private assets to wealthy investors. And the White House may make it easier for corporate 401k plans, the primary US retirement savings vehicle, to put money into private assets as well.” [Brooke Masters in the Financial Times, 2025-05-28]

With Private Equity Struggling For Exits That Live Up To Paper Returns, Concerns Exist That Retirement Funds Could Bail Out Institutional Investors. According to Brooke Masters in the Financial Times, “The problem for PE is that volatile markets, higher interest rates and now uncertainty over tariffs have made it hard for firms to sell or float the assets that they own. The funds may report fabulous paper returns, but they have so far failed to crystallise, leaving existing investors strapped for ready cash. Private fund groups Blackstone, Apollo and KKR are seeking new blood. They have already teamed up with traditional asset managers to offer private funds to wealthy retail investors. But changing the SEC and 401k rules would widen the opportunity. Not only could the $9tn retirement market be fertile ground for raising new private funds, but it also could juice demand for buying stakes in existing ones, known as ‘secondaries’, allowing institutional investors to get out. The potential for trouble is huge. There is already evidence that retail private funds are paying over the odds, shelling out on average 4 per cent more last year for secondary stakes than traditional buyers. Perhaps they are better at spotting good opportunities than those buying for institutional clients. Perhaps not.” [Brooke Masters in the Financial Times, 2025-05-28]

Genius Act

The Stablecoin Legislation That Made It Through A Procedural Hurdle In The Senate Prohibited Stablecoins From Paying Interest. According to Robert Armstrong in the Financial Times, “It is striking that the act specifies that a stablecoin ‘is not a deposit . . . including a deposit recorded using distributed ledger technology’, but it’s important not to get caught up in terminology. If it quacks like a duck, and so on. It is also striking that the act insists that a stablecoin ‘does not offer a payment of yield or interest’. There are two ways to look at this latter point. You might say it’s a handout to the crypto industry; who wouldn’t want to run the sort of bank that is legally forbidden to pay depositors interest? On the other hand, you might see it as a safeguard; if issuers are not allowed to invest in longer-term, higher-yielding assets, it is better for the solvency of the industry that they don’t compete on yield.” [Robert Armstrong in the Financial Times, 2025-05-27]

The Genius Act Would Require Stablecoin Backing That Could Bear Interest. According to Robert Armstrong in the Financial Times, “The second bit of news is that the Genius (Guiding and Establishing National Innovation for US Stablecoins) act has made it through an important procedural vote in the Senate. Knowing that stablecoins are bank deposits, it is easy to see the act for what it is: a framework for light-touch regulation of a new kind of bank. Not a ‘narrow bank’, exactly (you can look up what that is) but a sort of ‘banking lite’. The central feature of the act as currently written is the requirement the deposits/stablecoins be backed 1:1 by one of the following reserve assets: US dollars, US central bank reserves, ‘demand deposits . . . at an insured depository institution’, ‘Treasury bills, notes, or bonds with a remaining maturity of 93 days or less’, Treasury bill repo or reverse repo agreements, or shares in money market funds that invest only in the other permitted assets.” [Robert Armstrong in the Financial Times, 2025-05-27]

NOTE: With that structure, stablecoin issuer profits are protected from competing on interest rates, and therefore guaranteed profits. Furthermore, as those profits are would be capped at \(i\), the interest rate a stablecoin issuer would receive on its holdings, stablecoin issuers’ profits would be positively correlated with interest rates. Given Republicans’ preferred policy of deficit-exploding tax cuts for the rich would be expected to increase interest rates, this legislation would be expected to increase the profits of stablecoin issuers.

Interestingly, there is some parallel to Glass-Steagall’s Regulation Q, which, aiming to stop banks taking risks to compete on interest rates, allowed the Fed to set a cap. It can be argued that this contributed to the savings and loan crisis, as S&Ls–not subject to Regulation Q–could attack deposits by offering higher interest rates.

Outlook: Hysteresis Effects

While it is unlikely that this ruling will mark the end of Trump’s tariffs, even if it does, it is important to note what economists call hysteresis effects: the idea that the effects of a shock can persist beyond its existence. In other words, things that are broken don’t just fix themselves.

[Bureau of Economic Analysis,

[Bureau of Economic Analysis,  [Cavallo, Llamas, and Vazquez,

[Cavallo, Llamas, and Vazquez,  [Bloomberg,

[Bloomberg,  [Financial Times,

[Financial Times,