The data reveals significant disruptions across multiple sectors: major ports are operating at 50% below normal capacity, recent graduate unemployment has hit historic highs, and American exports have collapsed—with vehicle exports to Canada dropping to just 16-20% of 2024 levels. Car prices are rising through “stealth” increases via reduced incentives and higher fees, while skilled worker shortages are driving up labor costs, with companies like Xcel Energy seeing 50% increases over five years. The oil sector is contracting sharply, with American rigs shutting down since tariffs were implemented, and international tourism revenue is projected to decline by $12.5 billion as multiple countries warn their citizens about traveling to the US.

The financial stability picture is equally concerning, with growing risks from crypto exposure in traditional companies and evidence that private credit returns have been systematically overstated by managers compared to independent data. Perhaps most telling is the emerging capital flight from US markets, evidenced by persistent arbitrage opportunities in Hong Kong that suggest growing reluctance to hold US assets. Meanwhile, Brazil is actively diversifying away from American financial markets toward Europe and China. The immigration enforcement spending in H.R. 1, while officially scored at $168 billion, likely represents nearly $1 trillion in hidden costs when properly accounting for the economic contribution of deported immigrants and realistic spending timelines.

Weakening Economy

Port Of Lost Angales Executive Director: June Traffic And Hiring Were Roughly 50 Percent Below Normal Levels. According to Erika D. Smith in Bloomberg, “On a normal day in June, about a dozen ships, most newly arrived from Asia, would be docked at the Port of Los Angeles. Workers would be busy unloading cargo, directing the containers to trucks, trains and planes bound for businesses and warehouses across the US. But no day has been normal since the start of President Donald Trump’s roller coaster of a trade war. ‘You”re seeing what’s been noticeable to us over the last several weeks,’ said Gene Seroka, executive director of the Port of Los Angeles, on Wednesday, nodding toward the sprawling San Pedro Bay and the equally struggling Port of Long Beach in the distance. ‘During the past seven days, we”ve averaged about five ships. Job orders for our dock workers … are down nearly 50%.’” [Erika D. Smith in Bloomberg, 2025-06-07]

2022: Direct Economic Activity From The Port Of Long Beach Was More Than One Percent Of GDP, With 20 Percent Of Southern California Jobs Tided To The Ports. According to Erika D. Smith in Bloomberg, “But the port city that’s perhaps in the most precarious position is Long Beach. Along with Los Angeles, it operates the largest port complex in the US and the busiest in the Western Hemisphere. About 60% of the trade that comes to the port is directly with China. The acres of cranes and shipping containers, impossible to miss just west of Long Beach’s downtown, serve as the hub of an industry that contributed some $300 billion in direct economic output and $93 billion in tax revenue to Los Angeles County in 2022, according to a recent economic development report. Across Southern California, 1 out of every 5 jobs is tied to the ports, including the broader supply chain of warehouse workers and truck drivers. And more than 70% of the longshore workers employed at one of the ports live within a 10-mile radius.” [Erika D. Smith in Bloomberg, 2025-06-07]

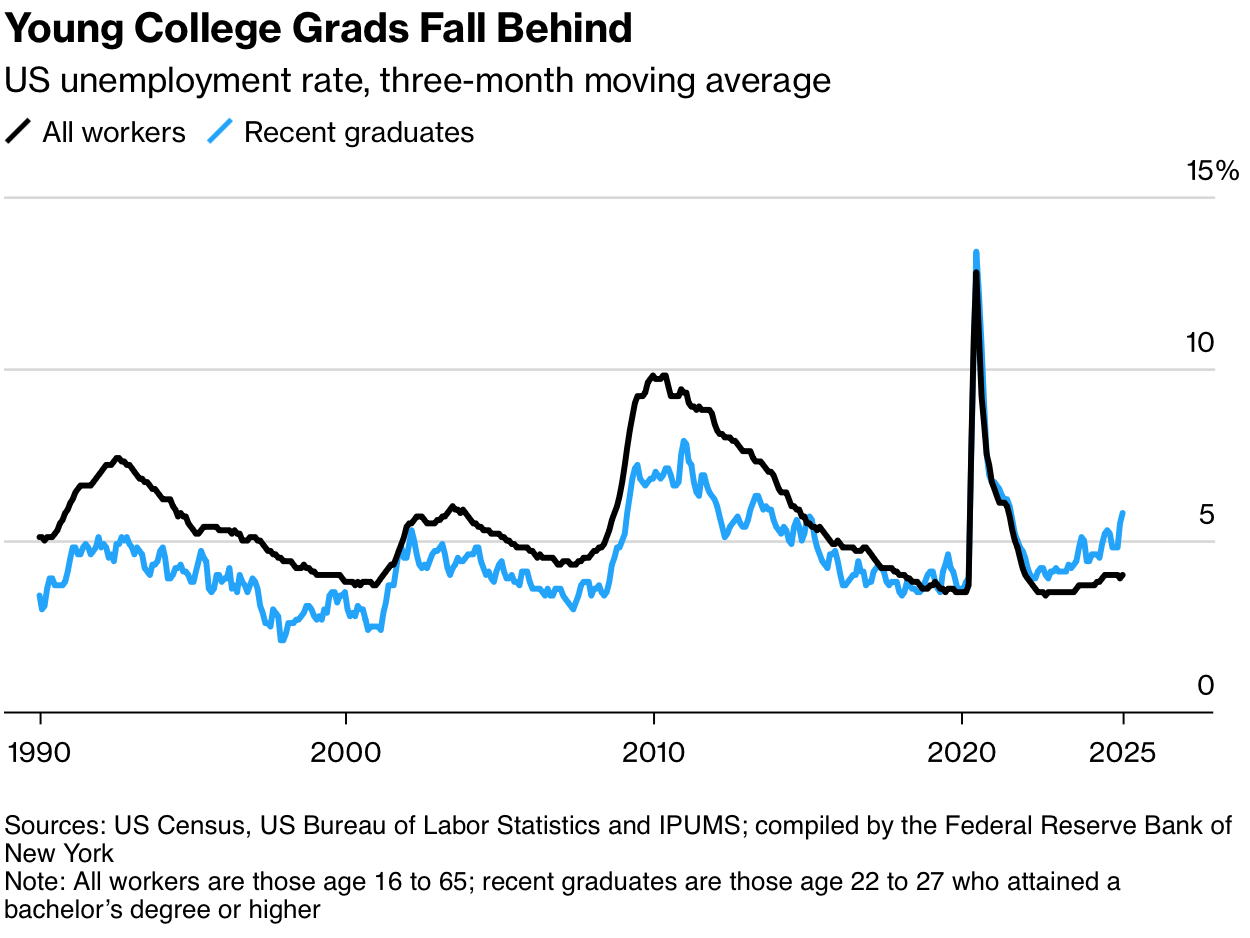

Labor Market Weakness

March 2025: The Unemployment Rate For Recent Graduates Was Higher By The Aggregate Unemployment Rate By The Most Since At Least 1990. [Bloomberg, 2025-06-09]

Higher Prices

Although Sticker Prices Have Yet To Rise, Car Makers And Sellers Have Been Reducing Other Incentives. According to Bloomberg, “Car buyers racing to get ahead of President Donald Trump’s tariffs face an uncomfortable truth — the trade war is already boosting US auto prices, often in ways nearly invisible to consumers. The sticker price on a particular make and model may not have changed, at least not yet. But automakers have been quietly cutting rebates and limiting cheap financing deals, adding hundreds of dollars to buyers” monthly payments even as the companies say they”re holding the line on pricing. Several have boosted delivery charges — a fee everyone must pay when buying a new vehicle — by $40 to $400 dollars, according to automotive researcher Edmunds.com Inc. Some dealers, meanwhile, have decided to charge more for the cars already on their lots, knowing it will cost more to replace them.” [Bloomberg, 2025-06-06]

April 2025: New Car Prices Increased By The Most In Five Years. “On The Consumer Side, They’re Seeing Several Thousand Dollars Of Actual-Experience Price Increase.” According to Bloomberg, “But the auto industry’s subtle price hikes are already having an effect. The average sale price for a new car jumped 2.5% in April, the steepest monthly increase in five years, according to the Kelley Blue Book car buying guide. The average reached $48,699, almost a record. Incentives, which once knocked 10% off the price, fell to 6.7%. Zero-percent financing deals — a key come-on in this age of high interest rates — dropped in April to their lowest rate since 2019, according to researcher Cox Automotive. And at some point, car buyers may balk. ‘On the consumer side, they”re seeing several thousand dollars of actual-experience price increase, whereas the factory is saying, “No man, we didn’t raise prices at all,”’ said Morris Smith III, a Ford dealer in Kansas. ‘Stealth is a good word for it.’” [Bloomberg, 2025-06-06]

By June 2025: Most Of The Inventory Of Pre-Tariff Cars On Dealer Lots Has Been Projected To Be Exhausted. According to Bloomberg, “All of these changes — the sticker price increases, reduced incentives and higher fees — will become more visible to car shoppers in the coming weeks. Since the 25% levies went into effect on April 3, dealers have been selling from a shrinking stockpile of pre-tariff cars. (There’s an exemption for cars that comply with the terms of the US, Mexico and Canada free trade agreement, which only face an import tax on their non-American content.) That process is nearly done, and by late June, dealers will face the new reality of lots filled with cars that cost more to bring into the country.” [Bloomberg, 2025-06-06]

Restricting Immigration

Unable To Fill New Engineering Roles, Xcel Energy Has Seen Its Labor Costs Outpace Inflation Over The Last Five Years. According to Bloomberg, “The US is already unable to fill about a third of its more than 400,000 new engineer roles created each year. The UK will see 20% of its engineers retire by 2030 — leaving a shortfall of 1 million jobs. Japan will see a deficit of 700,000 in that period. These can have big impacts on the economy. In Britain, the shortage of engineers could wipe 5% from its gross domestic product, according to the think tank Stonehaven. In the US, the lack of skilled workers will hold back President Donald Trump’s attempts to increase manufacturing, even if the tariff regime stabilizes and businesses get ready to invest. Trump’s attacks on US universities” international students, who tend to study engineering in a greater proportion than domestic students, will likely further sap the supply of skilled workers. When it doesn’t bankrupt a company or halt a project, skilled worker shortages lead to higher costs and longer timelines to build much-needed infrastructure, such as electricity grids. This is a problem for the US and Europe, which are seeing a surge in demand for power thanks to electric cars, heat pumps and massive data centers. The US utility Xcel Energy Inc. estimates its labor costs have risen 50% in the past five years, outpacing inflation.” [Bloomberg, 2025-06-04]

New Workers Can Only Be Born Or Imported, So A Decline In Birthrates And Immigration Restrictions Are A Hostile Combination. According to Bloomberg, “A shortage of skilled workers, especially engineers, is a growing problem in developed countries. How do you get more labor? ‘You either birth them or you import them,’ says Zeke Hernandez, professor at the Wharton School of the University of Pennsylvania. ‘But in an environment of declining birth rates, increasing retirements and now a restrictive immigration regime, shortages become quite severe.’” [Bloomberg, 2025-06-04]

Weaker Exports

April 2025: American Exports Of Passanger Vehicles To Canada Dropped To Between 16 And 20 Percent Of Their 2024 Average. According to Jason Miller, “Within the April trade data, we can begin to see many of the negative effects of tariffs. One example that affects the great state of Michigan where I live: the collapse in passenger vehicle exports (HTS 8703) with Michigan as a state of origin that were exported to Canada. One chart. Thoughts: For 2024, exports swung between $250 and $350 million each month. That is somewhere to the tune of 10,000 - 20,000 cars a month (ballpark estimate). As can be seen, April saw export plunge to $50 million, or roughly 1/5th to 1/6th of the average month in 2024. When you look at the last Economic Census and consider the average plant for one of the four largest assemblers shipped $6.7 billion a year (https://lnkd.in/g94ur9J2), it becomes clear that the $3.5 billion in exports to Canada in 2024 supports about 1/2 the demand of an entire plant. As the average plant of the four largest assemblers employs 3,800 people, that represents a lot of jobs. Implication: large US manufacturers don’t just import, they also export. Hopefully, the collapse of Michigan’s exports of finished passenger vehicles to Canada in April reverses itself, as many jobs are at on the line in Michigan and elsewhere in the Great Lakes region.” [Jason Miller, 2025-06-07]

World Travel & Tourism Council: Trump’s Policies, Fully Implemented, Would Cut Tourism Income To The United States By $12.5 Billion. According to Bloomberg, “US President Donald Trump’s ‘America First’ policies have cut into travel worldwide. The simmering trade war, the crackdown at the border and the rollback of LGBTQ rights—capped by a ban on visitors from a dozen countries announced on June 4—have led to tens of thousands of canceled trips. With travelers choosing alternate destinations, the American economy will lose out on $12.5 billion this year, according to the World Travel & Tourism Council—which will widen the trade deficit, because economists count spending by visitors to the country as an export.” [Bloomberg, 2025-06-07]

June 2025: At Least 12 Countries Had Warned Their Citizens About Traveling To The United States. According to Bloomberg, “At least a dozen countries have advised their citizens to exercise caution on visits to the US. Canadians, for instance, have been told to prepare for delays, denial of entry and seizure of their devices. European countries including the UK, Germany and France have cautioned that travelers to the US risk detention by immigration officials. In March a backpacker from Wales was detained at the US border coming from Canada for almost three weeks, and a German tattoo artist was held for a month and a half when she tried to enter the US from Mexico. Ireland, Denmark and the Netherlands have warned transgender and nonbinary citizens of potential complications because of a Trump executive order recognizing only two sexes.” [Bloomberg, 2025-06-07]

Oil Market

Code

# Set up custom plot themeinclude("../scripts/oxocarbon-plot.jl")theme(:oxocarbon)# Include necessary packagesusingCSV, DataFrames, Dates# Load the csvraw =DataFrame(CSV.File("../resources/2025-06-09/Baker-Hughes.csv"))# Make a date columnraw.date =Date.(raw.Year, raw.Month, Ref(1))# Group raw by date and sum that valuerigs_groups =groupby(raw, :date)# Calculate rig counts by monthcounts = [sum(group.Count) for group in rigs_groups]months = [group.date[1] for group in rigs_groups]# Create a new dataframedf =DataFrame(; date = months, count = counts )# Create the plotplot(df.date[(end-18):end], df.count[(end-18):end]; xlabel="Month", ylabel="Baker-Hughes Rig Count", linewidth=2, title="Since Trump's Tariffs, American Rigs Have Shut Down", label="",)vline!([Date(2025,4,2)], label="Tariffs", linestyle=:dash, linewidth=2)

Crypto Infecting The Rest of The Financial Ecosystem

Standard Chartered: Roughly Public Companies Have Elected To Put Substaintial Portions Of Their Balance Sheets In Crypto. According to the Wall Street Journal, “Buying bitcoin is becoming a fad for a growing list of companies that have nothing to do with crypto but believe digital assets can boost their stocks. The problem, some industry insiders say: This could expose crypto to new risks, amplifying selloffs in moments of turbulence. The approach has been pioneered by executives such as bitcoin evangelist Michael Saylor, who has turned his software company Strategy into a warehouse for the digital currency. Other companies are following suit. About 60 companies with no previous ties to the market are now pursuing the ‘bitcoin treasury strategy,’ according to Standard Chartered Bank, citing data from BitcoinTreasuries.net. They make software, and offer marketing and healthcare services. Some aren’t just buying bitcoin, but are piling into smaller tokens such as ether, solana and XRP.” [Wall Street Journal, 2025-06-09]

Standard Chartered: Roughly 30 Of Those Companies Would Be Underwater On Their Holdings In The Event Of 15 Percent Fall In Bitcoin Value. According to the Wall Street Journal, “Their timing matters. The recently converted are likely to buy bitcoin and other tokens at much higher prices than earlier adopters such as Strategy. For instance, if bitcoin were to fall below $90,000 (just 15% below its current price of $106,000), the crypto holdings of some 30 public companies would be underwater, according to Geoff Kendrick, global head of digital assets research at Standard Chartered Bank.” [Wall Street Journal, 2025-06-09]

Context: Crypto Holdings and Debt Covenants

Under current accounting laws, a mark to market decline in crypto values should be counted as a loss on a company’s balance financial statement. Taking accounting losses is generally not free for businesses, and with such a volatile underlying asset, crypto crashes could accelerate financial difficulty for the companies that have made holding it a significant part of their financial identity.

Private Credit

CovenantLite: FOIA-Sourced Private Credit Returns Were Well Below Those Provided By Managers. According to CovenantLite, “Private credit has a data problem. More precisely, it has a performance data problem. In a market that increasingly prides itself on being institutional and transparent, most investors still rely on a dataset that’s built—at least partially—on what managers choose to show. If you’ve ever thought, ‘These returns feel a little high relative to what I’m realizing in my portfolio,’ you”re not wrong. The numbers are real—but the selection behind them isn’t neutral. This article digs into a quiet but important flaw in the way private credit performance gets reported. Using Preqin data, I separated fund returns by how the data was sourced: through Freedom of Information Act (‘FOIA’) requests versus directly submitted by managers. The results make one thing clear: IRRs directly submitted by managers are higher than those sourced via FOIA requests—in many cases, A LOT higher. And this is distorting investors” understanding of risk and return in private credit.” [CovenantLite, 2025-06-08]

1983-2019: Funds That Reported Their Data Outperformed Fund Data Sourced From FOIA Requests By 330 Basis Points. According to CovenantLite, “To test how much survivorship bias was affecting returns, I pulled all available private debt fund returns from Preqin, using the most recent “as of” data for each fund. This initial scrape gave me a universe of 1,815 funds with vintages ranging from 1983 to 2025. To reduce noise and focus on performance that had sufficient time to mature, I filtered down to funds with vintages through 2019. This conservative cutoff helps avoid overstating (or understating) IRRs from younger funds still in ramp-up mode. Next, I excluded strategies that seemed out of place for a private credit-focused analysis—such as Buyout (likely private equity mislabeled), Infrastructure, Growth, Fund of Funds, and a few others. After this cleaning process, I was left with a curated list of 1,175 funds that represent a broad but focused view of the private credit landscape. From there, I used Preqin’s source tagging to distinguish between FOIA-sourced data and manager-submitted data—allowing a direct comparison of performance based on how the information was obtained. Roughly 55% of the funds were sourced via FOIA, while 45% came from manager submissions. The punchline? The manager-submitted funds reported an average net IRR of 12.6%, while FOIA-sourced funds came in at 9.2%—a +3.3% spread that’s too big to ignore.” [CovenantLite, 2025-06-08]

Capital Flight

A Newfound Nervousness To Hold The US Dollar Could Be Behind The Collapse Of Interest Rates In Hong Kong. According to Robin Harding in the Financial Times, “For the past month or more, overnight interest rates in Hong Kong have been stuck just above zero per cent. Since everyone got used to ultra-low interest rates during the last couple of decades, it may not be immediately obvious how bizarre, unexpected and potentially alarming that situation is — or how it illustrates everything from the dwindling appetite of Asian investors for US assets, to a modest revival of Hong Kong’s capital markets, to surprising limits on the risk-taking capacity of banks and hedge funds. Donald Trump’s gyrations on trade policy have not broken global financial markets just yet — but what is happening in Hong Kong shows they are feeling the strain. The reason zero interest rates in Hong Kong are so odd is because its currency is pegged to the US dollar. That offers what seems like an easy arbitrage: borrow in Hong Kong at zero per cent, convert to dollars and earn US interest rates of more than 4 per cent. For an arbitrage, that is a large return, and since the currency is pegged the risk should be minimal. Yet for more than a month this divergence has continued. Every evening at seven o’clock the Hong Kong Monetary Authority announces the overnight rate. On Friday it stood, again, at 0.01 per cent. […] More concerning, however, the persistence of the arbitrage suggests limits on the market’s capacity to exploit it. The Taiwan dollar was not the first trade to blow up this year: a variety of so-called swap basis trades went wrong in April, at the time of Trump’s so-called “liberation day”, and with the US president’s gone-today-here-tomorrow approach to tariffs, currency volatility is high in general and risk managers have their traders on tight limits. The structure of modern hedge funds, with many small “pods” of traders and centralised risk controls, can exacerbate any move to cut exposures. That suggests markets have a limited capacity to absorb shocks at a time when they are being subjected to many of them. It raises the risk of sharp, correlated movements in financial assets in response to news — or even just rumour — about trade negotiations. It also hints at something more profound: the desire to hold Hong Kong dollars and other Asian currencies reflects a growing nervousness about US financial markets. It is, for now, nothing more than nervousness — a reluctance to put new money to work — but after decades of insatiable appetite for US financial assets, even that much is noteworthy.” [Robin Harding in the Financial Times, 2025-06-08]

Increased Appeal Of Other Markets

Amid Trump’s Tariffs, Brazil Has Announced That It Will Aim To Borrow More In Europe And China, And Less In American Financial Markets. According to the Financial Times, “Brazil is hoping to sell its first sovereign debt in the Chinese market as soon as this year, as President Luiz Inácio Lula da Silva looks to strengthen trade and investment ties with the Asian superpower. The leftwing administration in Brasília is planning the so-called panda bond — debt issued in Chinese renminbi by a foreign borrower — and is also keen to re-enter the euro-denominated bond market, according to deputy finance minister Dario Durigan. ‘The idea is that this year we”ll do both a new dollar issuance of a sustainable bond, like we did last year, as well as in Europe, and panda bonds in China,’ he told the Financial Times in an interview. ‘The European Union wants to negotiate with Brazil to expand our bilateral trade, whether in terms of transactions or also by offering Brazil the option of issuing its bonds in Europe,’ Durigan added. ‘The same thing can happen with China.’ The Lula government has been trying to deepen commercial ties with Brussels and consolidate links with Beijing, amid the global trade war sparked by US President Donald Trump’s sweeping tariffs.” [Financial Times, 2025-06-08]

New Debt Flooding In

Cato Institute: Congress’ Instructions To The CBO Obsured Almost $900 Billion In Costs Related To Immigration. According to David J. Bier for Cato, “The House of Representatives recently passed its budget reconciliation spending bill, the One Big Beautiful Bill Act (H.R. 1). The bill changes numerous aspects of tax and spending law, but its most significant spending increases are for immigration. The Congressional Budget Office (CBO) estimates the bill will direct an astounding $168 billion of the budget to immigration and border law enforcement, and there is even more for agencies that indirectly support immigration law enforcement. However, the CBO’s cost estimate is deficient in three ways. First, CBO assumes that all this increase is temporary, and second, it will happen gradually over the next 10 years, rather than in an immediate, reckless spending spree. Most importantly, it neglects the more significant cost of removing immigrants who would have paid more in taxes than they received in benefits. Properly considered, the actual cost of H.R. 1’s immigration enforcement spending is nearly $1 trillion more than the CBO estimates. When seen in the context of the overall costs of the bill, mass deportation would account for almost a quarter of the bill’s total price tag. Congress, not CBO, is primarily to blame for these flaws. The CBO must assess the immigration legislation at face value, and under its terms, the legislation provides only a one-time boost to spending. Moreover, CBO must score the bill in accordance with the instructions provided by Congress. Clearly, some members did not want to see an accurate score of mass deportation.” [David J. Bier for Cato, 2025-06-06]

The Combination Of H.R. 1’s Budget Gimmicks (Including Drastic Immigration Enforcement Spending Cuts After 2029), And The Trump Administration’s Ravenous Appetite For Immigration Enforcement, Mean The CBO’s Accounting Drastically Underestimates The Amount That Would Be Spent. According to David J. Bier for Cato, “Unlike normal fiscal year appropriations, H.R. 1 makes the funds available over a 5‑year period, and technically, the spending can stretch out over 10 years as long as it is “obligated” before 2029. The CBO assumes a business-as-usual spending pattern where the spending slowly ramps up and then slowly ramps down over 10 years. But this is based on CBO’s baseline spend-down patterns, which is absurd here. The Trump administration desperately wants to spend this money immediately. It is even plausible that they could blow through this money by next year and demand more from Congress. It is already stealing from other agencies and the military to do enforcement, and it is currently spending money for ICE appropriated for the end of the year. The bill appears to confirm this more aggressive timeline by mandating the hiring of 10,000 ICE agents for a cost of $8 billion—$800,000 per agent. It costs ICE about $200,000 in compensation per agent per year (p. 12), meaning that $8 billion is only enough to employ these agents for four years. The same math applies to CBP personnel. A more realistic position is that the Trump administration will use almost all this authority over the next four years. In this scenario, the government will spend nearly $80 billion annually on immigration enforcement in 2028. This is nearly half the amount all the states spend on local policing nationwide to improve public safety, and the $80 billion would be five times more than all other federal law enforcement combined. Nearly the same situation would occur in 2029 under the CBO’s assumptions when 78 percent of all federal law enforcement would be immigration. Either way, immigration enforcement would dwarf the rest of federal law enforcement. However, both scenarios assume that Congress will aggressively cut immigration enforcement after 2029. Budget analysts have questioned this assumption when it comes to tax cuts, but it is particularly egregious when it comes to immigration spending. Congress does not—and will not—cut immigration enforcement like this. H.R. 1 requires increased pay for all Border Patrol and ICE agents, hiring thousands of new agents, and new detention facility contracts. While the “wall” may be complete, the wall maintenance will likely be as much as half the cost of construction.” [David J. Bier for Cato, 2025-06-06]

Per Congressional Republicans’ Instructions, CBO Did Not Look At How Immigration Enforcement Spending Would Effect Immigration. With Reasonable Numbers, That Could Be More Than $800 Billion In Increased Deficits. According to David J. Bier for Cato, “The CBO does not directly estimate how all of this spending will affect immigrants. […] Combined with Trump’s policy changes that expedite removal for immigrants in the interior, we can reasonably expect that: Deportations would increase fivefold to over one million per year; Voluntary exits triggered by the deportations (both from families whose parent/spouse is gone as well as others fearful of what will happen) would increase proportionally to 500,000 per year; Illegal immigration and asylum seekers would not return to the trend from its currently historically low level; and Legal immigration would decline by at least 15 percent, due to deterrence and fewer people able to sponsor them. Altogether, over the five years when we expect the funding to be in effect, we can predict net immigration to fall by about 8 million, with an additional million lost in later years (again, keeping with Congress’ constructed reality that none of the increased spending will persist). Although it has not estimated how many people H.R. 1 will deport or the fiscal effects of those deportations, CBO has already estimated the fiscal effects of the 8.7 million increase in the number of illegal immigrants, asylum seekers, and parolees under the Biden administration. It found that this population will reduce the deficit by $897 billion over 10 years.” [David J. Bier for Cato, 2025-06-06]

David J. Bier: Lifetime Fiscal Costs Of Trump’s Proposed Mass Deportation Would Be Around $5 Trillion. According to David J. Bier for Cato, “Although CBO projections only account for costs over 10 years, I’ve previously extended this type of analysis to the lifetime of these immigrants. In that more comprehensive analysis, I found that the fiscal cost of mass deportation would be nearly $5 trillion. Whatever the time frame, immigrants are reducing the deficit and debt, so removing them will dramatically increase future debt. Hopefully, the Senate will recognize these costs and abandon the House’s flawed approach.” [David J. Bier for Cato, 2025-06-06]

[Bloomberg,

[Bloomberg,