May 2025: Sales Of New Homes Fell 13.7 Percent, Much More Than Expectations, Even As April Sales Data Were Revised Downwards. According to the Wall Street Journal, “Sales of new homes sank in May amid continued concerns over high mortgage costs. Here are the main takeaways from the Commerce Department report released Wednesday: —Sales of new single-family homes fell 13.7% to 623,000 from a downwardly revised 722,000 in April. –Sales had been expected to come in at 695,000, according to economists polled by The Wall Street Journal. –Monthly data on sales are volatile and tend to be revised. May’s data came with a 13.1% margin of error. –Compared with May 2024, sales declined 6.3%, the Commerce Department said.” [the Wall Street Journal, 2025-06-25]

Code

# Set up custom themeinclude("../scripts/oxocarbon-plot.jl")theme(:oxocarbon)# Load packagesusingFredData, DataFrames, Dates, StatsPlots# Set up Fredkey =ENV["FRED_API_KEY"]f=Fred(key)# Get the datastarts=get_data(f, "HOUST"; observation_start="2021-05-01", observation_end="2025-05-02",).datapermits=get_data(f, "PERMIT"; observation_start="2021-05-01", observation_end="2025-05-02",).data# Make the Plotplot(starts.date, starts.value; xlabel="Month", ylabel="Thousands Of Units", title="Weakest Housing Production In Four Years", linewidth=2, label="Units Started", )hline!([starts.value[end]]; linestyle=:dash, linewidth=2, label="" )plot!(permits.date, permits.value; linewidth=2, label="Units Permited", )hline!([permits.value[end]]; linestyle=:dash, linewidth=2, label="", color=:black )

Higher Prices

June 2025: Powell Said Tariff-Driven Inflation Was A Major Cause Of The Fed’s Inaction. According to Bloomberg, “Federal Reserve Chair Jerome Powell on Wednesday said the US central bank is still struggling to determine the impact of tariffs on consumer prices. ‘The question is, who’s going to pay for the tariffs?’ Powell said in response to a question during his testimony before the Senate Banking Committee. ‘How much of it does show up in inflation. And honestly, it’s very hard to predict that in advance.’ Powell’s second day of testimony on Capitol Hill this week comes after Fed officials left interest rates steady on June 18. Policymakers are facing even more pressure from President Donald Trump to lower borrowing costs in the wake of weaker-than-expected inflation readings. Two Fed governors, Christopher Waller and Michelle Bowman, have signaled they would be open to lowering rates as soon as July if inflation remains contained. But Powell on Tuesday repeated his message that officials need not rush to lower rates, citing the strong economy and uncertainty over how tariffs will affect inflation. Powell told the House Financial Services Committee that recent economic data is backward looking and many economists expect ‘a meaningful increase in inflation’ over the course of this year due to tariffs.” [Bloomberg, 2025-06-25]

Financial Instability

Autocallable ETF

June 2025: Calamos Announced The Planned Launch Of An Autocallables ETF, Approved By Trump’s SEC. [Calamos Investments, 2025-06-24]

Sellers Of Insurance Against Stock Market Crashes Risk Having Crashes Exacerbated. According to Matt Levine in Bloomberg, “There is a market for insurance against stock market crashes. Most investors are more or less long the stock market — they own diversified portfolios of stocks — and some of them worry that they will lose money if the stock market goes down. They would like to buy long-term black-swan-type insurance against a disastrous market crash. But who wants to sell that insurance? Well, Warren Buffett, occasionally. But in general, this sort of insurance is not that appealing for the seller: The trade is ‘you get paid a little bit each year when times are good, but you lose a ton of money when the stock market crashes.’ That’s the worst time to lose a ton of money! Also, if you are the buyer of that insurance, you might worry about credit risk: If you are buying insurance that pays off if the market crashes, how can you trust that the seller will pay you? Again, most investors are long the stock market, so if you buy crash insurance from some investor, and then the market crashes, she will probably have lost a ton of money herself and might be unable to pay you.” [Matt Levine in Bloomberg, 2025-06-24]

Marketing A Derivatives Transaction As A Yield Instrument, Autocallables Aggregate Retailers Into Selling Insurance On The Market. According to the Financial Times, “Autocallables — or structured products as they are known in Europe — are a typical of the funky vehicles that flourished in the low interest rate period that now looks like it is coming to and end. They are products mainly sold to retail investors as a yield-rich alternative to rock-bottom deposit rates. A typical structure involves offering to pay a 5 to 10 per cent yield as long some large benchmark equity index does not fall more than 40 per cent or rise more than 10 per cent. If the index falls 40 per cent, then the product changes from a yield product to an equity product, and you lose 40 per cent of your initial capital. If the index rises 10 per cent, the yield payments stop, and you get all of your capital back. […] The yield on an autocallable comes from the underlying dividend yield of index, and then the amount of premium that can be generated by selling puts. For simplicity, the higher the VIX (or local equivalent) the higher the yield that can be generated. I like to think of autocallables as a distributed portfolio insurance market. But what does that mean? When a trader wants to hedge their position, they often buy puts on the market. Historically, the other side of that trade would be a pension fund or some other long-term investor who would be willing to buy the market at that level, if it should fall, and liked collecting coupons in the meantime. However, sophisticated investors would want a hefty premium to bear the risk, so the cost of portfolio insurance was relatively high. Autocallables — and particularly Korean autocallables — changed the balance of the market. Retail investors would be buying a yield product, and typically rolled over the products as they expired, in effect constantly selling puts. This meant the balance of the market started to shift from sellers to buyers of insurance, and the price of hedging a portfolio fell substantially.” [the Financial Times, 2022-09-13]

Calamos’s ETF Would Index To A Levered Version Of The S&P 500, Meaning That Its Listed Payout Threshold Is Twice As High As It Functionally Is. According to Matt Levine in Bloomberg, “Here is a more detailed description. “Attractive high stable income derived from equity market parameters rather than credit risk or duration—providing a genuinely diversified income source,” etc. The product is slightly more complicated than what I have described: Instead of buying one autocallable, you buy a”52+ laddered autocallables, staggered weekly,” to smooth out your yield, though presumably if the market crashes most of them pay out. The description advertises recent yield of 14.7% on autocallables (higher than my 10% toy example). You lose money if the index falls by 40%, but the index is a levered version of the S&P 500 — roughly the S&P 500, but with a 35% volatility target — so really you are selling insurance on something closer to a 20% market crash. People want to buy that insurance, and now anyone can sell it.” [Matt Levine in Bloomberg, 2025-06-24]

Ramping Up Leverage

June 2025: Elizabeth Warren Warned Of The Danger Of The Trump Administration’s Proposed Leverage Requirements, Which Could Increase Leverage In Treasury Holdings. According to Bloomberg, “US Senator Elizabeth Warren criticized potential reforms to a key bank capital buffer ahead of regulators” meetings this week, saying the rule is a ‘critical safeguard’ that promotes financial stability. Officials are set to propose changes to what’s known as the enhanced supplementary leverage ratio, Bloomberg News reported earlier this month, after concerns that the bank capital rule constrained trading in the $29 trillion Treasuries market. ‘It would be irresponsible to slash the eSLR in any economic environment. It is especially reckless to do so given the numerous threats to the economy and the nation’s financial system,’ Warren wrote in a letter to Federal Reserve Vice Chair for Supervision Michelle Bowman, as well as acting chair of the Federal Deposit Insurance Corp. Travis Hill and Rodney Hood, the acting head of the Office of the Comptroller of the Currency. Warren said the economy already faces risks from President Donald Trump’s ‘chaotic tariff policies.’ In April, Trump’s tariffs rattled the markets, sharpening investors” focus on the standards. […] Warren said Treasuries are not completely free of risk and banks should not be permitted to finance those investments with unlimited leverage. ‘Banks” own actions, and a clear record of evidence, demonstrate that concerns over a strong eSLR are more related to big banks” ability to make payouts to shareholders and executives than their ability to act as a source of strength to the economy during periods of stress,’ the Massachusetts Democrat said.” [Bloomberg, 2025-06-24]

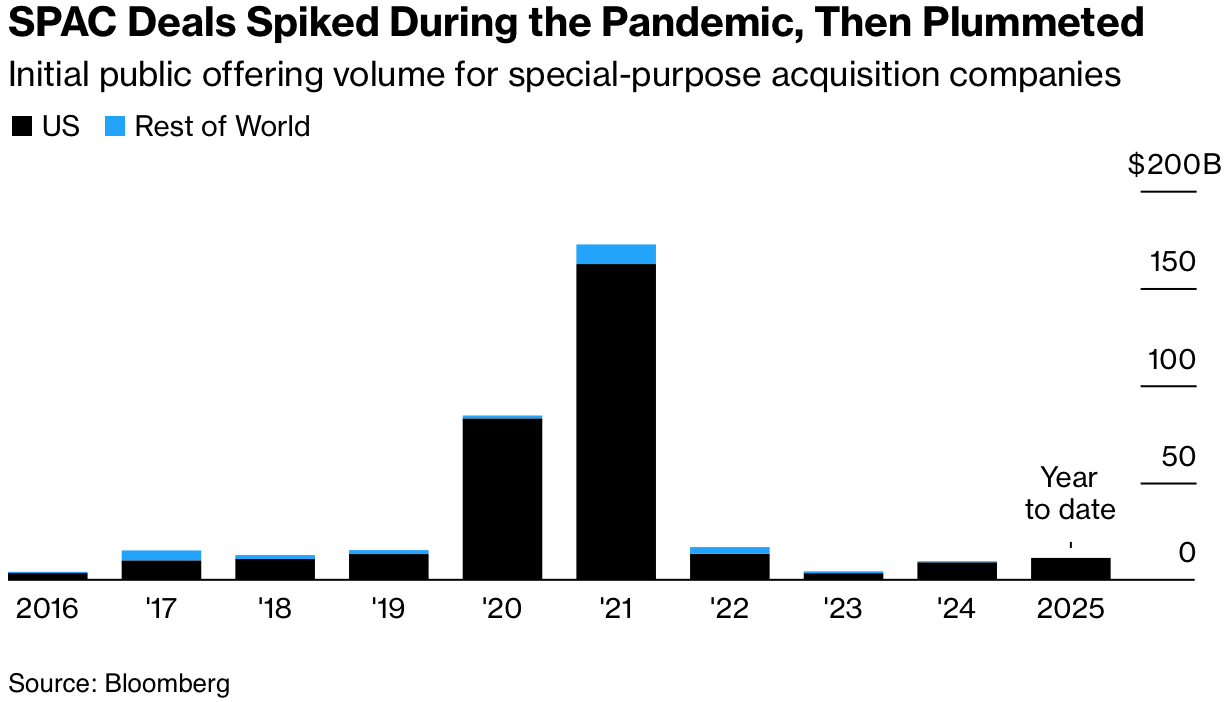

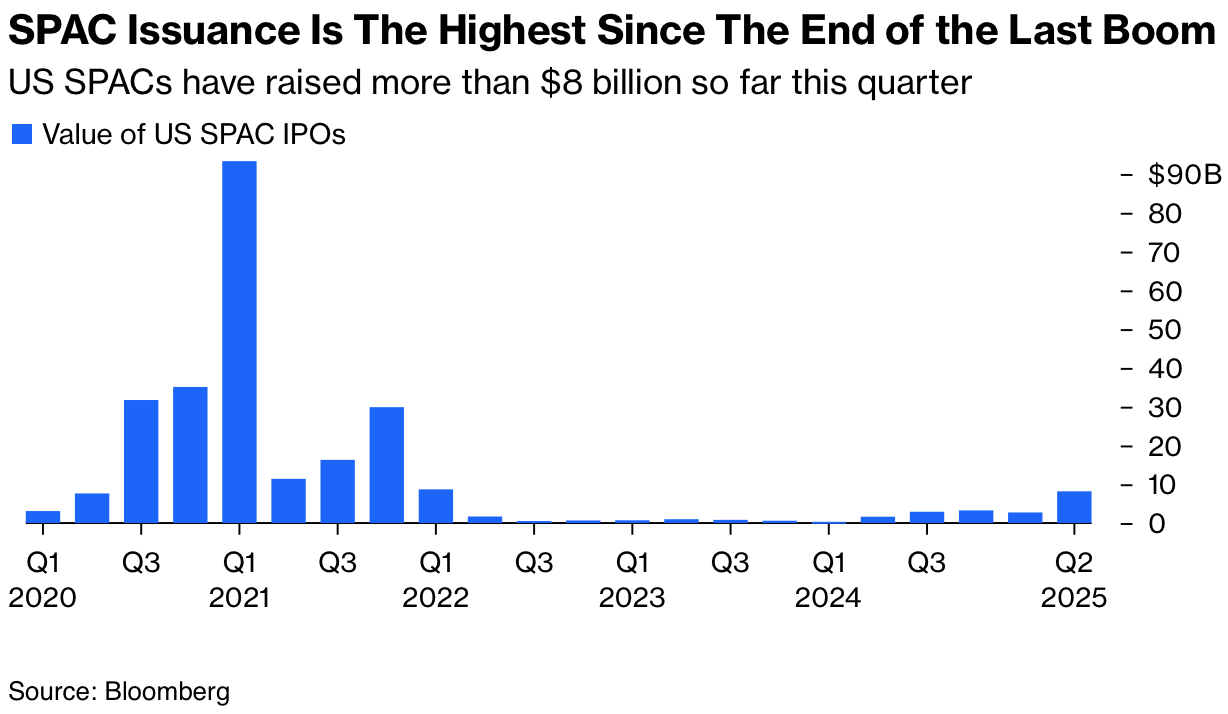

SPACs

2025: SPAC Activity Has Rebounded Slightly, Surpassing 2023 And 2024 Levels By June. [Bloomberg, 2025-06-17]

June 2025: After Regulatory Scrutiny Had Prompted A Self-Imposed Ban On SPAC Deals, Goldman Sachs Has Begun To Underwrite Those Deals Again. According to Bloomberg, “Goldman Sachs Group Inc. is wading back into the market for SPACs three years after stricter regulatory scrutiny prompted a self-imposed ban on handling so-called blank-check companies. The investment bank is once again open to underwriting new deals for special-purpose acquisition companies, according to people with knowledge of the matter. The firm will evaluate potential deals on a case-by-case basis and may limit the sponsors it works with, one of the people said, asking not to be identified discussing private matters. The decision marks a reversal from 2022, when the bank pulled out of working with most of the SPACs it took public and also stopped work on new US SPAC issuance. A SPAC typically works with its adviser even after going public to complete its merger with a target firm, known as the de-SPAC transaction. SPACs caught fire on Wall Street in the market mania following the pandemic. Blank-check companies drew financiers, politicians and celebrities with the promise of making millions off investors rushing into the vehicles. But that came to an abrupt end when markets soured, hammered by stricter regulations and the plunging stock of companies that went public by merging with blank-check firms.” [Bloomberg, 2025-06-17]

Participants Have Expressed The Expectations That The Trump Administration Would Roll Back Additional Regulations The Biden Administration Put In Place. According to Bloomberg, “When Goldman pulled out of most of its SPAC work in 2022, a spokesperson for the bank said it was in response to the evolving regulatory environment, adding that it could reverse course if the SEC guidelines were scaled back. The changes included exposing underwriters to greater liability risk in soured deals. Two years later, the Securities and Exchange Commission embraced the plan for tightening oversight of SPACs, forcing more disclosure and marking an effort to crack down on conflicts of interest. The rules were partly aimed at addressing concern that the listings were bypassing more stringent requirements on traditional IPOs and exposing retail investors to higher risk. The Trump administration is also expected to ease rules adopted under the Biden administration that it views as hindering capital formation.” [Bloomberg, 2025-06-17]

[Bloomberg,

[Bloomberg,  [Chris Bryant in Bloomberg,

[Chris Bryant in Bloomberg,