July 03, 2025

Data

Manufacturing Activity

ISM: Despite Accelerating Price Pressure, Manufacturing Activity Stayed Consistent With A Contraction In June 2025. According to Bloomberg, “US factory activity contracted in June for a fourth consecutive month as orders and employment shrank at a faster pace, extending the malaise in manufacturing. The Institute for Supply Management’s manufacturing index edged up 0.5 point last month to 49, according to data released Tuesday. Readings below 50 indicate contraction. A measure of prices paid for raw materials showed slightly faster inflation.” [Bloomberg, 2025-07-01]

June 2025: Price Pressure Reached Its Highest Level Since June 2022. According to Bloomberg, “Meanwhile, higher materials costs remain an issue for producers, the ISM survey indicated. The group’s price measure ticked up to 69.7, near the highest level since June 2022.” [Bloomberg, 2025-07-01]

June 2025: The Ratio Between ISM Survey Respondents Talking About Reducing Headcount Relative To Those Talking About Hiring Reached One Of Its Widest Levels On Record. According to Bloomberg, “For every comment on hiring, there were 3.2 on reducing head counts — one of the widest ratios since ISM began tracking employment comments — reflecting companies’ continuing focus on accelerating staff reductions due to uncertain near- to mid-term demand.” [Bloomberg, 2025-07-01]

Economic Degradation

Worse Information

July 2025: The Trump Administration Proposed Cutting Almsot A Fifth Of NOAA’s Staff. According to Bloomberg, “The National Oceanic and Atmospheric Administration is proposing cutting about 18% of its workforce and slashing $1.5 billion from its budget, including terminating programs to protect coastal communities and research that supports better forecasts and natural disaster prediction. At least 2,256 positions, out of 12,596 have been targeted for elimination, according to budget estimate released Monday. NOAA’s Oceanic and Atmospheric Research office, described as ‘the engine that drives the next-generation’ of science and technology, will be eliminated, with some of its functions going to other departments.” [Bloomberg, 2025-07-01]

Claiming AI Could Fill In The Gaps, The Trump Administration Has Pushed For Cuts To The Data And Researchers Involved In Building Climate And Weather Models. According to Bloomberg, “The budget comes amid President Donald Trump’s cuts to climate research and federal weather forecasting agencies, reductions that critics say will diminish the ability to predict weather and erode the quality of weather models as fewer observations are made. Commerce Secretary Howard Lutnick pushed back against some of these criticisms in a congressional hearing earlier this year, saying the agency will use automation and AI to cover the gaps.” [Bloomberg, 2025-07-01]

- Since 2007, Improvements In Forecasts Had Saved An Average Of $5 Billion Per Storm, Dramatically More Than NOAA’s Budget. According to Bloomberg, “A recent study showed forecast improvements since 2007 have saved the US economy $5 billion per storm that makes landfall, Franklin said. ‘That’s four times the annual National Weather Service budget and we had five landfalling US hurricanes last year.’ The cuts would not just affect climate change research, but also many aspects of long-term weather, Swain said. A number of high-profile labs, including the National Severe Storms Lab that was made famous by the movie Twister, would be impacted.” [Bloomberg, 2025-07-01]

Capital Flight

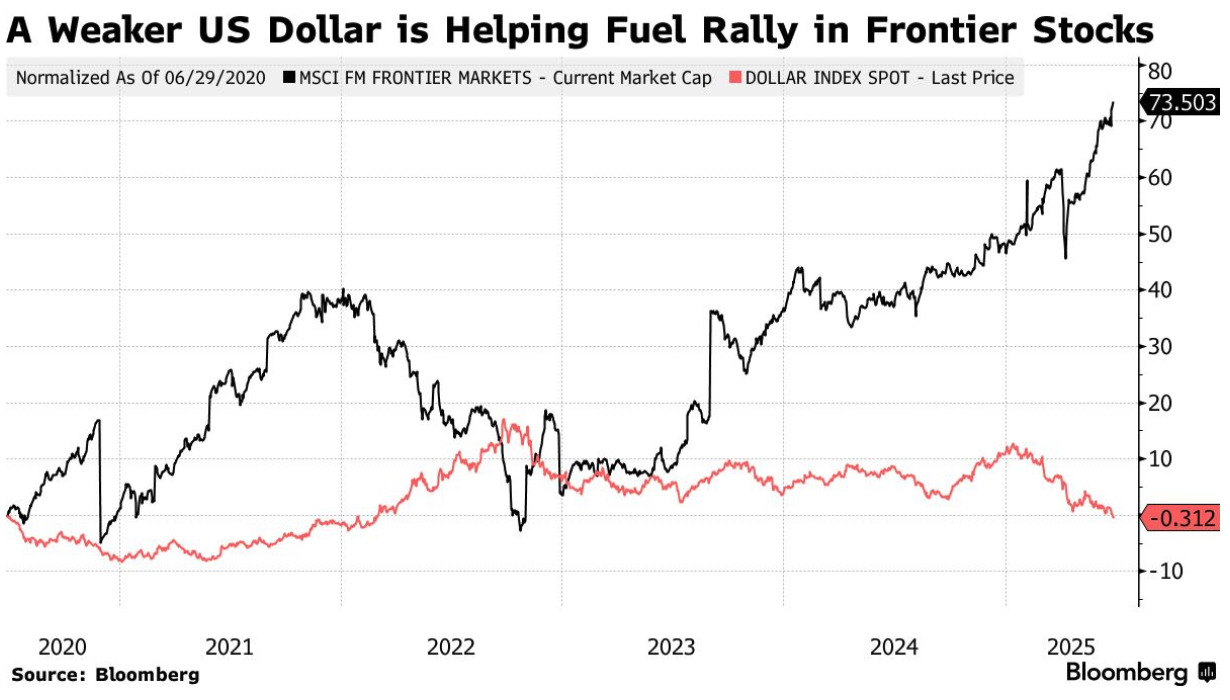

In The First Half Of 2025, MSCI’s Gauge Of The 25 Smallest And Less Liquid Equity Markets Saw Its Largest Rally Since 2007. According to Bloomberg, “Frontier-market stocks are poised for more gains after their strongest first half in 18 years, strategists said. MSCI Inc.’s gauge of 25 smaller and less liquid equity markets advanced 17% in the first six months of the year, its biggest rally for that period since 2007. The advance was underpinned by a weaker dollar, relative insulation from global risks and the reduced threat of an oil-price spike. Investors have pumped funds into frontier nations such as Vietnam and Morocco as they chase higher returns and options outside the US, where unpredictable trade policies and rising debt levels have spooked markets. The slump in the dollar, which is down about 9% for the year, has helped reduce import costs and support growth in developing economies. ‘Frontier markets are cheap,’ said Charlie Robertson, head of macro strategy at FIM Partners. ‘Many in Frontier are tariff-resistant, lovers of a weak dollar and getting a double-whammy benefit from lower oil prices cutting the import bill and inflation.’” [Bloomberg, 2025-07-02]

Financial Instability

Riskily-Named Bank

Trump-Aligned Billionaires Palmer Luckey, Joe Lonsdale, And Peter Thiel Have Put Money Into A Bank With The Goal Of Serving Startups And Crypto Businesses. According to the Financial Times, “A group of tech billionaires led by Palmer Luckey, co-founder of military contractor Anduril, is preparing to launch a US bank intended to fill the gap left by Silicon Valley Bank serving start-ups, including cryptocurrency businesses. To be named Erebor, the bank would be backed by high-profile tech investors including Joe Lonsdale, the founder of venture capital firm 8VC and a co-founder of Peter Thiel’s defence group Palantir, according to people familiar with the matter. Thiel’s venture capital fund, Founders Fund, would also be among the investors, according to two people close to the matter. Like Anduril and Palantir, Erebor’s name is a reference to JRR Tolkien’s The Lord of the Rings. Erebor is the ‘lonely mountain’ whose treasures are reclaimed from the dragon Smaug. Luckey and Lonsdale — who were big donors to Donald Trump in the 2024 US presidential election — want the bank to take over the niche once occupied by SVB as the go-to lender for riskier companies and cryptocurrency players that traditional banks might reject. Erebor has applied for a national bank charter in the US, a licence that allows a financial institution to operate as a bank.” [Financial Times, 2025-07-01]

The Bank, Whose Banking Charter Is Before The Trump Administration Would Be Named Erebor, After The Dwarven Stronghold Retaken In The Hobbit. According to the Financial Times, “A group of tech billionaires led by Palmer Luckey, co-founder of military contractor Anduril, is preparing to launch a US bank intended to fill the gap left by Silicon Valley Bank serving start-ups, including cryptocurrency businesses. To be named Erebor, the bank would be backed by high-profile tech investors including Joe Lonsdale, the founder of venture capital firm 8VC and a co-founder of Peter Thiel’s defence group Palantir, according to people familiar with the matter. Thiel’s venture capital fund, Founders Fund, would also be among the investors, according to two people close to the matter. Like Anduril and Palantir, Erebor’s name is a reference to JRR Tolkien’s The Lord of the Rings. Erebor is the ‘lonely mountain’ whose treasures are reclaimed from the dragon Smaug. Luckey and Lonsdale — who were big donors to Donald Trump in the 2024 US presidential election — want the bank to take over the niche once occupied by SVB as the go-to lender for riskier companies and cryptocurrency players that traditional banks might reject. Erebor has applied for a national bank charter in the US, a licence that allows a financial institution to operate as a bank.” [Financial Times, 2025-07-01]

In Addition To Targeting Clients In Startups And Cryptocurrency, It Would Also Look To Give Foreign Companies Access To The American Banking System. According to the Financial Times, “‘The bank will be a national bank . . . providing traditional banking products, as well as virtual currency-related products and services, for businesses and individuals,’ according to the application, made public this week. Its target market would be businesses that were part of the US ‘innovation economy’, in particular tech companies focused on virtual currencies, artificial intelligence, defence and manufacturing, the filing said. It would also serve individuals who work for or invest in these companies. It also planned to work with non-US companies ‘seeking access to the US banking system’.” [Financial Times, 2025-07-01]

Context: A Bad Name and Bad Strategy

Erebor is a Terrible name for a bank

Because the above section is way too long, and more important, this section will be as short as possible, but just as I believe that the name Palantir is a signal of its malevolent intentions, Erebor is a terrible name for a bank.

The timeline for Erebor is as follows: the Mountain, Erebor becomes a thriving location for dwarves, attracting the dragon Smaug, who kills most of the dwarves, and takes the treasure for himself. As a result, the economy that was built around Erebor dries up.

When a company of dwarves, led by Thorin, the grandson of the last king under the mountain, manages to retain control of Erebor, the consequences of Smaug’s long-holding of the treasure becomes apparent, as he infected it with Dragon-sickness, which makes anyone who holds the treasure extremely greedy. As a result, Thorin refused to cooperate with anyone else, including the men of Dale who were instrumental in defeating Smaug.

This dispute escalates into the battle of five armies, in which Thorin is killed.

After that, it served as the source of speculative expeditions to Moria, which ultimately created the false hope that led the fellowship there and to the death of Gandalf the grey. Not exactly the precedent that should be set in a bank aiming to serve other speculative ventures.

Trade War

Powell: Without Trump’s Tariffs, The Fed Probably Would Have Cut Interest Rates. According to Bloomberg, “Speaking Tuesday during a panel in Portugal, Fed Chair Jerome Powell repeated that the central bank probably would have cut rates further this year absent Trump’s expanded use of tariffs. Still, when asked if July was too soon for a rate cut, Powell didn’t rule out the possibility.” [Bloomberg, 2025-06-30]

Effect On Smaller Companies

JP Morgan: Almost Half Of Midsized Companies Import Goods Directly. According to Bloomberg, “Nearly half of these midsize companies — defined as those with between $10 million and $1 billion in annual revenue — import goods. New research from the JPMorganChase Institute breaks down the range of direct costs that they would face under the various tariff scenarios. ‘Since midsize firms have an outsize reliance on Chinese goods, making up 20.9% of their total 2022 goods imports, a rate of 55% still leads to substantial costs for some segments of the middle market,’ the JPMorganChase Institute report said.” [Bloomberg, 2025-07-02]