Around the edges, more and more parts of the Trump economy have started to break. After recovering from its massive drop in anticipation of Trump’s tariffs, labor market momentum is once again falling. Meanwhile, Amazon’s Prime day event is off to a slow start, as Tariffs have squeezed merchants out of being able to offer meaningful discounts. Meanwhile, the Trump administration continued its crackdown on construction that could increase the supply (and therefore reduce the price) of energy, with an executive order making the process of certifying that construction had started for the sake of tax purposes much harder. Apparently, this was traded for the votes of the Freedom Caucus.

In Trade war news, the Yale Budget Lab put together a write up of the Tariffs Trump has announced so far this month (excluding the 50 percent tariff on copper announced today), and in shocking news, the consequences will be bad for the country, and especially bad for the poorest Americans.

In one bright spot, Elise Stefanik’s vendetta against Harvard could derail the administration’s push to allow for Americans’ 401(k)s to bail out private Equity. By trying to get the SEC to look at the marks of Harvard’s private equity holdings, it could set a precedent that would be dangerous to an industry reliant on pricing itself.

2025: The First Four Hours Of Amazon’s Prime Day Event Saw Sales 14 Percent Lower Than In 2024. According to Bloomberg, “Amazon.com Inc.’s Prime Day sales fell almost 14% in the first four hours of the event compared with the start of last year’s sale, according to Momentum Commerce, which manages 50 brands in a variety of product categories.” [Bloomberg, 2025-07-08]

Due To Trump’s Tariffs, Some Merchants Decided Against Participating In The Promotions This Year. According to Bloomberg, “Before this year’s sale began, some sellers were planning to sit out the event in the wake of tariffs imposed by President Donald Trump that have pushed up prices for many products imported from China and elsewhere. Merchants and analysts alike are watching the sale closely for clues to the strength of the US economy as well as consumer sentiment.” [Bloomberg, 2025-07-08]

Gutting Investment

July 2025: Trump Signed An Executive Order More Strictly Defining When A Project Has Started, Making It Harder For Solar Installations To Get Building. According to Bloomberg, “On Monday evening, Trump issued an executive order directing the US Treasury Department to more strictly define when a project has started construction, including restricting the use of efforts to lock in tax credits unless a substantial portion has been built. The order could serve as an incremental negative for the entire solar sector, Phil Shen, an analyst for Roth Capital Partners, wrote in a report late Monday. ‘The risk is to the downside,’ Shen said. Under the tax-and-spending bill signed into law July 4, solar and wind developments are eligible for tax credits if they begin construction within 12 months. That provision had irked fiscal conservatives in the US House Freedom Caucus, who wanted to see an end to the incentives.” [Bloomberg, 2025-07-07]

Bloomberg: Reports Indicated Trump Made The Decision To Make It Harder To Build Factories In Exchange For The Freedom Caucus’ Votes For His BBB. According to Bloomberg, “The executive order comes after reports the Trump administration had struck a deal with the Freedom Caucus to more closely scrutinize the incentives in exchange for support for the budget package.” [Bloomberg, 2025-07-07]

Housing

Lennar: Incentives To Entice Buyers Rose To The Highest Level Since 2010. According to the Wall Street Journal, “Big home builders with financing arms such as D.R. Horton targeted young buyers by offering mortgage-rate buydowns that make monthly repayments more affordable. But these sweeteners are no longer working as well as they used to. Builder Lennar said it had to offer incentives equivalent to a 13.3% price discount in its second quarter to entice buyers—the highest rate since 2010. This is eating into builders’ profit margins.” [the Wall Street Journal, 2025-07-07]

Trade War

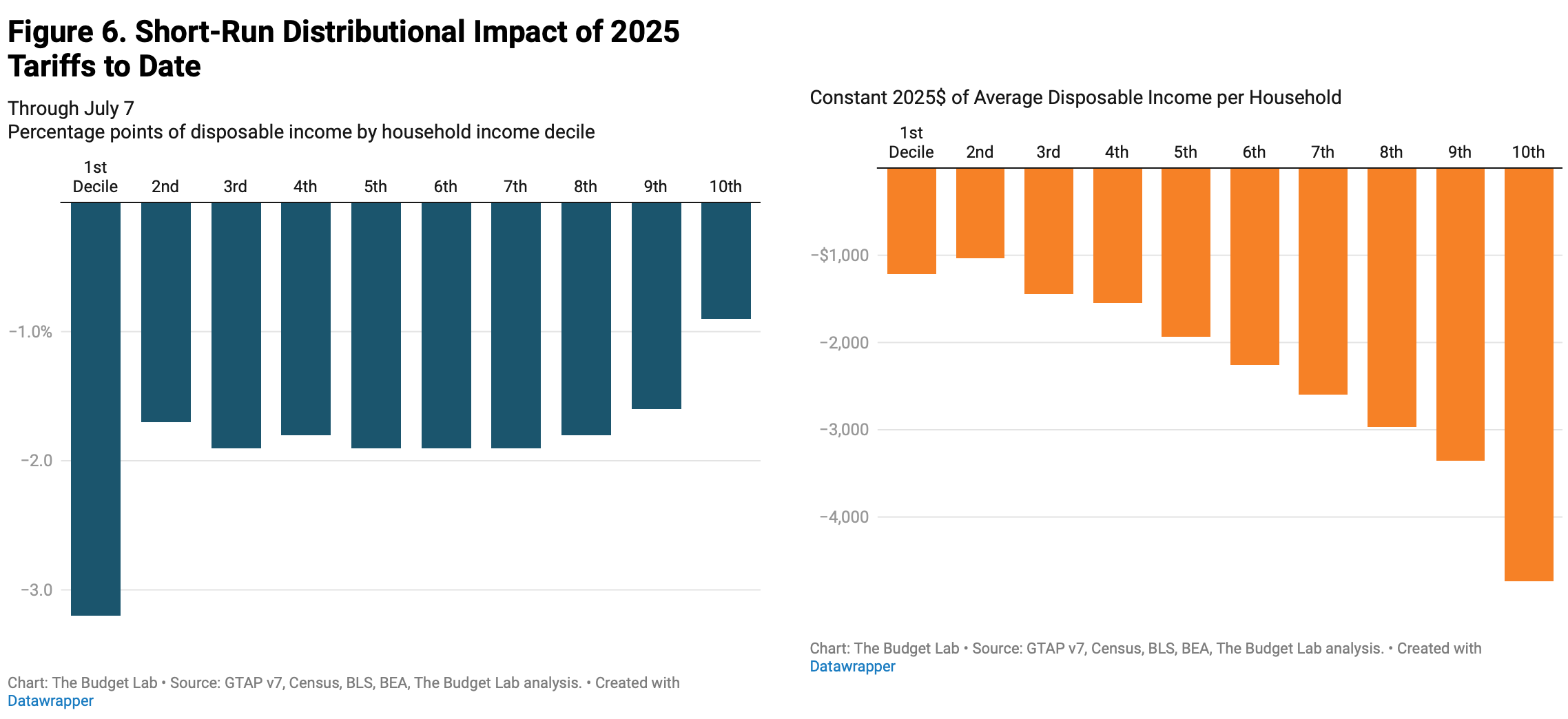

July 2025: After Incorporating Trump’s Latest Announced Tariffs, The Yale Budget Lab Found Tariffs For American Consumers Rose To Their Highest Levels Since The Great Depression. According to the Yale Budget Lab, “Consumers face an overall average effective tariff rate of 17.6%, the highest since 1934. After consumption shifts, the average tariff rate will be 16.5%, the highest since 1936.” [the Yale Budget Lab, 2025-07-07]

July 2025: Trump’s Tariffs Would Be Expected To Raise Prices By About To $2,300 Per Household. According to the Yale Budget Lab, “The price level from all 2025 tariffs rises by 1.7% in the short-run, the equivalent of an average per household income loss of $2,300 in 2025$. This assumes the Federal Reserve does not react to tariffs and so the real income adjustment comes primarily through prices rather than nominal incomes; if the Federal Reserve reacted, the adjustment could in part come in the form of lower nominal incomes. Annual pre-substitution losses for households at the bottom of the income distribution are $1,200. The post-substitution price increase settles at 1.5%, a $1,900 loss per household.” [the Yale Budget Lab, 2025-07-07]

Yale Budget Lab: Trump’s July Tariffs Would Likely Lead To A Short-Run Increase In Consumer Prices Of 1.7 Percent, Barring A Fed Reaction. According to the Yale Budget Lab, “The 2025 tariffs imply an increase in consumer prices of 1.7% in the short-run, assuming no policy reaction from the Federal Reserve and full passthrough of tariffs to consumers. As a result, TBL assumes the real income adjustment comes primarily through prices rather than nominal incomes. If the Federal Reserve reacted, the adjustment could in part come in the form of lower nominal incomes. This is a pre-substitution number that captures consumer welfare effects. It is the equivalent of a short-run income loss3 of $2,300 per household on average in 2025 dollars. The post-substitution price increase settles at 1.5%, a $1,900 short-run loss per household.” [the Yale Budget Lab, 2025-07-07]

NOTE: Evidence Exists To Suggest The Fed Has Reacted

July 2025: Powell Said That The Fed Likely Would Have Cut Without Trump’s Tariffs. According to CNBC, “Federal Reserve Chair Jerome Powell said Tuesday that the U.S. central bank would have eased monetary policy by now if not for President Donald Trump’s tariff plan. When asked during a panel if the Fed would have lowered rates again this year had Trump not announced his controversial plan to impose higher levies on imported goods earlier this year, Powell said, ‘I think that’s right.’ ‘In effect, we went on hold when we saw the size of the tariffs and essentially all inflation forecasts for the United States went up materially as a consequence of the tariffs,’ Powell said at European Central Bank forum in Sintra, Portugal.” [CNBC, 2025-07-01]

Regressive Redistribution

Yale Budget Lab: The Cost Of Trump’s Tariffs To The Lowest Decile Of Households Will Be 3.5 Times Larger Than To The Top Decile. According to the Yale Budget Lab, “Tariffs are a regressive tax, especially in the short-run. This means that tariffs burden households at the bottom of the income ladder more than those at the top as a share of income. The regressivity is about the same when looking at all 2025 tariffs: the short-run burden on the 1st decile is more than 3x that of the top decile (-3.2% versus -0.9%). The average annual cost to households in the 1st and top decile rise to $1,200 and $4,700 respectively in 2025$. The median cost is $2,100 per household.” [the Yale Budget Lab, 2025-07-07]

Capital Flight

Currency Traders Have Struggled With The Capital Flight Caused By Trump’s Trade War, Citing Its Unprecedented Nature. According to Bloomberg, “Some of Wall Street’s tried-and-true currency strategies aren’t working anymore, and it’s baffling even the most seasoned traders. Before President Donald Trump’s policies sent the dollar plunging, investors could reliably use a number of indicators to figure out how to trade. Europe cuts interest rates? Sell euros. Markets look jittery? Buy dollars. Oil prices spike? Time to snap up currencies from commodity exporters. But now, those signals are misfiring more frequently. Traders at UBS Group AG and Mizuho International Plc, say the models they used to count on getting it right are instead getting it wrong. And the new forces driving currency markets, like the broad shift of money out of the US and foreign investors buying dollar hedges, are hard to track because the data is sparse, making it tough for professionals to adjust their systems. As a result, they’re running smaller and simpler trades.” [Bloomberg, 2025-07-07]

Despite European Interest Rates Being Between 225 And 250 Basis Points Lower Than Those In The U.S., The Euro Has Appreciated 13 Percent Against The Dollar. According to Bloomberg, “Take the dollar and euro. In June, the European Central Bank cut borrowing costs for the eighth time in this cycle, bringing the deposit rate to 2%. While in the US, the Federal Reserve last chose to hold in a range of 4.25% to 4.5%. All else being equal, that would argue for a strong dollar and weak euro. The opposite has happened, with the euro surging 13% this year to a four-year high.” [Bloomberg, 2025-07-07]

Private Markets

Potential Good Policy Outcome?

July 2025: Rep Stefanik Asked The SEC To Look At The Valuations Of Harvard’s Private Equity Investments. According to the Wall Street Journal, “Rep. Elise Stefanik (R., N.Y.) recently sought an investigation into Harvard’s financial disclosures to bondholders. She might as well have fired a bazooka at the entire private-equity industry. In a letter to Securities and Exchange Commission Chairman Paul Atkins, the Republican congresswoman said the university’s finances might be more precarious than publicly acknowledged. Much of its $53 billion endowment is invested in private-equity funds that ‘are often overvalued due to reliance on internal estimates and outdated transaction data,’ she said. The letter added that ‘the real, realizable value of these assets is likely far below stated values,’ because of higher interest rates and declining private-market valuations. She might be right. But Harvard doesn’t generate those valuations itself. It gets them from the external managers at the funds where it invests. So if the SEC investigates Harvard over the valuations, it should also investigate the private-equity firms that provide them, if not the whole private-equity sector. This could be helpful. With a full-court press under way in Washington to get private-market funds, like private equity, into Americans” 401(k) retirement plans, it’s more urgent than ever that alternative investments reflect market realities, not wishful thinking.” [the Wall Street Journal, 2025-07-01]

2024: The Average Secondary Market Sale Of Private Equity Assets Was An 11 Percent Discount. According to the Wall Street Journal, “The real problem arises when investors unexpectedly need cash and can’t sell the holdings at their stated values. On the secondary market, private-equity stakes usually sell at a discount to their official values. Last year, the average discount was 11%, according to Jefferies.” [the Wall Street Journal, 2025-07-01]

Secondaries Have Become A Hot Area Of Private Equity

July 2025: Blackstone Began Exploring Launching A Fund To Purchase Stakes In Other Private Equity Assets From Managers Desperate For Liquidity. According to Bloomberg, “Blackstone Inc. is exploring further inroads into the booming private credit-secondaries market, people with knowledge of the matter said. The alternative investing giant is considering a stand-alone pool of capital to buy second-hand private credit funds, said the people, who weren’t authorized to speak publicly as the matter is private. That would be a departure from the current approach where it invests through its flagship private equity funds. A new strategy would fall under the remit of Blackstone’s Strategic Partners secondaries unit specializing in private equity, infrastructure and real estate. A spokesperson for Blackstone declined to comment. The private credit secondary market — where limited partners can sell their stakes to other institutions — is gaining momentum as fund managers look for liquidity to fund capital distributions in an M&A drought.” [Bloomberg, 2025-07-07]

Private Credit

Bridge Funding To Government Contractors Facing DOGE-Led Cuts Have Proved Lucrative To Private Credit Firms. According to the Financial Times, “Private credit lenders have found a new batch of clients: US government contractors short-changed by Elon Musk’s cost-cutting drive and trying to stay afloat. Legalist, a private capital lender based in San Francisco, told the Financial Times that its ‘government receivables’ business had extended more than $100mn in financing to dozens of contractors since the start of 2025, more than doubling the strategy’s previous total book of business. The group is looking to raise $250mn from investors to extend more similar loans. Contracts worth more than $70bn have been abandoned by the so-called Department of Government Efficiency (Doge), led by Musk until his falling out with President Donald Trump in May, according to HigherGov, a private research service. Loans from Legalist serve as bridge financing for government reimbursement on work that has been completed but not yet paid, often when traditional banks have balked at extending credit. Eva Shang, who co-founded Legalist as a litigation finance investor in 2016 as a participant in the Y Combinator start-up development programme, said the company’s government contractor business had historically been ‘small time’ and ‘slow going’ but had quickly accelerated as the Trump White House sought to shrink the size of the federal government.” [the Financial Times, 2025-07-08]

As Banks Balked At Loans Secured By Invoices Against The Trump Administration, Private Credit Was Able To Step In, At “A Pretty Big Premium.” According to the Financial Times, “One contractor with USAID, who spoke on the condition of anonymity, said it found itself in a tough situation earlier this year with the government owing it nearly $200mn for services already rendered when a stop-work order was issued. The company had existing credit lines with large banks but those facilities relied on historical accounts receivables that had already been collected to calculate a ‘borrowing base’. Those traditional financial institutions were unwilling to extend new liquidity amid the Trump actions against USAID, an agency targeted for an 83 per cent reduction in programmes by secretary of state Marco Rubio. ‘Banks had been pricing us as low risk. That wasn’t true anymore and it was easier for them to walk away rather than find a solution,’ said a finance executive at the contractor. Legalist provided as much as a $75mn credit line that was secured against monies owed for work the contractor already performed and as well as ‘termination budgets’ — what the government owed to make the company whole on previous expenditures for contracts that were to be cancelled. ‘We are paying a pretty big premium relative to an asset-backed facility with a main street bank,’ said the executive, but added that he appreciated the ‘creativity’ of the Legalist loan.” [the Financial Times, 2025-07-08]

Loans To Government Contractors Would Be Expected To Charge 12 Percent, Despite Only Covering 50-80 Percent Of Expected Reimbursements. According to the Financial Times, “Shang told the FT the government receivables strategy at Legalist, which has about 70 current borrowers, targets an interest rate of at least 12 per cent with the loan size roughly 50-80 per cent of the expected reimbursement.” [the Financial Times, 2025-07-08]

NOTE: 12 Percent is borderline Usury for this kind of Loan

The loans that these contractors are receiving while they wait for the Trump administration to pay them should, in theory, be extremely good collateral. As the times story noted:

In January, Doge issued a “stop work order” for all existing grants and contracts held by the development agency USAID. Over the next few months, it went on to issue similar orders via the departments of housing and urban development, homeland security and veterans affairs, among several others.

Federal procurement rules allow contractors whose work is upended by policy changes to get their already sunk outlays reimbursed — eventually.

If a stop work order is subsequently lifted — as many of Doge’s orders have been — contractors are entitled to compensation for “reasonable costs” incurred during the lull. In other instances, Doge issued “terminations for convenience” for thousands of government contracts outright, which allowed contractors to claim expenses incurred during wind-down.

“It’s kind of common wisdom in the government contractor community that if you get a termination for convenience you can sometimes be paid more than you would have under the contract,” Shang said. Some industry observers cited the Biden administration’s termination of several contracts agreed by the first Trump administration for the construction of a southern border wall, which ended up costing the government billions of dollars.

Combined with the fact that the Prompt Payment Act Requires government receivables to be paid within 30 days, or else an interest rate (currently 4.625%) is applied to whatever is owed, should make for what can only be called asset for lenders to loan against.

Unfortunately, Trump’s record of paying his bills speaks for itself, and it seems that the only lenders available have been able to charge interest rates more in line with junk bonds than investment grade, or treasury debt. This despite the fact that these contractors’ assets will be short-term, interest-bearing obligations against the Federal government, at a 50-80 percent LTV.

Code

# Gather The databbb=get_data(f, "BAMLC0A4CBBBEY"; observation_start="2015-07-07", observation_end="2025-07-07",).data ccc=get_data(f, "BAMLH0A3HYCEY"; observation_start="2015-07-07", observation_end="2025-07-07",).data t1y=get_data(f, "DGS1"; observation_start="2015-07-07", observation_end="2025-07-07",).data # Make the Plotplot(bbb.date, bbb.value; xlabel="Date", ylabel="Yield", title="Trump's Recievables Trade Like Junk", linewidth=2, label="BBB",)plot!(ccc.date, ccc.value; label="Junk", linewidth=2,)plot!(t1y.date, t1y.value, label="1 Year Treasury", linewidth=2, )hline!([12.0]; label="Target", linewidth=2, linestyle=:dash,)

Tax Avoidance

Taking Advantage Of ETFs’ Tax-Advantaged Structure To Off An S&P 500 Tracking Product That Excludes Dividends. According to Bloomberg, “Wall Street’s latest tax dodge doesn’t hide in the Cayman Islands or rely on complex derivatives. It’s engineered to turn a publicly traded fund into a tax-minimizing machine that hums quietly on autopilot. While dividends have long been a defining feature of stock investing — a sign of corporate discipline and investor reward — Roundhill Investments plans to launch the S&P 500 No Dividend Target exchange-traded fund on July 10 with the ticker XDIV. Its ambition is simple but strategic: track the performance of the famous benchmark while dodging its payouts. The fund will sell holdings just before their dividend dates — steering income away from ETF shareholders and, in the process, away from their tax bills. As stock benchmarks have climbed in recent years and tax bills have grown alongside them, asset managers are building products that give investors more control over when — and whether — they owe taxes. These rely on sophisticated mechanisms to reduce taxable events, essentially transforming the fund structure into a programmable tax-sensitive tool. These strategies are executed through US-regulated ETFs that trade on public exchanges, offering investors easy access and the kind of fiscal flexibility once reserved for private wealth clients. It’s ‘for people who are tax-aware — intended for people who want to have S&P 500 exposure without the downside of distributions,’ said Dave Mazza, chief executive officer at Roundhill. ‘There hasn’t been a product in the market to meet the needs of investors for this.’ While most ETFs already sidestep capital gains by using a mechanism known as in-kind redemptions, XDIV’s strategy takes aim at a different category of tax exposure: ordinary income. The fund, which will charge a 0.0849% fee at the start, will invest in other S&P 500 ETFs, such as Vanguard’s VOO, but will exit positions just before ex-dividend dates. It will then rotate from one such index fund into another that isn’t about to pay a distribution.” [Bloomberg, 2025-07-07]

[the Yale Budget Lab,

[the Yale Budget Lab,