Unequivocally, Trump’s economy got worse over the weekend. In addition to Friday’s data from the national association of relators showing that a median home would be unaffordable for a median household, risk factors accumulated in force. The financial world has run wild with Trump’s volatility and promises not to regulate, with more leveraged or inverse single share ETFs launched in the first half of 2025 than in all of 204, including a leveraged CLO ETF. The crypto treasury strategy could be in trouble, with Strategy (formerly MicroStrategy), the holders of more than 3 percent of all bitcoin in existence, issuing notes to pay for dividends promised to the holders of securities issued earlier to pay for bitcoins. To make matters worse, private credit’s rise and private equity’s struggles have made the pool of financing available for buyouts much more in debt than equity, driving up leverage ratios.

Meanwhile, Trump’s trade war continues to make life worse for Americans, with even Oren Cass, the exemplar of a bad-faith defender of tariffs noting that the volatile way in which Trump has rolled out his tariffs “maximizes the disruption and creates the weakest incentives [for reshoring]. While businesses have announced plans to raise prices, Trump poured gasoline on that situation with Tariffs effecting the largest grower of the type of coffee Americans drink, and major industrial inputs like copper and steel. Speaking of gasoline, as the largest Oil exporter, the American economy will suffer from the fact that the IEA projected the slowest non-pandemic growth in global oil demand since the pandemic. These higher prices and lower incomes will only–according to three AEI economists–be exacerbated by Trump’s immigration crackdown, which will reduce income growth and raise prices, all while reducing the labor force and employment.

It is no wonder then, that things have started to break. In the second quarter of 2025, more high-grade debt was downgraded than upgraded for the first time since early 2021, while more than 11 times as much debt dropped down to junk than moved up to investment grade. And if that were not enough, major stories about corrupt practices, either to funnel tens of millions of dollars a year to the Trump family, or to disadvantage workers in Republican states broke.

Releases

Code

include("../scripts/oxocarbon-plot.jl")theme(:oxocarbon)usingFredData, DataFrames, Dateskey=ENV["FRED_API_KEY"]f=Fred(key)hai=get_data(f, "FIXHAI"; ).databar(hai.date, hai.value .-100; title="Housing Affordability Went Negative In May 2025", xlabel="Month", ylabel="Ease of Purchase", legend=false,)hline!([0.0]; linewidth=2, linestyle=:dash,)

NOTE: The National Association of Realtor’s created the Home Affordability Index to show that, at a value of 100, a family with a median income could afford median home on a typical 30 year mortgage with 20 percent down. In this plot, I adjusted the measure to have zero be typical affordability, with a positive value being affordable and a negative value being unaffordable.

Financial Instability

January 2025 - June 2025: More Leverage Or Inverse Single Share ETFs Have Been Launched Than Total Leveraged Or Inverse ETFs Launched In 2024. According to Bloomberg, “A record 73 leveraged or inverse ETFs launched in the US in 2024, according to Bloomberg Intelligence, more than the two prior years combined, and over half were single-stock. This year has already eclipsed that, with more than 100 leveraged or inverse products overall, three-quarters of which are single stock.” [Bloomberg, 2025-07-10]

July 2025: The First Levergaed CLO ETF Was Launched. According to Bloomberg, “Reckoner Capital Management is testing investors’ hunger for a new category of risky bets with an exchange-traded fund that uses leverage to juice returns on collateralized loan obligations. The Reckoner Leveraged AAA CLO ETF (ticker: RAAA) is the first such fund to invest in a variety of top-rated CLO bonds while leveraging up to 50% of that exposure, according to a statement. The ETF arrives amid strong demand for collateralized loan obligations, which bundle buyout debt into bonds. Retail investors are also embracing leveraged investment strategies, once considered the province of investment professionals, like hedge funds and asset managers, that can move in and out of wagers quickly.” [Bloomberg, 2025-07-09]

Ponzi Dynamics

July 2025: Strategy Announced A $4.2 Billion Offering To Raise Cash To Pay Dividends. According to FT Alphaville, “Earlier this week, Strategy announced a $4.2bn at-the-market offering of Stride. On the surface, it looks like yet another bid to raise cash for more bitcoin purchases. But tucked away in the announcement was a telling clause: proceeds may also be used to pay dividends on other classes of preferred shares, namely Strife and Strike (Alphaville emphasis added): Strategy intends to use the net proceeds from the ATM Program for general corporate purposes, including the acquisition of bitcoin and for working capital, and may also use the net proceeds for the payment of dividends to holders of its 10.00% Series A Perpetual Strife Preferred Stock, $0.001 par value per share and 8.00% Series A Perpetual Strike Preferred Stock, $0.001 par value per share. This isn’t a refinancing, where a company swaps expensive capital for cheaper funding. Nor is it a typical dividend recapitalisation, where a company borrows to pay shareholders dividends. A dividend recap usually assumes the business generates enough cash to support more debt. Strategy’s legacy software division doesn’t produce enough free cash flow to cover these preferred dividends, and bitcoin, of course, pays no income. Instead, this manoeuvre is something different. Strategy is effectively reserving the right to use money from new securities to prop up old ones, reassuring investors that it can keep issuing fresh paper to cover dividend payments. This in turn is meant to give them confidence to buy the future rounds of preferred shares.” [FT Alphaville, 2025-07-10]

Strategy’s Business Model Has Been To Raise Capital To Buy Bitcoin. According to FT Alphaville, “Michael Saylor’s company Strategy, formerly known as MicroStrategy, doesn’t just believe in bitcoin — it has staked its entire future on it. Since pivoting from enterprise software to crypto back in August 2020, it has transformed into a bitcoin investment vehicle, with its shares surging more than 25-fold. But beneath the euphoria lies a capital structure that’s becoming increasingly self-referential. Strategy’s approach to financing has had three key elements. First, it has issued ever larger amounts of common stock to raise money for buying bitcoin, taking advantage of its shares trading at roughly twice the company’s net asset value (NAV). Second, it has issued huge sums of convertible bonds, exploiting the high volatility of its own shares to secure phenomenally favourable terms. Initially these convertibles were secured against its bitcoin holdings, but today the outstanding bonds are unsecured, removing the risk of margin calls. If the share price fails to rise enough for the bonds to convert, the company still has to repay the money, but maturities have been pushed out, giving Strategy breathing room (at least until the first investor put in September 2027) even if bitcoin prices drop sharply. Third, it has issued three classes of perpetual preferred shares — Strike (STRK), Strife (STRF) and Stride (STRD) — with high, discretionary dividends, some of which can be paid in kind.” [FT Alphaville, 2025-07-10]

FT Alphaville: While “The Music Plays On,” If Strategy Trades Below NAV, Or Bitcoin Falls, The Company Has No Plan B. According to FT Alphaville, “Dependence on these two factors carries obvious risks. The company has no hedge, no diversified income, and no plan B. Its fate hinges on the assumption that capital will always be available and bitcoin’s price will either rise or, at the very least, stay elevated. A prolonged downturn or shut-off from funding could force the unthinkable: selling bitcoin to meet dividend payments. This would represent an existential crisis for a ‘buy and HODL’ maximalist. For now, the music plays on. Bitcoin’s rally boosts both Strategy’s NAV and the stock’s premium to NAV, and investors continue to clamour for Saylor’s paper. But each new layer of financial engineering makes the structure shakier. Strategy has proven its approach pays off in a bull market. The question is whether it can withstand the storm when the tide inevitably turns.” [FT Alphaville, 2025-07-10]

July 2025: Strategy Was The Largest Corporate Holder Of Bitcoin. According to FT Alphaville, “The logic was simple: raise as much money as possible to buy bitcoin. Strategy is now by far the largest corporate holder of bitcoin anywhere. Yet its latest move may mark a shift.” [FT Alphaville, 2025-07-10]

July 2025: Strategy Owned 597,325 Bitcoins. [Strategy, accessed 2025-07-11] NOTE: This amounts to roughly 3 percent of all bitcoins in existence.

Code

usingYFinancebtc_dat=get_prices("BTC-USD"; range="1y", interval="1wk") |> DataFrameplot(Date.(btc_dat.timestamp), 100.0./((btc_dat.vol ./ btc_dat.adjclose)./597_325); xlabel="Week", ylabel="Current MSTR Holdings, % Weekly Volume", title="Strategy's Bitcoin is a significant share of BTC volume", linewidth=2)

Higher Leverage

PGIM Head Of Direct Lending: “Leverage Is Also Stretching.” According to Bloomberg, “Finding steep competition from the broadly syndicated market, private credit firms are offering one benefit to potential borrowers: leverage. Direct lenders are pitching higher leverage ratios as a sweetener for deals, particularly for companies owned by private equity firms. Tacking on more debt gives companies flexibility to make acquisitions, and can fund a dividend payout to shareholders, also known as a dividend recapitalization. ‘We are seeing fierce competition for the highest quality assets, and with that, the illiquidity premium is shrinking,’ said Matt Harvey, the head of direct lending at PGIM Private Capital. ‘Leverage is also stretching, in addition to terms, but we aren’t observing a blatant abuse of credit underwriting standards.’ Facing a hot broadly syndicated market, private credit lenders have been focused on finding ways to entice borrowers. With many firms unable to compromise on tighter pricing, offering more leverage can be a draw. Ways to add more leverage can also include accepting heavily adjusted earnings metrics or providing delayed draw term loans.” [Bloomberg, 2025-07-10]

Private Credit Has Pushed Some Companies’ Leverage To Six Times Earnings. According to Bloomberg, “For some companies, private credit has pushed their leverage to over six times earnings, according to people with knowledge of the matter, a level viewed as relatively high by Wall Street standards. Deals for companies within some industries, such as software or business services, have tacked on leverage more than eight times earnings, said the people, who asked not to be identified discussing private information.” [Bloomberg, 2025-07-10]

Private Credit Companies Have Offered Generous Drawdown Provisions And Payment In Kind Options. According to Bloomberg, “Private credit can offer more flexibility than a syndicated transaction and some large cap managers are offering features including large delayed draw commitments or payment-in-kind options to compete against such financings, according to Freund. Delayed draw term loans give borrowers access to the full amount at deal close, with the option to borrow at a later date.” [Bloomberg, 2025-07-10]

2025: Around 45 Percent Of Companies Financed By Private Debt Risked Breaching Their Leverage Cap, A Three-Fold Increase As Compared To Buyouts Completed Between 2010 And 2019. According to Bloomberg, “Around 45% of companies financed by private debt are in danger of breaching their leverage cap, which is based on interest coverage ratio of two times, a measure of earnings compared to interest payments, according to a report from MSCI. That marks an almost three-fold increase compared to buyout vintages from 2010 to 2019.” [Bloomberg, 2025-07-10]

2020 - 2025: The Share Of High-Yield Borrowers Delaying Payments By Accumulating More Debt, Payment-In-Kind, More Than Doubled. According to Bloomberg, “There are other reasons to be worried about credit quality now. High-yield borrowers are delaying about 9% of interest payments globally, known as paying in kind, according to JPMorgan Asset Management’s Oksana Aronov, up from about 4% in 2020. And cash balances at high-grade US companies are showing signs of starting to fall. The second quarter earnings season begins in the US in the coming week, and will give more insight as to how companies are faring.” [Bloomberg, 2025-07-12]

How Much Leverage 6x Earnings Is

It is a lot. Especially because PE and Private Credit companies typically look at EBITDA rather than net profits (before interest) for earnings. To give you an idea, the 250th company in the S&P 500, Targa Resources had $4.1 billion in EBITDA, but about $2 billion in net income before interest. At 6x EBITDA leverage, that would imply $24.6 billion in debt. At a 6 percent interest rate, that would be $1.4 billion in interest, meaning that a 30 percent fall in profits wold see the company unable to meet interest payments out of profits from operations.

Interest Rate

Profit Fall to Require Borrowing to Pay Interest

5

38.5 %

7

14.4 %

8.13

0.0 %

At an interest rate of only 8.13 percent, Targa would have to grow its profit just to be able to meet its interest obligations.

Trade War

July 2025: The IEA Forecast The Slowest Global Oil Demand Growth Since 2009 (Excluding The Pandemic). According to the Financial Times, “The International Energy Agency has said it expects global oil demand to grow at the slowest pace since 2009, outside of the coronavirus pandemic, amid early signs that US tariffs are weighing on economic activity. The energy advisory body said it expected consumption to increase by only 700,000 barrels a day this year. That would be the smallest rise in annual demand since the aftermath of the global financial crisis, with the exception of 2020 when demand contracted by 8.7mn b/d as governments shut key parts of the economy in order to contain the spread of Covid-19. In its monthly oil market report, the IEA said it had trimmed its forecast from a previous growth estimate of 720,000 b/d, after lower than expected demand in the second quarter of the year, particularly in emerging markets. While the slowdown in growth in the past three months was ‘partly weather related’, the IEA also flagged the impact of the economic uncertainty created by US President Donald Trump’s surprise tariffs on many trading partners. ‘Although it may be premature to attribute this slower growth to the detrimental impact of tariffs manifesting themselves in the real economy, the largest quarterly contractions occurred in countries that found themselves in the crosshairs of the tariff turmoil,’ it said.” [the Financial Times, 2025-07-11]

Helen Of Troy, Makers Of OXO, Revlon, Honeywell, Vicks, And Others Saw A Large Earnings And Operating Margin Decline Due To: “Cancellation Of Direct Import Order”, “Tariff-Related Pull Forward”, And “Consumer[s] Trading Down.” According to Bloomberg, “Moving on to the quarter, our Q1 results were well below our expectations. Tariff-related disruption on our shipments was greater than we originally expected in April. There are three tariff-related impacts making up approximately 8 percentage points of the 10.8% consolidated revenue decline. One, cancellation of direct import orders from China in response to higher tariffs. Two, tariff-related pull forward of orders into the fourth quarter of fiscal ’25, leading to elevated inventory and lower replenishment in the first quarter of fiscal ’26, which we expect to continue into the second quarter as demand continues to soften. And three, China softness driven by a shift from cross-border e-commerce, the localized distribution models, and increased competition from domestic sellers driven by government subsidies. In addition to tariff-related impacts, we also saw weeks of supply adjustment at certain key retailers as shifting consumer demand curves are being reflected in retailers inventory management practices. Finally, we are seeing clear evidence of the consumer trading down with average price compression of 3% to 4% in our US business, which impacted first quarter revenue and profitability. You may have seen other companies recently calling out trade down behavior, including the Dollar stores, which are a beneficiary of this trend.” [Bloomberg, 2025-07-11]

Chaos

Even Oren Cass, A Stark Defender Of Trump’s Tariffs, Has Noted The Negative Consequences Of Their Uncertainty. According to Oren Cass in the Financial Times, “If a tariff starts at zero but companies believe it will reach 50 per cent in a few years, they will invest as quickly as if the rate starts at 50 per cent. But starting the rate at 50 per cent, and leaving companies to guess what it will be in the future, maximises the disruption and creates the weakest incentive.” [Oren Cass in the Financial Times, 2025-07-11]

Higher Prices

Helen Of Troy CFO: In Response To Tariff-Driven Profit Losses, The Company Planned To Deploy “Strategic Price Increases That Will Take Effect Near The End Of Summer.” According to Bloomberg, “To offset all this, and despite evidence that consumers are moving to cheaper goods, Helen of Troy’s CFO said the company is deploying “strategic price increases that will take effect near the end of summer.” These price increases are apparently on average in the 7% to 10% range. The company’s stock sank a stunning 22.7% yesterday.” [Bloomberg, 2025-07-11]

Coffee

2024: The U.S. Imported 30 Percent Of Its Coffee From Brazil, Which Has Been The Top Producer Of Americans’ Preferred Arabica Variety. According to Bloomberg, “The US imported nearly $2 billion worth of coffee from Brazil in 2024, according to the US Department of Agriculture. The shipments are roughly 30% of US coffee consumption, Brazilian coffee exporters group Cecafé said. ‘It’s a loss to our companies, and it means more costs and more inflation to American consumers,’ Cecafé Chief Executive Officer Marcos Matos said. Brazil is the world’s top grower of the premium arabica variety favored by Starbucks Corp. and most specialty coffee shops. Prices for the bean have already surged over the past year as poor weather in Brazil threatened supplies. Tariffs on Brazil could result in coffee prices rising ‘quite a lot,’ Giuseppe Lavazza, chairman of Italian roaster Lavazza, said on Bloomberg Television.” [Bloomberg, 2025-07-10]

Steel

June 2025: Nucor, An American Steel Maker, Raised Prices To Take Advantage Of “Favorable Market Conditions” (Their Compeditors’ Products Being Tariffed). According to Steel Industry News, “Nucor Corporation has implemented another price increase effective June 20, 2025, raising its Consumer Sport Price (CSP) for hot-rolled coil to $910 per ton for all producing mills, with California Steel Industries (CSI) pricing set at $970 per ton. This $20 per ton increase represents the company’s ongoing effort to capitalize on favorable market conditions while navigating the complex landscape of tariff uncertainty, stable but cautious demand, and evolving produciton dynamics that characterize the steel industry heading into the second half of 2025.” [Steel Industry News, 2025-06-30]

Code

usingCSVprice_data=DataFrame(CSV.File("../resources/2025-07-14/Nucor-Prices.csv"))price_data.Week_Of =Date.(price_data.Week_Of)plot(price_data.Week_Of, price_data.CSP_Price; linewidth=2, label="Nucor Price", xlabel="Week Of", ylabel="Consumer Spot Price / Ton", title="Prices Up More Than 50 Percent Since December",)hline!([950.0]; linewidth=2, linestyle=:dash, label="Cleveland Cliffs July Price")

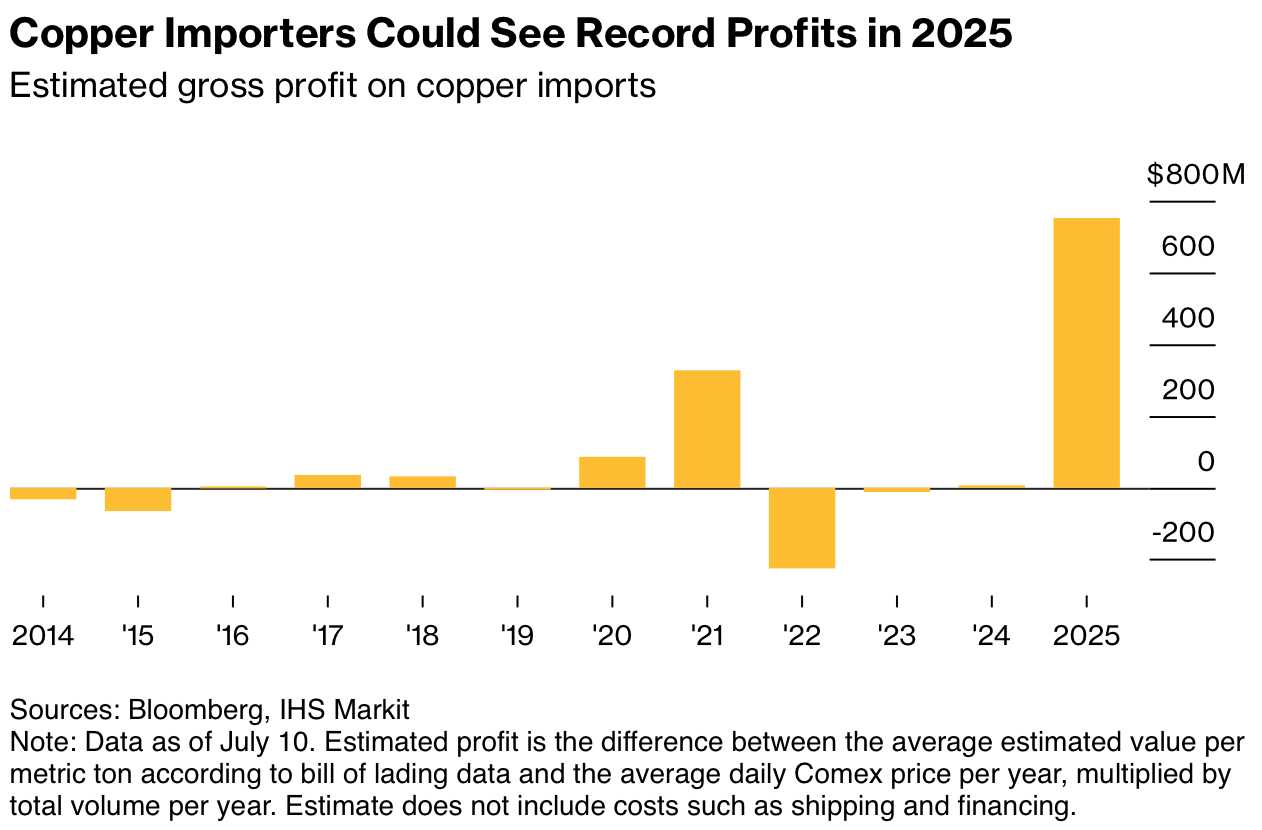

Copper

July 2025: Before Trump’s Copper Tariffs Went Into Effect, Americans Were Already Paying 25 Percent More For Copper Than The Rest Of The World. According to Bloomberg, “With US prices about 25% higher than the LME’s global benchmark, US consumers are already feeling the impact of the tariffs, which Trump says will help support the development of a domestic copper industry.” [Bloomberg, 2025-07-11]

While American Businesses, Especially Those Exposed To The Power Industry, Higher Copper Prices Will Lead To Higher Prices And Thinner Margins, But Commodity Traders Have Made $500 Million In The Lead Up To Trump’s Tariffs. According to Bloomberg, “For American businesses, surging copper prices mean higher costs and thinner margins, especially alongside levies on steel and aluminum that are already in place. Copper is mainly used in power infrastructure for its conductivity — making it key for both the energy transition and the data center boom — but it’s found in everything from air conditioners to electric vehicles. With US prices about 25% higher than the LME’s global benchmark, US consumers are already feeling the impact of the tariffs, which Trump says will help support the development of a domestic copper industry. The immediate winners are clear: The commodity traders, miners and banks that have been able to ship copper to the US. Based on the simple math of the wide gap between prices in the US and the rest of the world, the flood of imports may have delivered a combined windfall of roughly $500 million, divided between the producers who’ve been able to sell their metal at high premiums, logistics companies being paid top dollar to fast-track shipments, and — the lion’s share — to traders.” [Bloomberg, 2025-07-11]

Through July 10, 2025, Copper Importers Profited More Than In Any Year Since At Least 2014.[Bloomberg, 2025-07-11]

Bloomberg: Consensus Expectation For Higher American Copper Prices Than Abroad Would Disadvantage American Manufacturers. “Unfortunately, We Have To Pass The Increase To The Customers.” According to Bloomberg, “The consensus expectation is that prices on the LME will fall while Comex continues to wind higher in advance of the tariffs, baking in a major cost disadvantage for US manufacturers. That, combined with stiff tariffs on steel, aluminum and other key industrial raw materials, will fan worries about inflation in the US, and anxiety about an ensuing slowdown in other major economies. ‘Unfortunately we have to pass the increase to the customers, and we have no idea how they’re going to handle it,’ said Charles Bareijsza, chief executive officer and president of New Jersey-based distributor Metal Associates, which sells copper products including sheets, pipes and wires. ‘We tried to forewarn them. I called our largest customer and I said to them, “Be prepared.”’” [Bloomberg, 2025-07-11]

Economic Degradation

Immigration

AEI: Trump’s Push Against Immigration Would Reduce Income Growth By 0.3-0.4 Percent, While Reducing The Labor Force And Employment. According to Edelberg, Verger, and Watson in AEI Economic Perspectives, “We assess the macroeconomic implications of the observed and expected changes to immigration policy during the second Trump administration. We project that net migration in 2025 will be between −525,000 and 115,000, reflecting a dramatic decrease in inflows and somewhat higher outflows. Net migration may be reduced even further in 2026 before rebounding in 2027 and 2028. These changes will reduce gross domestic product growth by 0.3–0.4 percentage points in 2025 and put significant downward pressure on growth in the labor force and employment. Monthly payroll employment growth could be near zero or negative in the next few years.” [Edelberg, Verger, and Watson in AEI Economic Perspectives, July 2025]

AEI: Trump’s Immigration Policies Could Push Sustainable Employment Growth From Between 140 And 180 Thousand Per Month To Between 10 And 40 Thousand Per Month. According to Edelberg, Verger, and Watson in AEI Economic Perspectives, “Slowing immigration will put significant downward pressure on growth in the labor force and employment. Potential employment growth, meaning employment growth when the labor market is operating sustainably at “full employment,” could be between 10,000 and 40,000 jobs a month in the second half of 2025 (down from 140,000 to 180,000 in 2024), and potential job growth could turn negative in the second half of Trump’s term.” [Edelberg, Verger, and Watson in AEI Economic Perspectives, July 2025]

Under AEI’s Low Scenario, The Range Of NAIR Employment Growth By 2028 Could Have Employment Decline At Its Low End. According to Edelberg, Verger, and Watson in AEI Economic Perspectives, “We estimate that the labor market in 2025 could accommodate employment growth of 40,000 to 70,000 in that scenario, lower than the range projected for 2025 before the pandemic. The range is shifted down by increasing amounts over time in our projections as declines in net migration take an increasingly large toll on labor force growth. For example, in 2028 the range in potential employment growth spans a decline in employment of 10,000 a month and an increase of 30,000.” [Edelberg, Verger, and Watson in AEI Economic Perspectives, July 2025]

AEI: Reducing The Labor Force By 1.3 Million Workers Would, All Else Being Equal, Raise The Rate Of Inflation By 0.5 Percent A Year For The Next Three Years According to Edelberg, Verger, and Watson in AEI Economic Perspectives, “A lower level of immigration reduces the economy’s ability to produce goods and services because it reduces the size of the labor force. In the near term, a reduction in the size of the labor force—all else equal makes it more expensive for firms to produce goods and services and thus results in higher inflation. For example, McKibbin et al. (2024) estimate that a reduction in labor supply of 1.3 million workers resulting from mass deportations would raise the price level by 1.5 percent over three years (or, in other words, it would raise the rate of inflation by an average of 0.5 percentage points from 2025 to 2028).” [Edelberg, Verger, and Watson in AEI Economic Perspectives, July 2025]

Things Breaking

Q2 2025: For The First Time Since Early 2021, More High-Grade US Debt Was Downgraded Than Upgraded. According to Bloomberg, “Credit rating downgrades are becoming more frequent, the latest sign that companies are starting to perform worse and raising fresh questions about whether corporate debt valuations should be as high as they are. In the second quarter, around $94 billion of high-grade US debt was downgraded, compared with just $78 billion of upgrades, according to JPMorgan Chase & Co. strategists. It was the first time since early 2021 that downgrades outpaced upgrades in dollar terms, and more companies are at risk of being demoted later this year as economic uncertainty rises, JPMorgan strategists including Eric Beinstein and Silvi Mantri wrote this week.” [Bloomberg, 2025-07-12]

Q2 2025: More Than 11 Times As Much Debt Was Dropped Below Investment Grade Than Went From Sub-Investment Grade To Investment Grade. According to Bloomberg, “But by at least some measures, including not just ratings downgrades but also companies losing investment-grade status, the outlook is deteriorating. In the second quarter, there were about $34 billion of debt known as Fallen Angels, or bonds cut to junk, compared with just $3 billion of rising stars, JPMorgan strategists said. And on Friday, US President Donald Trump threatened a 35% tariff on some Canadian goods, ramping up his trade rhetoric.” [Bloomberg, 2025-07-12]

July 2025: Florida’s Brightline Railroad Was Forced To Defer Some Of Its Interest Payments Due To Lower-Than-Expected Ridership And Higher Than Expected Costs. According to Bloomberg, “Brightline Trains Florida, the private passenger railroad between Miami and Orlando, is deferring interest payments on some of its debt as it burns cash to offset lower-than-expected ridership and higher costs. The Fortress Investment Group-backed railroad plans to defer a July 15 interest payment on about $1.2 billion of 10% and 12% coupon tax-exempt bonds, according to Ashley Blasewitz, a spokesperson for Brightline. The deferred payments are the latest signs of trouble for Brightline in its attempt to bring high-speed rail to the main travel corridors of Florida.” [Bloomberg, 2025-07-11]

Corruption

Binance’s Support For Trump’s Crypto Projects

Before Binance’s Founder Publicly Asked Trump For A Pardon, His Company Wrote The Code For Trump’s Stablecoin. According to Bloomberg, “One of the Trump family’s crypto ventures has received key behind-the-scenes help from the world’s largest digital-asset exchange, whose founder is a convicted felon now seeking a presidential pardon. Binance wrote the basic code to power USD1, a stablecoin launched by the Trumps” World Liberty Financial Inc., according to three people familiar with the matter. They asked not to be named because the arrangement was private. Later, Binance’s founder and principal owner, Changpeng Zhao, said publicly that he had applied for a pardon. CZ, as he’s known, pleaded guilty in 2023 to failing to maintain an effective anti-money-laundering program. The coding work — writing the ‘smart contract’ that governs how USD1 tokens are created — helped make USD1 available for use in a $2 billion transaction this spring when an investment firm founded by the United Arab Emirates used it to buy a stake in Binance. Now, more than two months since that transaction, more than $2 billion in USD1 — roughly 90% of all coins outstanding — remains in Binance’s wallets, according to blockchain data. The assets backing that sum generate interest income, which could reach tens of millions of dollars for the Trumps on an annual basis. Binance also promoted USD1 to its 275 million users, a sought-after benefit among stablecoin issuers.” [Bloomberg, 2025-07-11]

More Than 90 Percent Of The USD1 Tokens Ever Created Were Used For A UAE-Founded Entity To Invest $2 Billion Into Binance, Providing Millions Of Dollars In Income To The Trump Family. According to Bloomberg, “The coding work — writing the ‘smart contract’ that governs how USD1 tokens are created — helped make USD1 available for use in a $2 billion transaction this spring when an investment firm founded by the United Arab Emirates used it to buy a stake in Binance. Now, more than two months since that transaction, more than $2 billion in USD1 — roughly 90% of all coins outstanding — remains in Binance’s wallets, according to blockchain data. The assets backing that sum generate interest income, which could reach tens of millions of dollars for the Trumps on an annual basis. Binance also promoted USD1 to its 275 million users, a sought-after benefit among stablecoin issuers.” [Bloomberg, 2025-07-11]

When USD1 Launched, Binance Added It To A Program That Compeditor Circle Had To Pay $60 Million To Join. According to Bloomberg, “When USD1 launched, World Liberty listed only one business partner: Palo Alto, California-based BitGo Inc., which said it would provide the ‘underlying infrastructure and user experience’ for minting and burning the stablecoins. ‘Minting and burning’ means creating new tokens when users buy them and destroying them when they”re cashed in. A BitGo spokesperson declined to comment. Soon after World Liberty announced its new stablecoin, the BNB Smart Chain that was founded by Binance made the new token part of a broad promotion campaign that offers zero transaction fees on trades. Binance’s spokesperson said the campaign is designed ‘to promote stablecoins built on BNB Chain.’ ‘BNB Chain is open to all projects in principle, and particularly welcomes stablecoins,’ she said. A recent regulatory filing by Circle Internet Group Inc., another stablecoin issuer, suggests how valuable promotional help can be. It said Circle paid Binance $60 million upfront in part to promote its coin, USDC, and agreed to share future revenue with the exchange. Under the two-year deal, Binance also agreed to hold USDC in its company treasury. World Liberty’s new stablecoin got off to a slow start, according to blockchain data, which isn’t surprising. There are many competitors, some of them well established, and all of them offer similar, if not identical, functionality.” [Bloomberg, 2025-07-11]

May 2025: Trump’s SEC Dropped A Lawsuit Against Binance. According to Bloomberg, “Meanwhile, Zhao’s relationship with US regulators has improved markedly. In May, the Securities and Exchange Commission dropped a lawsuit against Binance that had been filed in June 2023, one of several crypto-focused enforcement actions the regulator has either abandoned or paused. The SEC had accused the exchange of, among other things, lying to regulators about its operations in the US. The lawsuit quoted Binance’s former chief compliance officer texting a colleague, “We are operating as a fking unlicensed securities exchange in the USA bro.” The SEC said it was dropping the case “in the exercise of its discretion and as a policy matter.”” [Bloomberg, 2025-07-11]

Florida’s Citadel Non-Competes

July 2025: Florida Enacted Legislation Pushed By Ken Griffin Allowing Non-Compete Agreements Of Up To Four Years. According to Bloomberg, “Florida enacted legislation allowing non-competes of up to four years, handing a victory to Citadel’s Ken Griffin, who pushed for the policy. Labor lawyers say it’s one of the most employer-friendly policies in the country. It also goes in the opposite direction of many states, which have been trying to rein in or ban non-competes. The law’s supporters say it protects trade secrets and will help attract high-paying employers to Florida. ‘Florida is poised to become one of the finance capitals of the world,’ said Senator Tom Leek, one of the bill’s sponsors. ‘And if we want to attract those kinds of clean, high-paying jobs, we have to provide those businesses protection on the investment that they”re making and their employees.’ The bill became law without the signature of Governor Ron DeSantis under a rarely-used article in Florida’s constitution. If the governor fails to act on — or veto — a bill that’s been approved by the legislature, it becomes law within about two weeks. Florida employers can now ask for four year non-competes and ‘garden leaves’ — where employers continue to pay salaries and benefits. Employees though are mostly unable to re-enter the labor market. Employers also won’t have to pay bonuses, which can make up the majority of compensation at finance firms.” [Bloomberg, 2025-07-08]

[Bloomberg,

[Bloomberg,