August 7, 2025

Economic Degradation

Higher Prices

The Prospect Of Higher Inflation Standing In The Way Of Fed Cuts Reduced Demand For Treasuries, Raising The Interest Rate. According to Bloomberg, “The Treasuries market saw most yields rise Tuesday after the first of this week’s three auctions of new notes and bonds drew weak demand. Yields for shorter-dated tenors rose the most, with the two-year note’s settling around four basis points higher Tuesday afternoon. Longer-maturity yields were little changed or slightly lower. While Treasuries had been rallying since last week, the auction result validated concern in some quarters of the market that yields had declined too much, and offered inadequate compensation for the risk that inflation data will stand in the way of expected Federal Reserve interest-rate cuts. A gauge of inflation in the US economy’s service sector compiled by the Institute for Supply Management unexpectedly increased in July to the highest level since October 2022. The $58 billion sale of three-year notes drew 3.669% versus its 3.662% yield in pre-auction trading shortly before 1 p.m. New York time, the bidding deadline. An auction is said to tail when the result indicates investors demanded a higher yield than indicated by pre-auction trading.” [Bloomberg, 2025-08-05]

Upward Redistribution

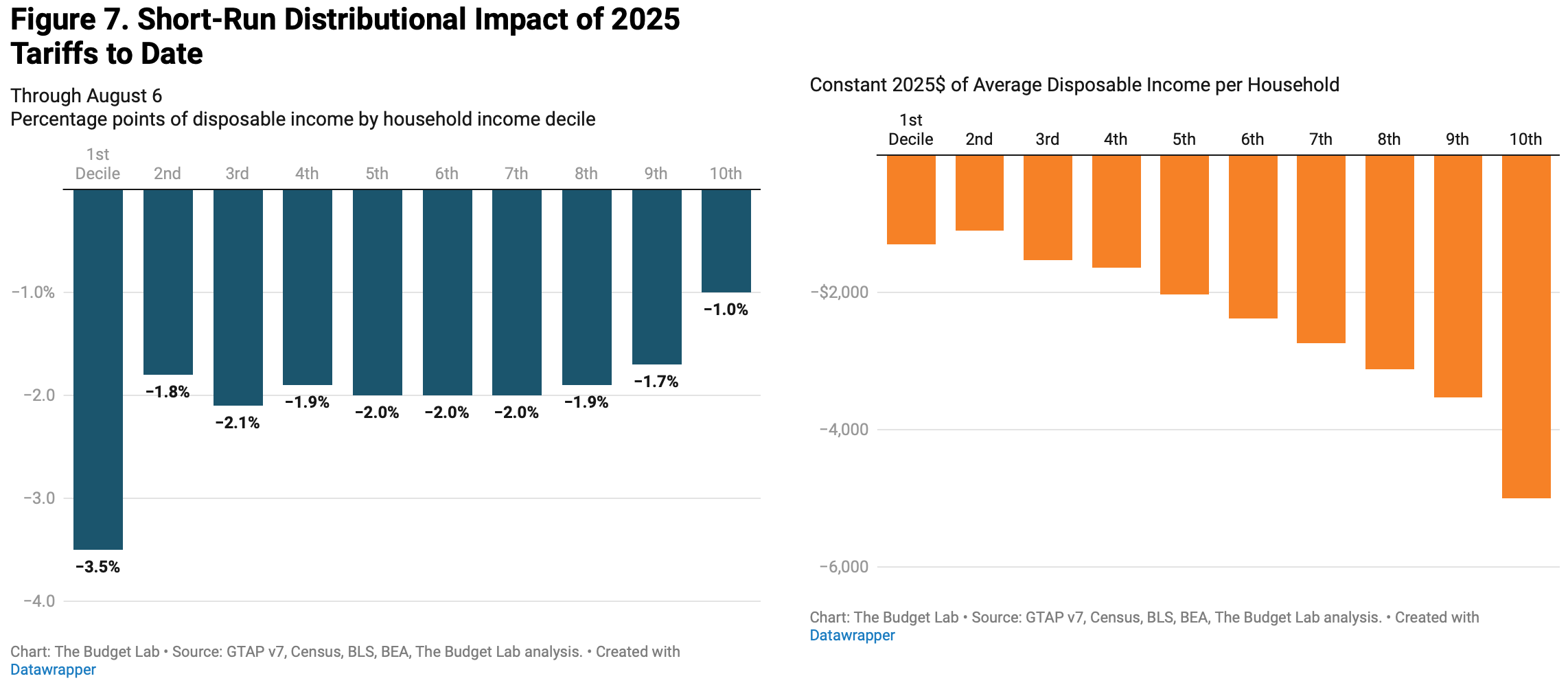

Yale Budget Lab: Trump’s Tariffs “Burden Households At The Bottom Of The Income Ladder More Than Those At The Top,” Costing The Median Household $2,200. According to the Yale Budget Lab, “Tariffs are a regressive tax, especially in the short-run. This means that tariffs burden households at the bottom of the income ladder more than those at the top as a share of income. The regressivity is about the same when looking at all 2025 tariffs: the short-run burden on the 1st decile is more than 3x that of the top decile (-3.5% versus -1.0%). The average annual cost to households in the 1st and top decile rise to $1,300 and $5,000 respectively in 2025$. The median cost is $2,200 per household.” [Yale Budget Lab, 2025-08-07]

Weaker Growth

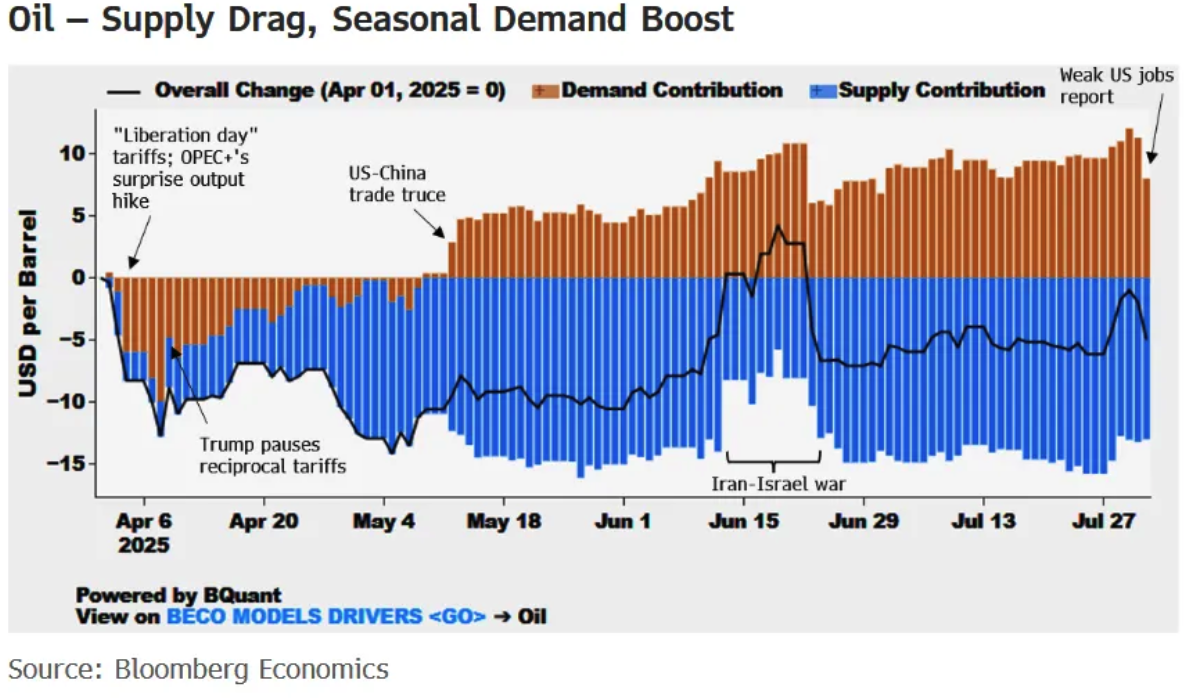

Unprofitable Oil Production

In Line With Trump’s Preferences, OPEC+ Has Dramatically Increased Oil Production, Putting Downward Pressure On Prices. According to Bloomberg, “OPEC+ will sharply hike production again in September to finish unwinding its latest tranche of supply cuts in a push for market share, but left a question mark hanging over its future options as global markets face a mounting surplus.aSaudi Arabia and its partners agreed on a video conference to add 547,000 barrels a day next month. This completes the accelerated reversal of a 2.2 million-barrel cutback made by eight members in 2023, and also includes an extra allowance being phased in by the United Arab Emirates. The latest hike caps a dramatic shift from the Organization of the Petroleum Exporting Countries and its partners, from defending prices to opening the taps. Their pivot has helped cap oil and gasoline futures amid geopolitical tensions and strong seasonal demand, offering some relief for drivers and a win for US President Donald Trump. But the added barrels are hitting a market that is already heading toward a sizable surplus.” [Bloomberg, 2025-08-03]

- Bloomberg Economics: The Weakening US Economy Could Be Expected To Further Weaken Oil Price Growth. According to Bloomberg,

[Bloomberg, 2025-08-05]

[Bloomberg, 2025-08-05]

Debt-Driven Shenanigans

Bloomberg: The Rise Of Legalistic “Liability Management Exercises” Have Made Creditors Less Willing To Jump Into Distressed Debt. According to Bloomberg, “Distressed debt investors are piling into a new strategy to make money from troubled companies. For decades, their playbook was simple: buy corporate bonds and loans when they first drop in value and profit from either a gradual recovery or, if things don’t improve, from restructuring negotiations that could hand them an equity stake in the company. Recent changes in the distressed-debt industry, though, have led some investors to change their approach after watching — and sometimes being stung by — the rise of so-called liability management exercises, which often pit creditors against each other in coercive, high-stakes battles that leave some participants nursing big losses. Those skirmishes have pushed a growing number of investors to hold off on buying a company’s debt until after it has gone through this kind of disruptive transaction and made it to the other side. At that point, the investment usually still offers the juicy yields associated with distressed companies, but now with strengthened terms to protect creditors if the borrower runs into trouble again.” [Bloomberg, 2025-08-04]

- The Potential Of A LME Leading An Investor To Lose Everything Has Made Jumping In Before Those Proceedings Are Completed Risky, Especially For Smaller Firms. According to Bloomberg, “Goel’s pivot illustrates some of the unintended consequences of the rise in LMEs, which have come to dominate the distressed market and are now spreading into higher quality credits. Distressed exchanges, which can serve as a proxy for restructuring maneuvers, accounted for a majority of defaults in the second quarter of this year, according to Bloomberg calculations based on data from Moody’s Ratings. While reshuffling debt through these transactions is supposed to make the underlying companies more attractive, it effectively divides existing lenders into winners and losers. Since creditors can’t always tell which side they’ll end up on, some are turned off altogether, preferring to skip the roller-coaster ride and invest when it’s over.” [Bloomberg, 2025-08-04]

Shrinking Labor Force

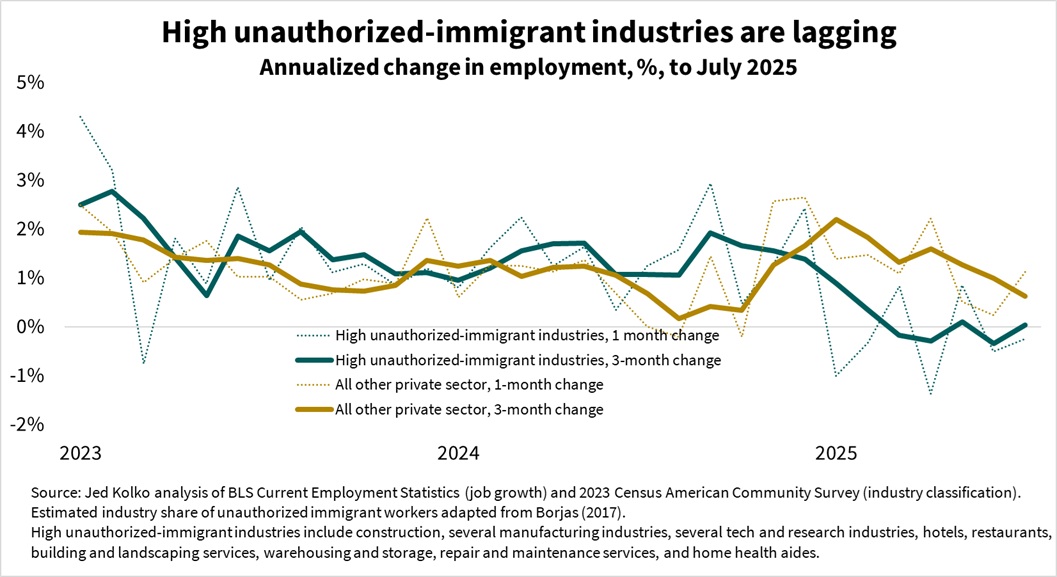

While Employment Growth Has Slowed Across The Whole Economy, Immigration Intensive Industries Have Seen Faster Declines In Growth. According to Jed Kolko,  [Jed Kolko, 2025-08-01]

[Jed Kolko, 2025-08-01]

More Expensive Inputs

August 2025: Trump Announced That He Would Raise Tariffs On Semiconductors. According to CNBC, “President Donald Trump said Tuesday he will unveil new tariffs on semiconductors and chips as soon as next week. ‘We”re going to be announcing on semiconductors and chips, which is a separate category, because we want them made in the United States,’ Trump said during a lengthy interview on CNBC’s ‘Squawk Box.’ Trump said that announcement will come ‘within the next week or so.’ He did not provide other details about the plan.” [CNBC, 2025-08-05]

Financial Instability

August 2025: Three Year Treasures Saw Weaker-Than-Expected Demand As Data And Policy Uncertainty Raised The Yield Investors Needed To Absorb The Trump Administration’s Growing Pile Of Debt. According to Bloomberg, “The Treasuries market saw most yields rise Tuesday after the first of this week’s three auctions of new notes and bonds drew weak demand. Yields for shorter-dated tenors rose the most, with the two-year note’s settling around four basis points higher Tuesday afternoon. Longer-maturity yields were little changed or slightly lower. While Treasuries had been rallying since last week, the auction result validated concern in some quarters of the market that yields had declined too much, and offered inadequate compensation for the risk that inflation data will stand in the way of expected Federal Reserve interest-rate cuts. A gauge of inflation in the US economy’s service sector compiled by the Institute for Supply Management unexpectedly increased in July to the highest level since October 2022. The $58 billion sale of three-year notes drew 3.669% versus its 3.662% yield in pre-auction trading shortly before 1 p.m. New York time, the bidding deadline. An auction is said to tail when the result indicates investors demanded a higher yield than indicated by pre-auction trading.” [Bloomberg, 2025-08-05]

Bloomberg Intelligence: August Market Pulse Indicator Reached “Manic.” According to Bloomberg, “Stock bulls have another reason to worry that the blistering rally in American equities may be about to cool. The Bloomberg Intelligence Market Pulse Index pushed to a ‘manic’ reading last month, a sign that investor exuberance may be running too hot. The measure combines six metrics like market breadth, volatility and leverage to deliver a reading on investor sentiment. When it gets into overheated territory, returns tend to weaken in the following three months. The Pulse index’s rise comes after the S&P 500 rallied almost 30% from its April low even as the American economy and labor market have shown signs of weakening. Surveys of investor sentiment indicate bullishness is growing toward alarming levels among Americans. And just this week, Wall Street strategists issued a slew of warnings that equities could face a pullback. ‘Risk taking in the stock market has gotten a bit overheated, so more muted returns may be in store in the next few months,’ Michael Casper, senior US equity strategist at BI, said by phone. ‘But this doesn’t necessarily signal a major selloff is imminent. Sentiment could hover at these levels for awhile, which may lead to a bumpier path for stocks in the second half of the year.’” [Bloomberg, 2025-08-06]

A $2 Trillion Market, Undermined

With The Prospect Of Trump Influencing The Bureau Of Labor Statistics, The $2 Trillion TIPS Market Is In Danger. According to Bloomberg, “The $2 trillion market for securities linked to US inflation data could be the first area of Treasuries to crack if the Bureau of Labor Statistics is politicized, according to bond investors. After President Donald Trump fired BLS chief Erika McEntarfer on Friday following a weak jobs report and said the figures were ‘rigged,’ investors have fretted that the move could erode trust in government data, which has a major effect on asset prices. That link is perhaps most acute in Treasury inflation-protected securities, where the face value of a bond is adjusted based on the consumer price index, which is calculated by the BLS. Interest payments are based on that floating principal. ‘If there is politicization of the BLS, and somehow the data is not credible it poses an enormous risk over time to the Tips market,’ said Amar Reganti, fixed income strategist at Hartford Funds. That concern was echoed by Michael Feroli, chief US economist at JPMorgan Chase & Co. ‘The $2.1 trillion market for TIPS is built on a foundation of trust in the construction of the CPI data’ Feroli wrote in a Sunday note. ‘The integrity of this data is at least as important as the employment data,’ Feroli said. ‘Here, even seemingly innocuous technical changes can matter.’ For example, calculating CPI with a method used by the European Union ‘would shave about 20 basis points off annual inflation,’ he said.” [Bloomberg, 2025-08-05]

Corruption

After Have Noted Their Expressed Intention To Benefit From Government Programs, Trump’s Oldest Two Sons’ Amended Their SPAC Filing To No Longer Explicitly Sell Their Corrupt Potential. According to Bloomberg, “Donald Trump Jr. and Eric Trump will advise a new company that’s looking to take over a US-based manufacturer, the latest in a string of such positions for President Donald Trump’s eldest sons. The Trump-advised blank-check company, called New America Acquisition I Corp., said Monday in a securities filing that it would look to do a deal with a firm ‘well-positioned to benefit from federal or state-level incentives, such as grants, tax credits, government contracts or preferential procurement programs.’ In an amended version of the document filed later the same day, that description and others were removed. The reason for the changes weren’t immediately clear, though the Associated Press reported the edit followed questions about potential for conflicts of interest, given the Trumps” involvement.” [Bloomberg, 2025-08-05]

Pushing Retirement Assets To Trump’s Friends

Trump Signed An Executive Order Making It Easier To Put 401(k) Assets In “Private Equity, Cryptocurrency And Private Real Estate.” According to the Wall Street Journal, “One order would make it easier for everyday Americans to invest their retirement savings in assets that lie outside public markets, such as private equity, cryptocurrency and private real estate. The move would fulfill a long-sought goal of Wall Street hedge funds and private-equity firms, which for years have wanted to tap in to the giant pool of money in 401(k) and other defined-contribution plans.” [Wall Street Journal, 2025-08-07]

Evidence of Successful Democratic Policymaking

Since The Biden Administration Pushed Through One-Day Trade Settlement, Trading Costs And Margin Requirements Have Dropped, Freeing Up More Capital To Be Put To Work. According to Bloomberg, “A long-feared change to Wall Street’s plumbing is paying off — and it’s freeing up billions. More than a year after the US adopted one-day settlement, a key measure of corporate bond trading costs is down 12%. Margin requirements — the cash or collateral firms must post to cover the risk of failed trades — have dropped 29%, according to Barclays Research. That’s capital that can now be put back to work. Plus, there are signs that those savings have boosted credit market liquidity. Score one for the US regulator, at least for now. The shift to T+1 was born of meme-stock chaos, when a wave of settlement failures exposed the dangers of delay. Europe, including Britain and Switzerland, is slated to follow in 2027. Barclays” findings align with data from the Depository Trust & Clearing Corporation, which last year showed that capital held to cover potential trade failures fell 29% to a quarterly average of $9.1 billion, down from $12.8 billion. ‘Think of it as an efficiency boost to the system — or, put differently, as if your insurance premium just went down,’ Zornitsa Todorova, head of thematic fixed income research at Barclays, said in an interview. ‘That capital can either be used to trade more actively or deployed elsewhere.’” [Bloomberg, 2025-08-06]