The Chicago Fed’s National Financial Conditions index provides a weekly update on financial conditions, with positive values indicating tighter than average conditions. The plot above shows the week-to-week change in two indices: overall leverage, and non-financial leverage. Their positive values indicate that achieving leverage in business operations has been getting harder.

The story told by this plot is as follows: around Trump’s election, the rate of overall leverage conditions tightening slowed to the point where those conditions began to loosen, before that loosening weakened in the days and weeks after his inauguration in the lead up to his announcement of “reciprocal” tariffs, before that tightening slowed and became loosening again, which diminished and has now come back to tightening.

Importantly, however, financial flows dominate the overall leverage story, so looking at non-financial leverage conditions, those have been continuously tightening since before his election.

Economic Degradation

Higher Prices

Trump’s Tariffs And Immigration Policies Have Made Housing More Expensive. According to Bloomberg, “Building or buying a new house costs even more than purchasing an existing home, and President Donald Trump’s tariffs are making the materials more expensive. Another cost pressure: Immigrant workers—the majority of plasterers, drywall installers, roofers and painters—are going into hiding as US Immigration and Customs Enforcement raids terrorize their communities.” [Bloomberg, 2025-08-13]

Trump’s Trade War

While Corn, Soybean, And Wheat Prices Have Fallen, Prices For Key Nutrients And Machinery Have Increased For Farmers. According to Bloomberg, “President Donald Trump has repeatedly said he loves farmers. His actions, though, are rippling across the agriculture industry as tariffs raise the cost of everything from tractors to fertilizers and squeeze profits for US growers already contending with low crop prices. The sweeping effects of the president’s trade war are coming into sharper focus as agricultural giants including Mosaic Co., AGCO Corp. and Bunge Global SA report their latest results: deliveries of key nutrients to the US have plunged, machinery prices are climbing and crop buyers are limiting purchases amid mounting uncertainty. The levy-inflicted costs come at a time when American farmers — who by and large strongly support Trump — have little buffer to absorb the impact. A benchmark for corn, soybean and wheat prices has fallen to its lowest levels since the height of pandemic lockdowns amid ample supplies globally, cutting into farm revenues.” [Bloomberg, 2025-08-08]

Capital Flight

Barry Eichengreen: A World Where The Dollar Loses Supremacy Would Lead To An Expected 80 Basis Point Hike In American Interest Rates. According to Bloomberg, “The US would have to give up some of the benefits of the strong-dollar regime, a key one being lower interest rates as fewer overseas investors buy dollar-denominated bonds. Barry Eichengreen, an economist at the University of California at Berkeley, who’s written extensively on the dollar, has calculated that in a scenario where the US withdraws from the global stage, the dollar’s share of reserves in countries that rely on its security could decline by about 30 percentage points. Long-term US interest rates could increase by as much as 0.8 of a percentage point, he estimates. US banks will need to pay more to raise money and charge more for mortgages as a result. Higher home loan rates tend to slow the economy because they leave less income for consumers to spend on vacations, home improvements and the like. And though a weaker foreign exchange rate may be good for rebalancing the trade deficit—by making American exports cheaper and more competitive and deterring spending on costlier imports—that’s not great for household wealth.” [Bloomberg, 2025-08-11]

As A Carry Trade Against The Dollar Has Gained Steam, Investors Have Consistently Poured Cash Into Developing-World Debt For The Past Four Months. According to Bloomberg, “Donald Trump’s erratic policies have left traders scrambling to diversify their holdings, sending the US Dollar Index to its worst first half of the year since the 1970s. The shift, which comes after a decade of US outperformance, has pulled in cash to emerging market assets following three years of outflows. Global funds dedicated to developing-world debt have seen inflows every week for the past four months, with investors pouring in $1.7 billion in the week ended Aug. 6, according to a Bank of America Corp. note citing data from EPFR. An index of local bonds has returned more than 12% as 18 out of 23 main EM currencies have gained against the dollar this year.” [Bloomberg, 2025-08-10]

The “Sell America” Trade Has Been Hard To Bottle Up, With Increased Demand For Currency Products Bypassing It. According to Bloomberg, “Like an uncorked genie, the “sell America” talk is proving hard to bottle up again. Banks and brokers are seeing rising demand for currency products that bypass the dollar, and some of Asia’s richest families are cutting exposure to US assets, saying Trump’s tariffs have made the country much less predictable. Geopolitical rivals within BRICS—a loose group of large economies led by Brazil, Russia, India, China and South Africa—are continuing their long push for a new cross-border payments system. Even long-term allies such as Europe see an opportunity to erode the dominance of the dollar.” [Bloomberg, 2025-08-11]

Oil Market Stress

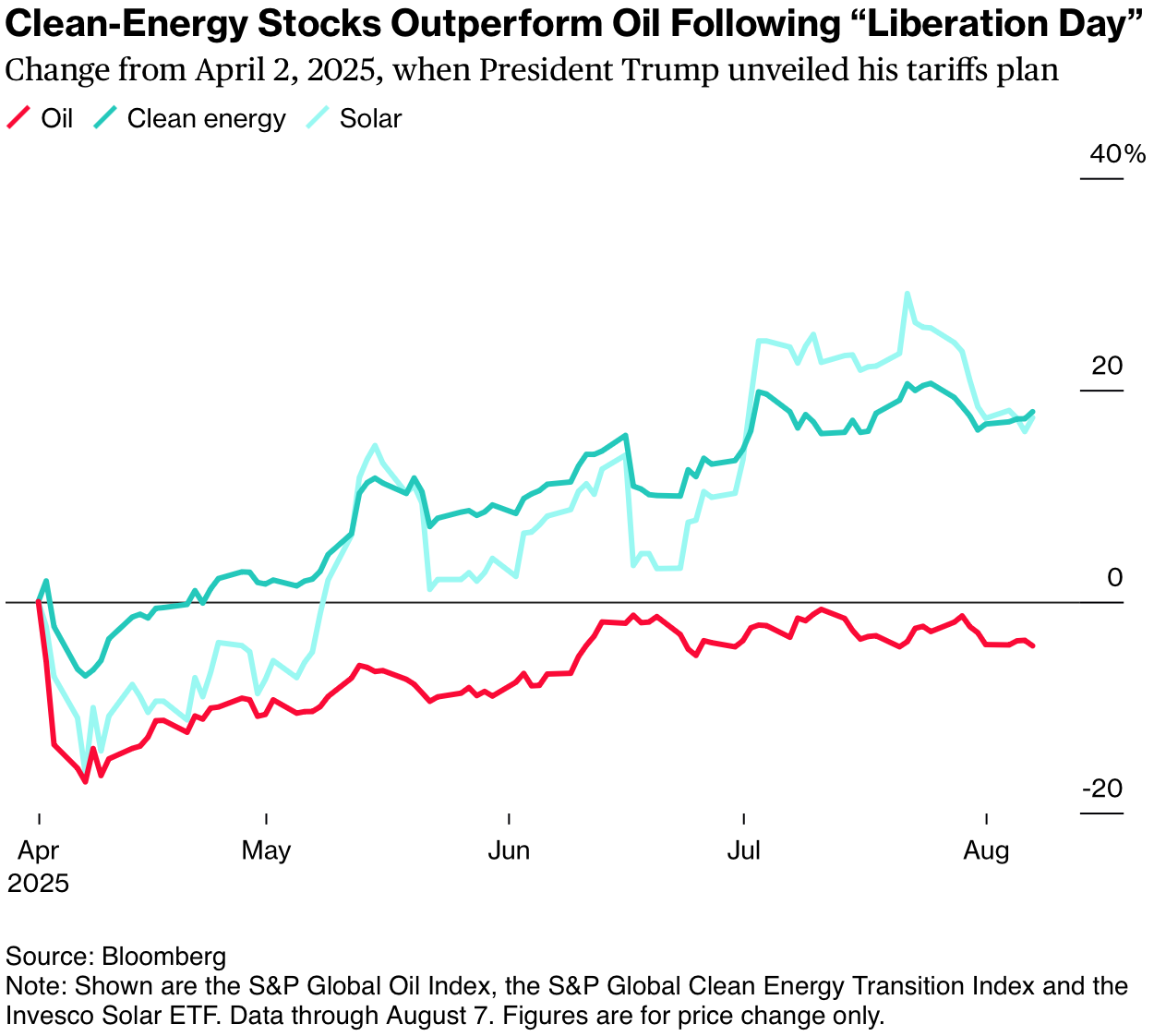

As Concerns About The Balance Of Supply And Demand In The Oil Industry Have Risen, Hedge Funds Have Turned Shorter To It. According to Bloomberg, “Since the beginning of October and through the second quarter, equity-focused hedge funds have — on average — been mostly short oil stocks, according to a Bloomberg Green analysis of positions on companies in global indexes for sectors spanning oil, wind, solar and electric vehicles. That’s a reversal of bets that had dominated since 2021, according to the data, which are based on fund disclosures to Hazeltree, an alternative-investment data specialist. […] There has been ‘a bottoming out with some of these clean energy plays,’ said Todd Warren, portfolio manager at Tribeca Investment Partners Pty. That trend has ‘really occurred at the same time as we’ve seen — in the oil patch — some concerns with regards to supply and demand balance,’ he said.” [Bloomberg, 2025-08-10]

The Slowing Trump Economy Has Raised The Question, “Who’s Buying The Oil.” According to Bloomberg, “Once investors take in ‘the general slowdown in everything,’ the question then becomes, ‘who’s buying the oil?’ said Kerry Goh, Singapore-based chief investment officer at Kamet Capital Partners Pte. Greenwich, Connecticut-based Tall Trees Capital Management LP is short oil stocks because ‘we see much lower oil prices, especially in 2026,’ said Lisa Audet, the fund’s founder and chief investment officer. Investors may get further insight into the supply-demand balance as early as this week, with OPEC set to release its monthly market analysis. Updates are also due from the US Energy Information Administration and the International Energy Agency. On Monday, oil held close to two-month lows. In the US, meanwhile, President Donald Trump’s quest to add supply in an effort to bring down the price of oil has unsettled local producers. The Dallas Fed’s latest quarterly energy survey, published on July 2, shows negative sentiment among oil companies toward the Trump administration’s policy on the fossil fuel. One respondent in the anonymized study said the administration’s implied price target of $50 a barrel is simply unsustainable for the industry. Another spoke of the ‘chaos’ caused by current US trade policies, adding the volatility will drive companies to ‘lay down rigs.’” [Bloomberg, 2025-08-10]

Financial Instability

Head Of Private Assets Behemoth Chosen By Meta For Private Credit Offering: Private Markets Untested By Steep Economic Downturns. According to the Financial Times, “Private markets ‘haven’t been tested’ yet by a steep economic downturn, the chief of $2.1tn bond giant Pimco has warned, urging the need to ‘constantly think about what can go wrong’. ‘We really haven’t had a hard recession since the great financial crisis,’ said Emmanuel ‘Manny’ Roman, chief executive of California-based Pimco, in an interview with the Financial Times. ‘You saw one very dicey month during Covid,’ he added, before a flood of public money came to the rescue. ‘The private markets in their current form haven’t been tested, and they will be tested when there’s a recession.’ Roman is well-positioned to assess the potential pitfalls of the roaring expansion in private capital, as asset managers and private capital firms rush to expand investor access to private markets, triggering concerns over whether such illiquid assets are suitable for retail investors. About $200bn of the firm’s assets under management were invested in alternative assets as of March 31, making it a major player in private capital. Last week, Bloomberg reported that social media giant Meta had picked Pimco to lead $26bn of debt financing to fund its data centre expansion. Private equity, private credit, real estate and other ‘alternative’ asset classes have boomed in recent years, as investors seek out higher returns than those available in public markets. A study from consultants at Bain and Company last year projected private market assets under management would grow at more than twice the rate of public assets to reach as much as $65tn by 2032. A widely anticipated White House executive order, issued this week, will open up 401(k) retirement accounts to private markets, a probable catalyst for even greater demand for so-called ‘alts’.” [Financial Times, 2025-08-11]

Administration Being Wrong About Numbers

Bloomberg Economics: The Trump Administration Has Misread Data On The Changing Immigrant Share Of Employment. According to Bloomberg, “The report does include a breakdown of foreign and native-born workers based on a survey of households, and the numbers indicate the foreign-born workforce and population has fallen by about a million over the last three months — a number administration officials were quick to seize on in touting their immigration policy achievements. ‘Since the president took office, he created about 2.5 million jobs for Americans, whereas we’ve eliminated about a million jobs for foreign-born workers,’ Stephen Miran, chair of the White House Council of Economic Advisers, said in an Aug. 1 CNN TV appearance. ‘That’s a result of our strong immigration policy, of our strong border policy, keeping America safe,’ said Miran, whom Trump nominated Thursday to fill a temporary slot on the Fed’s Board of Governors. But many analysts, including those at Bloomberg Economics, have written off the decline in the labor force, noting it is largely related to how the data are constructed. Many economists point to a simultaneous, implausible surge in the native-born workforce and population numbers. ‘It’s not that we’ve suddenly given birth to a lot of 16-year-olds and boosted the native population,’ said Jonathan Pingle, the chief US economist at UBS.” [Bloomberg, 2025-08-09]

Corruption

Allowing 401(k)s To Invest In Private Markets Could Allow Flailing PE Investments To Be Bailed Out By “Perpetual, Indicriminate” Buyers. According to Bloomberg, “Should private equity be included in 401(k) plans, it means more ‘perpetual, indiscriminate’ buyers, which could unblock the bottleneck in PE exits, said Brian Payne, chief strategist of private markets and alternatives at BCA Research Inc. Evergreen funds are going to rise, but traditional drawdown vehicles will still dominate their portfolios, said Payne, former investment officer at the Teachers” Retirement System of the State of Illinois.” [Bloomberg, 2025-08-08]

If Trump’s GSE IPO Goes Forward, “It Could Create A Windfall For Investors Like Bill Ackman And John Paulson” Who Both Prominently Supported Trump’s Presidential Campaign. According to the Wall Street Journal, “The Trump administration is preparing to sell stock in mortgage giants Fannie Mae and Freddie Mac in an offering it believes could raise around $30 billion and kick off later this year, according to people familiar with the matter. The plans being discussed by some administration officials could value the companies at roughly $500 billion or more combined and involve selling between 5% and 15% of their stock, some of the people said. Still up for debate is whether the mortgage giants would IPO as one company or two separate entities. Fannie and Freddie, which bundle and sell mortgages, have been under government control since the 2008 financial crisis and rely on a government-backed guarantee to protect investors from losses. Shares of the firms, which currently trade on over-the-counter markets, each closed roughly 20% higher after The Wall Street Journal reported on the offering plans. It is unclear whether Fannie and Freddie would remain under government conservatorship. Bill Pulte, head of the Federal Housing Finance Agency, has in the past suggested the firms could remain under conservatorship while conducting a share offering, without clarifying how it would work. […] If any deal goes forward, it could create a windfall for investors like Bill Ackman and John Paulson who bought shares years ago, banking on the idea that eventually the government would sell stock in the mortgage giants. […] Ackman’s Pershing Square owns a roughly 10% stake in the common shares of both Fannie and Freddie. Paulson owns a sizable investment in preferred shares. Both Ackman and Paulson endorsed Trump for president.” [Wall Street Journal, 2025-08-08]