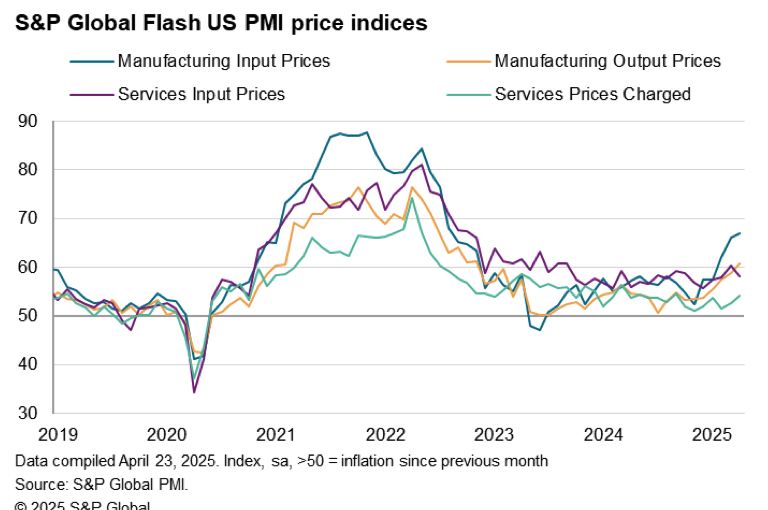

S&P Headline: Output Growth Hits 16-Month Low As Confidence Slumps And Selling Prices Rise At Increased Rate [S&P Global, 2025-04-23]

April 2025: Exports Of Services Fell, Subduing Demand Growth. According to S&P Global, “Demand growth was subdued in particular by a fall in exports of services (which include tourism-related activities as well as cross-border activities by service providers) on a scale not seen since January 2023.” [S&P Global, 2025-04-23]

April 2025: Corporate Sentiment About Future Output Fell For A Third Consecutive Month, To The Lowest Level Since July 2022, And The Joint-Second Lowest Level Since September 2020. According to S&P Global, “Sentiment among companies about their output over the coming year fell for a third successive month, dropping sharply to register the least optimistic outlook since July 2022. The latest reading was the joint-second lowest since September 2020, surpassed only by October 2022.” [S&P Global, 2025-04-23]

April 2025: Manufacturing Employment Fell For The First Time Since October 2024. According to S&P Global, “Employment rose slightly in April, up for the fourth time in the past five months, albeit registering a smaller gain than in March and a much-reduced rate of hiring compared to the strong 31-month high seen at the start of the year. Although a modest net increase in payroll numbers was recorded across the service sector in April, manufacturing jobs were cut for the first time since October. Hiring was often restricted by concerns over the economic outlook and demand environments both at home and in export markets, with rising cost concerns and labor availability also cited as restricting factors.” [S&P Global, 2025-04-23]

April 2025: Manufacturing And Service Sector Input Prices Rose Faster Than Output Prices, Compressing Margins. According to S&P Global, [S&P Global, 2025-04-23]

p1 =plot(price_data.date, price_data.median_sale_price ./1000.0, label ="Median (Left Axis)", xlabel ="Date", ylabel ="Price (\$'000)", title ="Q1 2025: Prices Of Homes Sold Fell", legend =:bottomleft)plot!(twinx(), price_data.date, price_data.mean_sale_price ./1000.0, label ="Mean (Right Axis)", color=colorant"#525252", ylabel ="Price (\$ '000)")

Sentiment

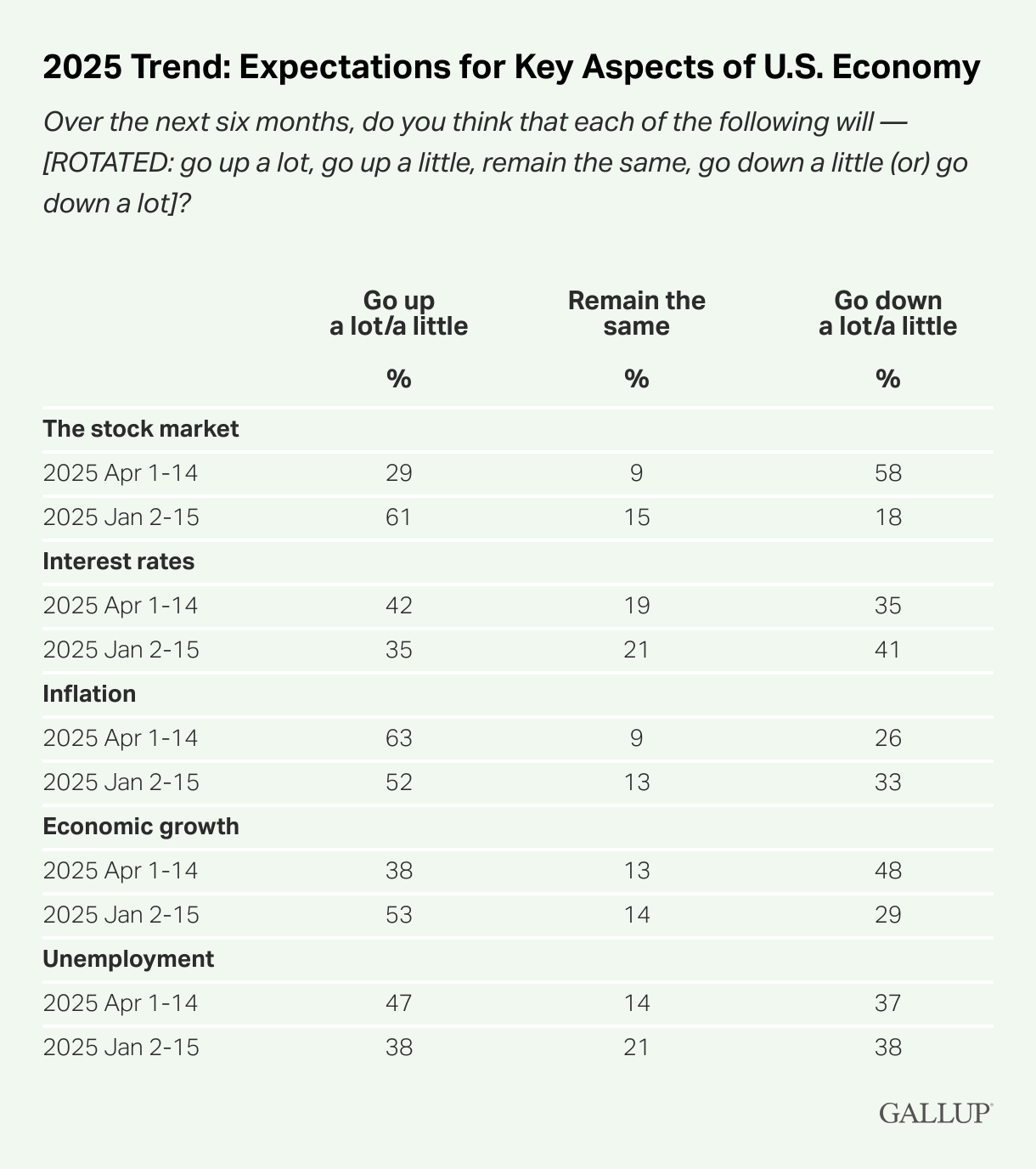

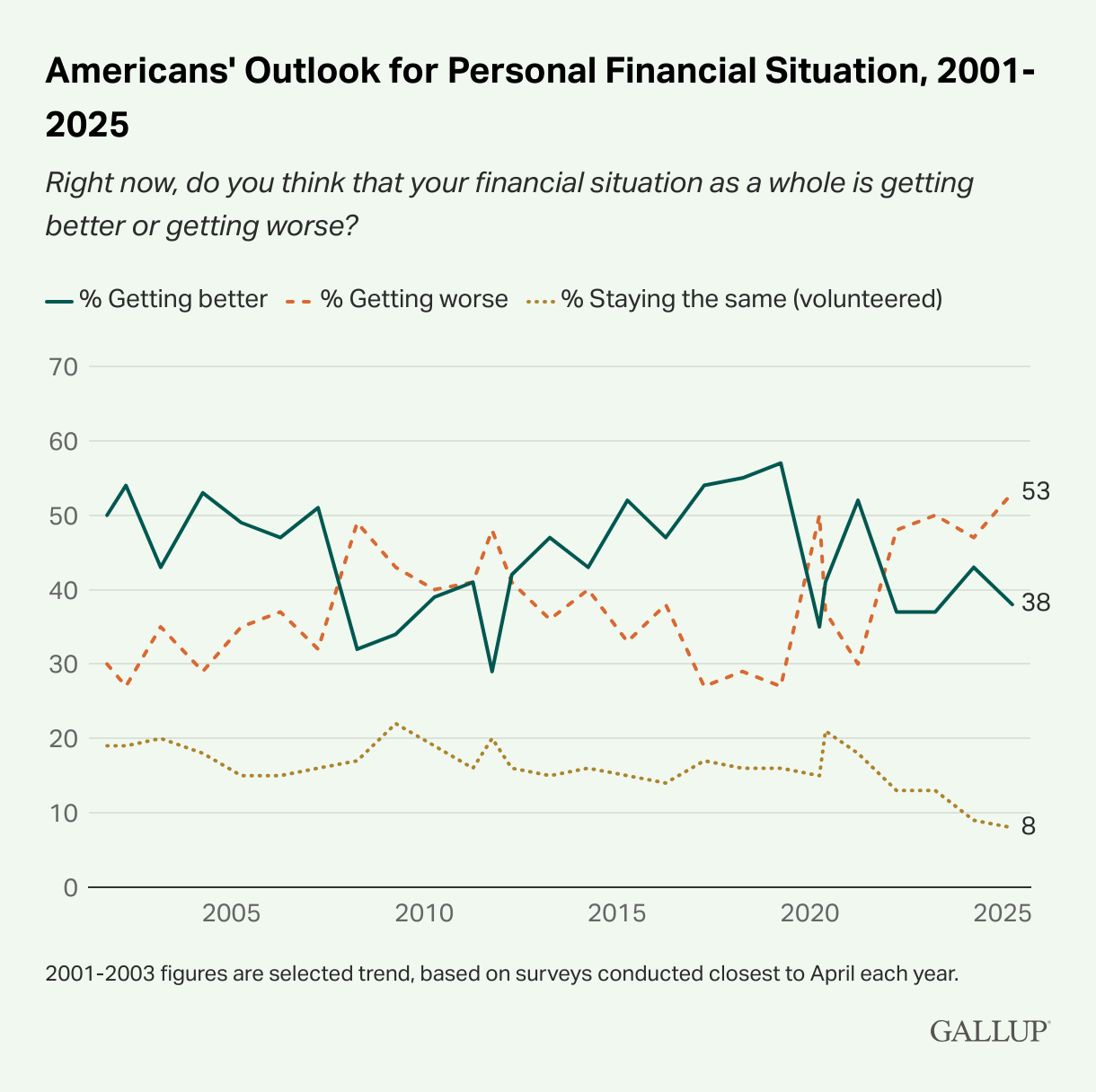

April 2025: For The First Time Since 2001, A Majority Of Americans Expressed Financial Pesimism About Their Own Finances. According to Gallup, “Several measures of Americans’ economic mood, including their perceptions of the U.S. economy and their own finances, have weakened in April compared with their prior readings — in some cases, substantially. Most notably, since January, Americans’ six-month outlooks for economic growth and the stock market have turned from positive to negative, while their forecasts for inflation, interest rates and the job market have dimmed. In line with those changes, Gallup’s yearly reading on Americans’ assessment of their personal finances shows a record-high 53% now believing their situation is getting worse. This marks the first time in the trend dating back to 2001 that a majority have expressed financial pessimism.” [Gallup, 2025-04-21]

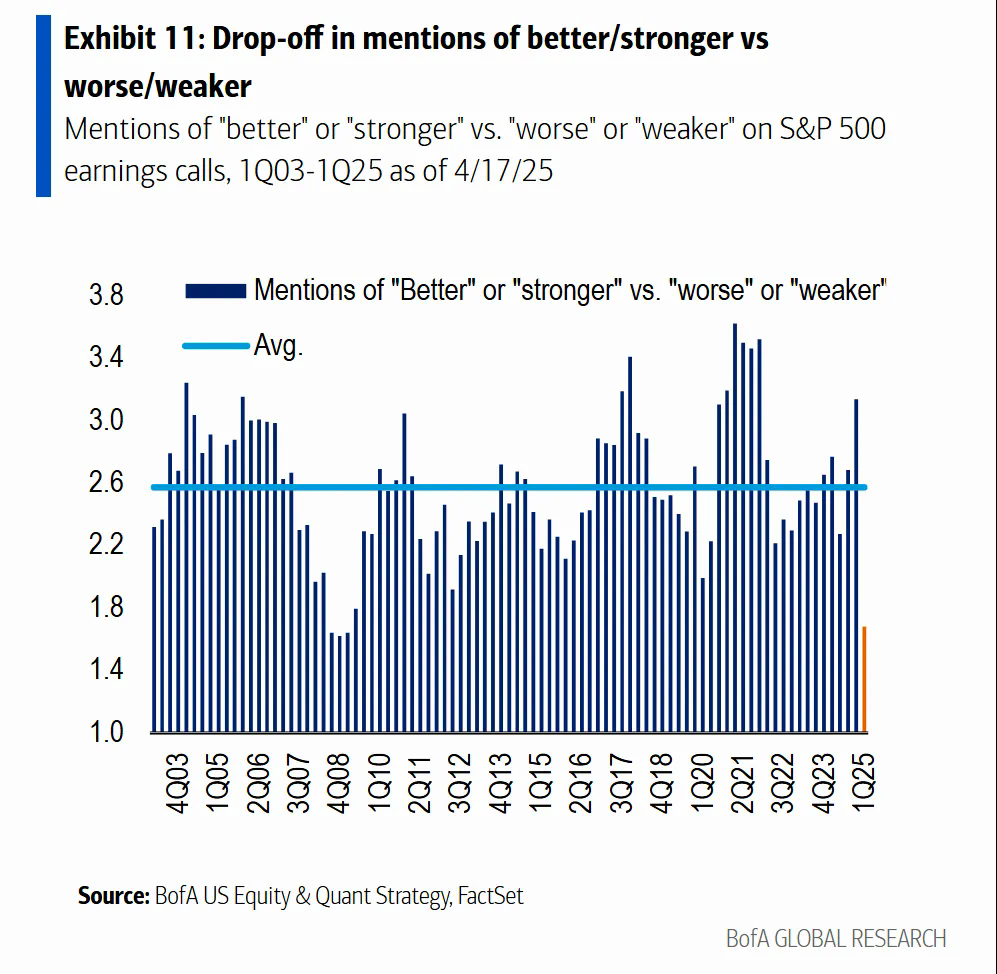

Bank Of America: Upgraded To Downgraded Earnings Guidance Reached Its Lowest Level Since The Pandemic, While Dictionary-Based Sentiment Analysis Dropped To 200 Levels. According to Bloomberg, “In fact, according to Bank of America analysts led by Savita Subramanian, we”ve only seen eight companies in the S&P 500 actually issue fresh earnings guidance so far this season. None of that has turned out to be above-consensus, and the proportion of upgraded earnings guidance to downgraded earnings guidance over the last three months is now at its lowest since Covid. Mentions of words like ‘better’ or ‘stronger’ versus words like ‘worse’ or ‘weaker’ are also at the lowest level since the 2008 financial crisis.” [Bloomberg, 2025-04-22]

April 2025: Bessent Told A Closed-Door Gathering Hosted By JP Morgan That The Trade Situation With China Was “Unsustainable” According to Bloomberg, “US Treasury Secretary Scott Bessent told a closed-door investor summit Tuesday that the tariff standoff with China cannot be sustained by both sides and that the world’s two largest economies will have to find ways to de-escalate. That de-escalation will come in the very near future, Bessent said during an event hosted by JPMorgan Chase & Co. in Washington, which wasn’t open to the public or media. He characterized the current situation as essentially a trade embargo, according to people who attended the session.” [Bloomberg, 2025-04-22]

Bessent Denied Intentions Of Decoupling From The Chinese Economy. According to Bloomberg, “Bessent said that it was not the US’s goal to decouple from China and that the current status quo of 145% tariffs on Chinese goods by the US and 125% tariffs on US products by China was not sustainable. He expressed optimism that tensions could cool in the coming months, which would bring relief to markets, but cautioned that a larger deal could take longer.” [Bloomberg, 2025-04-22]

Trump Promised To Be “Very Nice” To The Chinese Government In Any Trade Deal, Previewing “Substantial Tariff Reductions.” According to Bloomberg, “President Donald Trump said he plans to be ‘very nice’ to China in any trade talks and that tariffs will drop if the two countries can reach a deal, a sign he may be backing down from his tough stance on Beijing amid market volatility. ‘It will come down substantially but it won’t be zero,’ Trump said Tuesday in Washington, following earlier comments from Treasury Secretary Scott Bessent that the standoff was unsustainable. Trump added that ‘we”re going to be very nice and they”re going to be very nice, and we”ll see what happens.’” [Bloomberg, 2025-04-22]

Legal Justifications

April 2025: The Trump Administration Moved To Transfer A Case Challenging The Power He Claimed To Impose The Tariffs To An Appeals Path More Defferential To Presidential Power. According to Bloomberg, “President Donald Trump wants legal challenges to his sweeping tariffs to be heard by a specialized trade court, an approach that worked in his favor during his first administration even though it didn’t give him an immediate victory. The Trump administration is seeking to transfer three cases filed in federal courts in Florida, Montana and California to the US Court of International Trade, or CIT, whose judges handle technical disputes over tariffs. That court ruled against the president in lawsuits targeting his 2018 steel tariffs, but Trump emerged victorious when an appeals court sided with him. Legal experts say that steering the current cases on the same path will likely benefit the administration because they, too, would go through the US Court of Appeals for the Federal Circuit, which has historically been deferential to the authority of presidents to levy tariffs.” [Bloomberg, 2025-04-23]

Consequences

GE Aerospace Said It May Raise Prices In Order To Meet Financial Guidance. According to the Wall Street Journal, “GE Aerospace laid out a plan to offset tariffs Tuesday, while keeping its financial outlook unchanged, with some caveats. The jet engine maker said it aims to save $500 million by streamlining operations and seeking refunds for duties it pays on imported parts that are later exported. The company said it also may raise prices and look for additional cost reductions. Because of these actions, GE didn’t change its financial guidance for the year. But GE’s financial predictions don’t factor in a possible recession, any tariffs not already announced, or potential production slowdowns by aerospace companies such as Boeing and Airbus. GE posted better-than-expected quarterly adjusted earnings and revenue. Shares rose about 4% Tuesday morning.” [Wall Street Journal, 2025-04-22]

Dunn County ND Commissioner Tracey Dolezal: “There Will Be Job Losses,” As Trump’s Trade War Cuts Oil Prices, Infrastructure Upgrades May Need To Be Delayed. According to the Financial Times, “onald Trump’s global trade war is threatening a corner of America that voted in droves for the Republican president last year: oil-producing North Dakota. It might also upend the president’s plans to boost fossil fuel production in the state that launched America’s shale revolution. Trump’s tariff rhetoric triggered an oil price sell-off, with US prices plunging below $60 a barrel (West Texas crude settled at $63.08 a barrel on Monday). The escalation raised concerns across the US shale patch, some of the reddest parts of America, about an impending slowdown. ‘It’s just scary,’ Tracey Dolezal, a commissioner of Dunn County, one of the top oil-producing areas in North Dakota’s Bakken basin, told the Financial Times. The county received nearly $40mn in oil and gas taxes last year, more than half of total revenue. ‘There”ll be some job losses. Some businesses are really going to feel the effect if prices keep dropping,’ Dolezal said, adding that the county, which voted overwhelmingly for Trump in the past three presidential elections, may have to reduce infrastructure upgrades if prices fall further.” [Financial Times, 2025-04-22]

North Dakota’s Undiversified Economy Could Be More At Risk Than Other Oil-Rich States. According to the Financial Times, “North Dakota — the third-largest oil-producing state — is especially vulnerable to falling crude prices and slowing production, more so than peers such as Texas and Louisiana, which have more diversified economies. A shrinking inventory of wells and an increasingly consolidated, financially restrained industry, has slowed drilling in the Bakken. Ron Ness, president of North Dakota Petroleum Council, said: ‘Falling and volatile commodity prices certainly don’t inspire companies to want to engage and act, particularly the companies that we”re hoping that now have a little wind on their back.’” [Financial Times, 2025-04-22]

$50 Per Barrel Oil, As Called For By Peter Navarro, Would Be Devistating To American Oil Producers. According to the Financial Times, “The White House has called for prices to fall further with trade adviser Peter Navarro last month suggesting $50 oil would help tame inflation, a call that has rattled the US’s shale sector. ‘If production drops and the price drops, it makes things more difficult,’ said Daniel Stenberg, head of economic development at McKenzie County, another top-producing county in the Bakken and where 85 per cent of the population voted for Trump last year. Reed Olmstead, executive director of upstream research at S&P Global Commodities Insights, said ‘$50 oil will not be good for any local economies’. Falling prices ‘would certainly have ripple effects throughout the region’, he added. North Dakota reaped the benefits of a technological breakthrough in the 2010s when advances in horizontal drilling and hydraulic fracturing triggered the US shale revolution and transformed the agrarian state’s fortunes.” [Financial Times, 2025-04-22]

April 2025: Los Angeles Port Officials Projected A Fall In Cargo Volumes Of At Least 10 Percent By May 2025. According to Bloomberg, “China remains Southern California’s largest trading partner, with roughly $130 billion in imports passing through the twin ports last year, according to the report. Los Angeles port officials expect cargo volumes to fall by at least 10% as early as May, with declines likely to continue through the end of the year.” [Bloomberg, 2025-04-22]

April 2025: More Than 900,000 Americans Were Employed In Trade And Transportation In Southern California. According to Bloomberg, “The region is home to major distribution centers, rail systems and trucking routes used by Amazon, Walmart, FedEx, UPS and Prologis, a real estate giant specializing in warehouses. Trade and transportation directly employ more than 900,000 workers in Southern California and indirectly supports nearly 2 million jobs. The tariffs tit-for-tat also leaves thousands of the region’s importers facing inputs that potentially are two-and-a-half times more expensive, forcing companies to absorb the price increases or pass them on to consumers, the report said.” [Bloomberg, 2025-04-22]

At Least One Shipment Of American Propane Was Diverted From China To Japan. According to Bloomberg, “In the aftermath of the new duties, reports of cargo diversions are emerging. At least one shipment of US propane that was signaling China diverted to Japan.” [Bloomberg, 2025-04-23]

Chinese Retaliation Against Trump’s Tariffs Has Made Importing American Liquefied Petroleum Gas Too Expensive To Use As An Input In Production. According to Bloomberg, “A typically quiet corner of the oil market is being thrust into the center of President Donald Trump’s tariff war with China. Liquefied petroleum gas, or LPG, is a product that gets split out when natural gas is extracted from the ground or when crude oil is refined. It can be used to make propane for heaters and barbecues or to make plastics for toys and drinking straws. China recently imposed tariffs of 125% on American goods, making it too expensive for some plants to process the fuel and bolstering the need to find alternatives from elsewhere. There’s been a surge in shipments of US LPG to China during the last few years, partly as the shale boom spurs more production of other liquids than ever before. To put the scale of that growth in context: For every barrel of crude oil that’s pumped in the US, there’s half a barrel of LPG-type liquid being produced. The volume has topped 7 million barrels a day at times. That’s triggered a jump in flows to China, where the capacity of plants that help turn propane into plastics has rapidly expanded. On average last year, China imported a combined 540,000 barrels a day of propane and ethane from the US, Energy Information Administration data show.” [Bloomberg, 2025-04-23]

WSJ: Major Credit Card Companies Have Raised Loss Provisions, Tightened Standards, And Moved Towards More Upmarket Consumers In Anticipation Of Tariff-Led Slowdowns. According to the Wall Street Journal, “The largest credit-card companies are preparing for the economy to get worse. An economic downturn could mean more customers can’t pay their bills, and banks and credit card companies are trying to get ahead of it, according to their latest earnings reports. Already, delinquencies are rising and are now in line with levels from before the pandemic. JPMorgan Chase and Citigroup added money to their rainy day funds to cover expected future losses. Retail-card issuer Synchrony is tightening its lending standards. U.S. Bancorp is chasing a more affluent customer base that could better withstand a downturn.” [Wall Street Journal, 2025-04-222https://www.wsj.com/economy/consumers/credit-card-debt-delinquencies-economy-a8d7c825?mod=hp_lead_pos6]

Capital Flight

December 2024 - April 2025: Global Fund Managers Changed From Being Net 36 Percent Overweight American Equities To 36 Percent Net Underweight American Equities. According to the Wall Street Journal, “The reversal in international investment flows could be sizable, given how massive they have been in one direction. In Bank of America’s December survey, the difference between the percentage of global fund managers who were overweight U.S. equities and those who were underweight was 36 percentage points, the highest on record. In the April poll released last week, that number sank to a 36 percentage-point net underweight, following the largest-ever two-month decline. Respondents mentioned “a crash in the dollar because of an international buyers’ strike” as a new danger, echoing recent talk about a “risk premium” being applied across U.S. assets.” [Wall Street Journal, 2025-04-23]

Japanese Bond Sales

Following Trump’s Tariff Announcement, Japanese Sales Of U.S. Long-Dated Bonds Were Higher Than Over Any Two Week Period Since Records Began. According to the Financial Times, “Japanese investors offloaded more than $20bn in international bonds as US President Donald Trump’s tariffs shook markets early this month, in a sign of how the Wall Street turbulence cascaded around the world. Private institutions, including banks and pension funds, sold $17.5bn of long-dated foreign bonds in the week to April 4 and another $3.6bn over the next seven days, according to preliminary data from Japan’s Ministry of Finance. Japan holds $1.1tn in US Treasuries across the public and private sectors — the biggest international stockpile in the world — so its transactions are closely monitored and considered a proxy for buying or selling of US government debt. The recent sell-off marks one of the biggest outflows over any two-week period since records began in 2005.” [Financial Times, 2025-04-22]

Declining U.S. Equity Prices Forced Japanese Investors Equity Allocations Down, Forcing Debt Sales. According to the Financial Times, “According to several investors, the fall in US equities would have knocked Japanese pension funds’ allocations to international debt and equity out of balance. As a result, the funds would have been under pressure to sell Treasuries and other US government-backed debt to bring their portfolios back into alignment, they said.” [Financial Times, 2025-04-22]

Before the announcement of Trump’s liberation day tariffs, Japanese investors in the U.S. were doing extremely well. The weak Yen relative to the dollar multiplied performance for Yen-denominated holders of U.S. equities. This meant that their allocation rules (as I explained here) forced them to sell U.S. equities and buy U.S. bonds. After the announcement, however, while American investors saw a drawdown of as much as 18.9 percent, Japanese investors saw a drawdown of 24.09 percent. As a result, they had to reallocate even more aggressively by selling bonds.

Where that is problematic for the real economy, is that the outflow from bonds makes life much more difficult for American businesses than the outflow from equities, as it drives interest rates up more. Especially when there are already structural reasons for the increase in interest rates.

Inefficient Capital Allocation

Q1 2025: Lobbying Reports Mentioning Tariffs Jumped 95 Percent From One Year Ago. According to Bloomberg, “The number of companies lobbying on tariffs nearly doubled in the first quarter as President Donald Trump threatened a wave of sharp new import duties that could reshape global supply lines. Nearly 350 corporate reports listed tariffs as a specific issue they were discussing with the White House and lawmakers on Capitol Hill, up from 179 during the first quarter of 2024, according to a Bloomberg analysis of federal lobbying disclosures.” [Bloomberg, 2025-04-23]

April 2025: While 47 Percent Of Businesses Had Raised Prices This Year, 60 Percent Planned To In The Second Quarter. According to the Wall Street Journal, “Some 47% of small businesses say they have increased prices since the beginning of the year, and 60% plan to raise prices in the next three months, according to a survey of more than 500 small businesses conducted in April for The Wall Street Journal by Vistage Worldwide, a business-coaching and peer-advisory firm.” [Wall Street Journal, 2025-04-23]

April 2025: Hardware Distributor Fastenal Raised Prices. According to the Wall Street Journal, “Hardware distributor Fastenal said it raised prices in April. In a call with analysts earlier this month, Fastenal’s then-finance chief, Holden Lewis, said it developed a pricing-review tool in response to earlier rounds of tariffs in 2018. This allows the company to provide granular information to its customers about ‘the whys and the whats and the wheres’ of the price increases, he said. (Lewis’s planned resignation was effective last week.) ‘You never say this is an easy conversation, and the order of magnitude is somewhat something we haven’t navigated before,’ Lewis said.” [Wall Street Journal, 2025-04-23]

Business Conditions

April 2025: Banks Have Failed To Syndicate Billions Of Dollars In Loans, As Uncertainty Has Driven Away Buyers. According to Bloomberg, “Banks have been stuck with some $4.6 billion of debt after buyouts for pet supplies company Patterson Cos. and ABC Technologies Holdings Inc., an Apollo Global Management Inc.-backed Canadian auto parts company, closed before banks syndicated the debt to other investors. This happened as April’s uncertainty briefly sent premiums on US junk bonds to the highest in nearly two years and leveraged loan secondary-market prices to their lowest since mid-2023.” [Bloomberg, 2025-04-21]

Notes From IMPA’s Tax Policy, Inequality, and Uncertainty Conference

Larry Summers: The Trump Administration’s Moves To Downsize The IRS Could Cost The Government $1 Trillion In Reduced Revenue Over A Decade. According to Bloomberg, “Former Treasury Secretary Lawrence Summers said that the Trump administration’s moves to downsize the Internal Revenue Service, along with other changes, are likely to incentivize reduced tax-payment compliance — potentially costing the federal government $1 trillion in lost revenues over a decade. “We are threatening the basis of our tax system, which is based on voluntary compliance,” with the efforts to slash the IRS’s staff, Summers said on Bloomberg Television’s Wall Street Week with David Westin. Summers said he’s currently conducting analysis on the issue, along with colleagues he didn’t specify. “I’d be surprised if we’re not on a path to sacrificing more than $1 trillion of revenue over the next decade because of this misguided, wanton attack on the IRS,” he said.” [Bloomberg, 2025-04-22]

Yale Budget Lab: 18,000 Layoffs At The IRS Could Cost Between $159 Billion And $1.6 Trillion Over Ten Years. According to Bloomberg, “The Budget Lab at Yale, a nonpartisan research group, forecast that laying off about 18,000 IRS employees would result in a net revenue loss of roughly $159 billion over ten years. That could rise to as much as $1.6 trillion over a decade if non-compliance were high, the group said.” [Bloomberg, 2025-04-22]

The reason this report is so late is that I spent this morning at a conference hosted by the American University Institute of Macroeconomic Policy Analysis on Tax Policy, Inequality, and Uncertainty of the American Economy. It was helpful in trying to understand where our top tax thinkers are on the issues of the day.

While there is some clarity on the underlying economic issues, these thinkers do seem to be woefully out of touch with the macro scale political realities, although some work on that problem has been done, although there is some danger that it is being misinterpreted.

On the overall tax policy front, Nobel Laureate Joseph Stiglitz emphisized some failures in our current tax system, and noted that tracking errors made it so that there was no easy elegant solution to those problems.

One extremely important thing that he emphasized is that the corporate tax is a corporate profits tax, not a tax on returns to capital. In a corporate environment like the one we have today, a huge percentage of those profits are monopoly rents, and allowances like the accelerated depreciation allowance are actually subsidies to capital investment.

That helps to explain why the response to the TCJA was not an increase in corporate investment, as so many commentators at the time suggested it would be.

While that is a powerful message, it is muted by the fact that he spent the rest of his time talking about how long-term capital gains tax rates should not be lower than short term ones, and that capital gains taxes should be paid every year, rather than when the investments are sold. While both ideas are economically compelling, they are politically toxic, and give fodder to the right.

While Donald Trump is blowing up the macroeconomy, if we embrace that type of messaging we risk losing parts of the coalition that we need to win elections. While the loss of working class voters has been rightfully lamented, our gains with educated voters are something that we need to hold on to. While there are exceptions, subtraction is generally not a winning strategy in political elections.

Speaking of the working class, Ilyana Kuziemko talked about her research here on the policy perspectives of the working class with regard to policies that reduce inequality. The most important takeaway is that the working class favors “predistribution” to redistribution. Here thesis here is the same as what drives the upper class’ preference for redistribution over predistribution. When income is distributed after tax, more powerful people retain their control of the means of production.

This also means that the working class see redistribution as hand outs, whereas policies that promote higher wages and a less unequal distribution of income are seen as rewarding hard work. This is important messaging and policy guidance, but it should be taken with a grain of salt.

That is due to the facts that we have some difficulty infiltrating the media consumed by uneducated voters, and we do not want to alienate our current base of educated voters.

That goes back an anecdote from the Brookings Institutions’ Vanessa Williams. When FDR created Social Security, during the Great Depression, employers who opposed it included notes in workers’ paychecks saying that their wages had been cut to pay for the program. Luckily, the program was up and running quickly, and popular quickly.

While many programs are popular when voters are surveyed about them, if there is a long delay between the program’s passage of and the implementation give time for bad faith attacks. Congestion Pricing is a canonical example of this. So when we next have any power, any distribution based programs we implement need to be visible quickly.

[S&P Global,

[S&P Global,  [Gallup,

[Gallup,  [Gallup,

[Gallup,  [Bloomberg,

[Bloomberg,  [Bloomberg,

[Bloomberg,